Energy News Beat

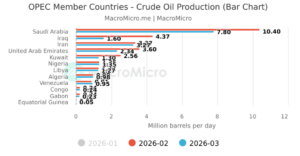

Saudi Arabia has delivered a stark update to OPEC: its crude oil production plunged another 651,000 barrels per day (b/d) in April, hitting just 6.316 million b/d—the lowest level since the 1990 Gulf War. According to a monthly report from OPEC’s secretariat obtained by Bloomberg, the kingdom’s output has now fallen a cumulative 42% since February, as the ongoing U.S.-Israeli war with Iran continues to choke off Persian Gulf exports.

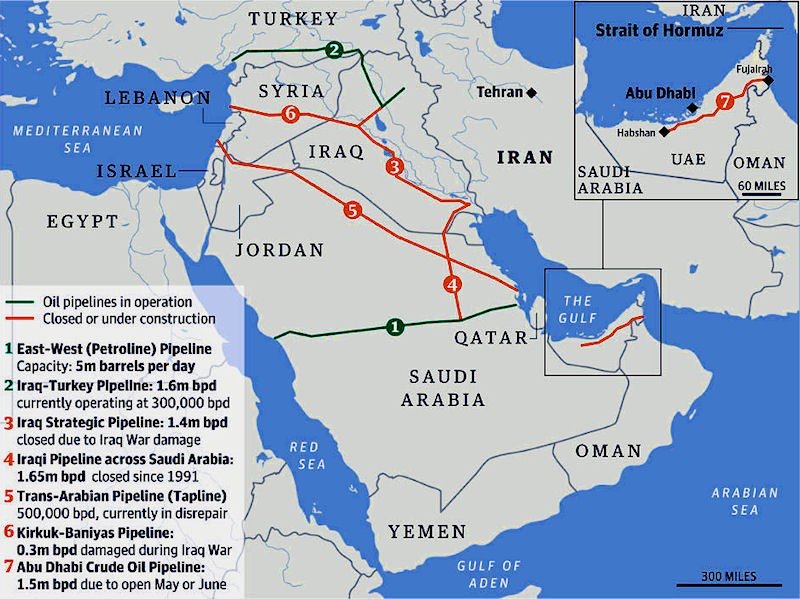

The decline is directly tied to disruptions from the Iran conflict, which has effectively blocked much of the Strait of Hormuz—the critical chokepoint for roughly one-fifth of global seaborne oil trade. Saudi Arabia, along with neighbors like Iraq, Kuwait, and the UAE, has seen massive shut-ins, with limited use of bypass pipelines unable to offset the losses. This marks the sharpest supply shock in decades, pushing global oil inventories down at a record pace and sending Brent crude prices spiking well above $100 per barrel in recent months.

OPEC Production Trends Over the Last 10 Years

OPEC members’ output has fluctuated significantly over the past decade due to a mix of voluntary cuts under OPEC+, geopolitical tensions, sanctions, and the COVID-19 demand crash. Pre-2022, major producers like Saudi Arabia routinely ran 9–11+ million b/d, while total OPEC crude hovered around 28–32 million b/d. Recent years saw deeper cuts, followed by partial unwinding—until the 2026 Iran war triggered unprecedented shut-ins.

Here are recent snapshots and historical trends for key OPEC members (pre-UAE exit):

Key 10-Year Context (approximate averages from EIA/OPEC data): Saudi Arabia: Peaked near 10–12 mb/d; now sharply lower due to war.

Iraq: Steady 4–5 mb/d range pre-war; recent ~60% drop to ~1.3 mb/d amid Hormuz issues.

UAE: ~3–4 mb/d; exited OPEC May 1.

Iran: Sanctions-hit but recovered toward 3+ mb/d pre-war.

Venezuela: Chronically low (~0.7–1 mb/d) due to infrastructure and sanctions.

Others (Kuwait, Nigeria, etc.): Volatile with quotas and outages.

Total OPEC crude has averaged ~30 million b/d recently but is now far below that amid the crisis.

Current Oil Market Situation

The Iran war (escalating since late February 2026) has created the biggest supply crisis in modern history. The de facto closure of the Strait of Hormuz has disrupted ~12–18 million b/d of flows at peak, leading to sharp global inventory draws—117 million barrels in April alone, per IEA estimates. OPEC+ responded with modest quota hikes (206,000 b/d for May, 188,000 b/d for June), but these are largely “on paper” while physical production remains paralyzed.

Non-OPEC supply (led by the U.S.) has helped somewhat, but the market remains tight. Brent averaged ~$117/b in April, with forecasts calling for elevated prices through mid-2026 even if flows resume later this year.

Global supply-demand balance remains in deficit mode for now:

Impact of UAE Leaving OPEC

In a major blow to the cartel, the United Arab Emirates announced its exit from OPEC (and OPEC+) effective May 1, 2026—after nearly 60 years of membership. As the third-largest producer (behind Saudi Arabia and Iraq), the UAE’s departure removes ~3–3.5 million b/d from the official OPEC baseline and strips the group of significant spare capacity.

Implications for remaining members: Weaker cartel cohesion: OPEC now has 11 members. The UAE cited a desire for flexibility in a “new energy age” and to ramp up output independently once the Hormuz situation stabilizes. This could add 1–1.5+ mb/d of extra supply long-term, pressuring prices downward post-crisis.

Greater burden on Saudi Arabia: As de facto leader, Riyadh faces increased pressure to manage quotas alone while its own output is crippled.

Potential fragmentation: Analysts note it could encourage other producers to reconsider membership if the group’s influence wanes.

UAE’s move is viewed by some as a strategic win for flexibility amid high global demand expectations.

Sanctions and Geopolitical Constraints on Key Members

U.S. financial controls remain a critical factor limiting full recovery for several producers: Venezuela: Sanctions on PDVSA were partially eased in March 2026 to unlock additional supply during the crisis, allowing limited U.S. company dealings and exports. However, core financial controls and restrictions on cash flows to the Maduro regime persist, capping upside.

Iraq: Production has plummeted amid the war. Recent U.S. Treasury sanctions (May 2026) targeted Iraq’s Deputy Oil Minister and Iran-backed militias for allegedly diverting Iraqi oil to benefit Iran, adding layers of scrutiny to its sector.

Iran: As a condition for any war-ending agreement, new or tightened U.S. controls on Iranian oil exports and revenues are widely expected, further constraining its ~3 mb/d output potential.

These overlays mean even a partial reopening of Persian Gulf routes may not immediately translate to pre-war production levels across OPEC.

Outlook

The Saudi production collapse underscores how geopolitics now dominates oil markets. With the UAE gone, OPEC’s ability to coordinate supply responses is diminished at a time when global inventories are being drawn aggressively. Remaining members will grapple with war recovery, sanctions, and the risk of higher non-OPEC supply flooding the market once disruptions ease.

Energy News Beat will continue monitoring the OPEC Monthly Oil Market Report and EIA data for updates on production rebounds and price trajectories.

Appendix – All Sources and Links

- Bloomberg: “Saudis Tell OPEC That Oil Output Sank Again to Lowest Since 1990” (May 13, 2026) – https://www.bloomberg.com/news/articles/2026-05-13/saudis-tell-opec-that-oil-output-sank-again-to-lowest-since-1990

- Reuters: UAE leaves OPEC (Apr 28, 2026) – https://www.reuters.com/markets/commodities/uae-says-it-quits-opec-opec-statement-2026-04-28/

- CNBC, Guardian, BBC coverage of UAE exit.

- EIA Short-Term Energy Outlook & OPEC Revenues Fact Sheet.

- MacroMicro OPEC Member Production Charts.

- IEA Oil Market Report (May 2026).

- U.S. Treasury OFAC announcements on Venezuela/Iraq sanctions (2025–2026).

- OPEC Annual Statistical Bulletin & Monthly Oil Market Reports (opec.org).

Data visualizations sourced from public MacroMicro and market analysis platforms for illustrative purposes.

The post Saudis Tell OPEC That Oil Output Sank Again to Lowest Since 1990 appeared first on Energy News Beat.