Energy News Beat

Wall Street banks are rapidly revising downward their oil price forecasts following the U.S.-Iran interim agreement to end hostilities, reopen the Strait of Hormuz, and ease restrictions on Iranian oil exports. The news has already triggered a sharp sell-off in crude prices, with Brent crude falling to around $80–81 per barrel as of June 16, 2026—down significantly from peaks above $100–120 during the height of supply disruptions earlier this year.

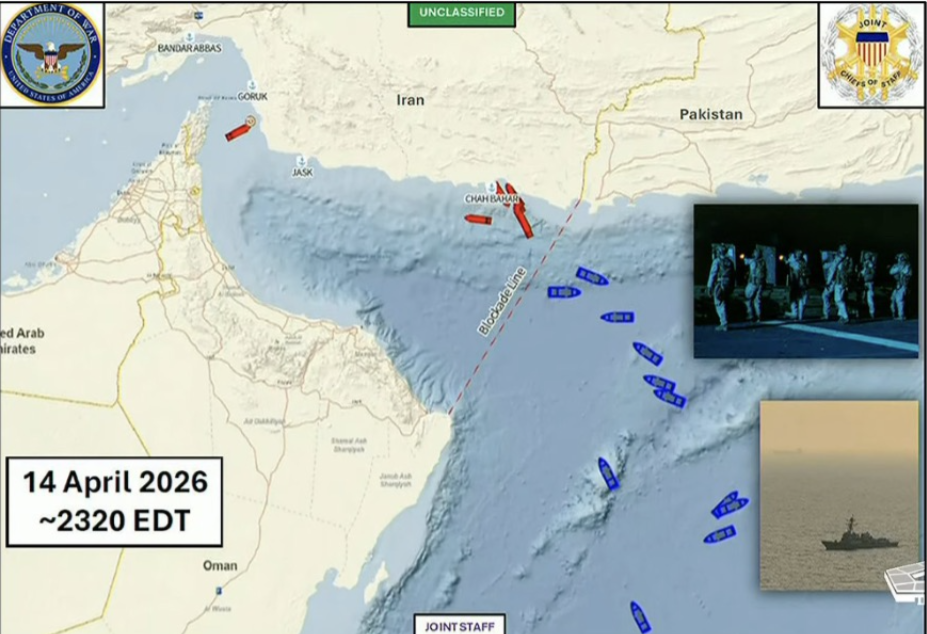

The breakthrough, announced over the weekend, involves a memorandum of understanding (MOU) that extends the current ceasefire, lifts the U.S. naval blockade on Iranian ports, and provides temporary waivers on oil sanctions during upcoming talks. A formal signing is expected around June 19, 2026, followed by a 60-day negotiation period covering Iran’s nuclear program, broader sanctions relief, and other issues. President Trump highlighted the potential for increased oil flows, stating variations of “Let the oil flow!”

Banks Cut Forecasts on Faster Supply Recovery

Major banks are betting that Persian Gulf oil supplies—accounting for roughly 20% of global trade through the Strait of Hormuz—will normalize more quickly than previously expected.

Morgan Stanley lowered its Brent crude forecast to an average of $90 per barrel in Q3 2026 (down from $100 previously) and sees $80 per barrel in Q4 2026.

Goldman Sachs cut its Q4 2026 Brent forecast to $80 per barrel (from $90) and its 2027 average to $75 per barrel (from $80). The bank now expects oil exports from the Persian Gulf to return to pre-war levels by the end of July 2026—one month earlier than its prior projection. It also revised its 2026 average Brent forecast lower, to around $85 per barrel in some updates.

Citi took an even more bearish stance, slashing its Q3 2026 Brent forecast to $75 per barrel and projecting an average of $70 per barrel in Q4 2026.

These revisions reflect reduced geopolitical risk premiums and expectations of rising Iranian oil exports once the strait reopens and temporary sanctions relief takes effect. Iran has been a major supplier to markets like China, and increased flows could add meaningful supply to global balances.

How Long Until Oil Markets Stabilize and Rebalance?

Oil markets have already reacted swiftly to the positive headlines, with prices dropping 4–5% or more in recent sessions. However, physical supply normalization and full market rebalancing will take longer than the initial price reaction.

Analysts and experts indicate that full stabilization could require weeks to several months:

Immediate (days to weeks): Price discovery and sentiment-driven moves as risk premiums unwind. Shipping insurance costs may remain elevated until security is assured.

Short-term normalization (1–2 months): Goldman Sachs projects Persian Gulf exports returning to pre-war levels by late July. Mine clearance, safe passage verification, and tanker operators resuming full operations are key hurdles. Some forecasts suggest ~80% of energy flows could resume by the end of Q3 2026.

Full rebalancing (2–6+ months): Actual ramp-up of Iranian production and exports takes time due to infrastructure, buyer arrangements, and logistics. Global inventories will adjust, and OPEC+ is likely to respond with production adjustments to prevent oversupply. The 60-day negotiation window adds uncertainty—if talks progress toward a final deal with sustained sanctions relief, supply could increase further; setbacks could reignite volatility.

Past geopolitical resolutions show that while futures markets price in changes quickly, physical flows and price equilibrium often lag by 1–3 months as the market digests new supply realities.

What This Means for Investors

Positive for broader markets: Lower energy costs ease inflation pressures, support consumer spending, and reduce the likelihood of aggressive monetary policy responses. Equity futures have rallied on the news, particularly in consumer-facing and cyclical sectors.

Challenging for the energy sector: Upstream oil producers, exploration & production companies, and energy majors face margin compression from lower realized prices. Energy stocks have already come under pressure. Investors may shift toward downstream refiners or integrated players less exposed to upstream volatility. Hedging strategies and positioning in oil futures will adjust rapidly.

Opportunities and risks: Reduced geopolitical premium could lower overall market volatility if the deal holds. However, the interim nature of the agreement and ongoing 60-day talks introduce execution risk. Long-term, sustained higher Iranian supply could pressure prices lower into 2027, favoring consumers of energy over producers. Diversified portfolios with exposure to non-energy sectors stand to benefit most in the near term.

What This Means for Consumers

The biggest near-term winner is the consumer. Lower crude prices translate directly to cheaper gasoline, diesel, and jet fuel at the pump. U.S. drivers are already seeing relief, with reports of falling retail fuel prices in some regions.

Globally, reduced energy costs help ease inflationary pressures on transportation, food (via fertilizers and logistics), and manufacturing. This provides breathing room for household budgets, particularly for lower- and middle-income families hit hardest by earlier price spikes. Airlines, shipping, and energy-intensive industries also gain cost relief, potentially supporting economic activity.

Longer term, if prices stabilize in a lower range (e.g., mid-$70s to low-$80s), it could support stronger global growth—but overly sharp or prolonged declines risk underinvestment in future supply, setting the stage for volatility later.

Risks and Outlook

The deal remains fragile. Full implementation depends on mine clearance, sustained safe navigation through the Strait of Hormuz, and progress in the 60-day talks. OPEC+ production decisions, global demand trends (especially in China), and any renewed tensions could override bullish supply expectations.

Markets are currently pricing in significant relief, but analysts caution against assuming a quick return to pre-war “normal.” Physical supply recovery and inventory dynamics will determine the new equilibrium.

Bottom line: The U.S.-Iran breakthrough marks a major de-escalation that is already reshaping oil price expectations. Banks are front-running faster supply recovery, consumers stand to gain at the pump, and investors are navigating a shifting energy landscape. The coming weeks and the 60-day negotiation period will be critical in determining how durable this relief proves to be.

- Original referenced article: Banks Slash Oil Price Forecasts After U.S.-Iran Breakthrough (OilPrice.com)

- Wall Street Journal coverage on bank forecasts: Wall Street Banks Slash Oil-Price Forecasts

- Investing.com summary of bank cuts: Banks Slash Oil Price Forecasts After US-Iran Breakthrough

- Bloomberg and other reports on Morgan Stanley/Goldman revisions (via aggregated sources)

- Context on U.S.-Iran deal and Strait of Hormuz: Reuters, CNN, Al Jazeera, The Guardian, AP News reports from June 14–16, 2026

- Oil price data and market reaction: Trading Economics, OilPrice.com futures, Yahoo Finance, and contemporaneous news (Brent ~$80–81/bbl as of June 16, 2026)

- Timeline and stabilization analysis: DW, AP News, Capital Economics commentary, and expert quotes on shipping/infrastructure recovery timelines

All information is current as of June 16, 2026. Oil markets remain highly dynamic—monitor official announcements on the signing and negotiation progress for updates.

The post Banks Slash Oil Price Forecasts After U.S.-Iran Breakthrough appeared first on Energy News Beat.