Energy News Beat

The AI boom has supercharged America’s data center industry, turning what was once a steady infrastructure play into one of the fastest-growing drivers of electricity demand in the country. Hyperscalers and AI startups are racing to build massive facilities packed with GPUs that devour power at unprecedented rates. From rural Texas fields to Virginia’s “Data Center Alley,” the land rush is on—and it’s reshaping energy markets, grids, and local economies in real time.

Current Landscape: Scale, Locations, and Power Draw

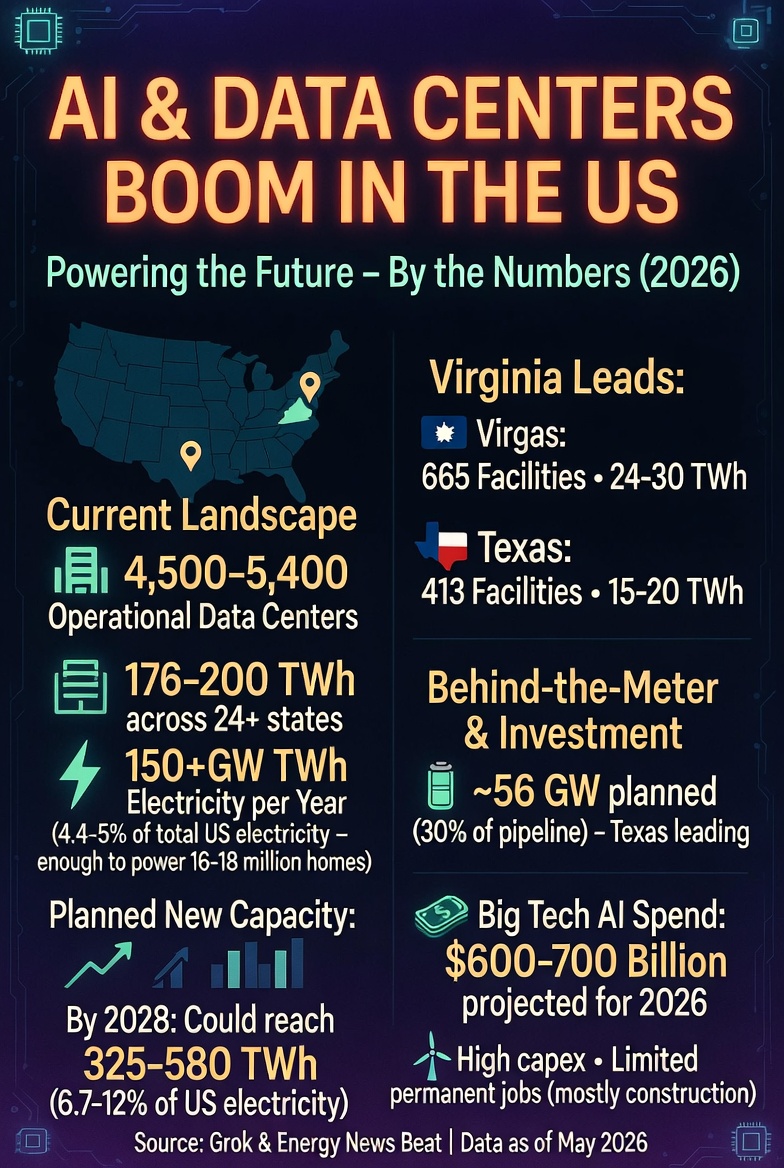

As of mid-2026, the United States is home to roughly 4,500–5,400 operational data centers. These facilities collectively consume about 176–200 TWh of electricity annually—roughly 4.4–5% of total U.S. electricity use, enough to power around 16–18 million homes. Average power demand sits in the 18–25 GW range, though peak loads are higher.

Virginia remains the undisputed king, with approximately 665 facilities (primarily in Loudoun County/Ashburn) consuming 24–30 TWh per year—more electricity than many entire states. Texas follows closely with around 413 facilities and 15–20 TWh, concentrated in Dallas-Fort Worth, Austin, San Antonio, and emerging West Texas hubs. Other major states include Illinois (244 facilities, ~12 TWh), California (321 facilities), and growing players in Georgia, Arizona, and the Midwest.

These numbers reflect legacy internet and cloud infrastructure, but AI workloads are dramatically changing the picture. A single large AI training run can consume as much power as hundreds of households, and inference (everyday AI use) keeps racks humming 24/7 at densities 3–5 times higher than traditional data centers.

The Buildout: Planned Projects, Power Plans, and Geographic Shifts

The pipeline is enormous. Planners have filed for over 150 GW of new data center power capacity across 24+ states, with thousands of projects in various stages. Virginia’s development pipeline could reach ~35 GW total capacity. Texas is close behind at ~27 GW and is projected to claim nearly 30% of national data center capacity by 2028 (exceeding 40 GW in ERCOT alone, up from ~8 GW today). Other hotspots include Pennsylvania, Georgia, Indiana, Arizona, New Mexico, and Utah.

By 2028, U.S. data centers could consume 325–580 TWh annually (6.7–12% of national electricity), according to Lawrence Berkeley National Laboratory analysis for the Department of Energy. Natural gas is expected to fuel much of the near-term growth, though many operators pledge eventual renewable matching or nuclear restarts.

Behind-the-Meter Boom: Bypassing the Grid

Grid interconnection delays have pushed many developers “behind the meter” (BTM)—building dedicated on-site generation (gas turbines, solar+battery hybrids, or even nuclear) directly tied to the load rather than waiting years for utility upgrades.

Cleanview’s February 2026 analysis identified 46 planned BTM data centers totaling ~56 GW—roughly 30% of the entire U.S. planned capacity. Ninety percent of these projects (≈50 GW) were announced in 2025 alone. Gas-fired generation dominates the near-term equipment mix, with renewables often slated for 2028+. Major BTM clusters are forming in gas-rich states: Texas leads, followed by New Mexico, Pennsylvania, Utah, and Wyoming.

Texas stands out as the most BTM-friendly environment thanks to ERCOT’s deregulated market, abundant pipelines, and fast permitting for on-site generation. However, Senate Bill 6 (signed June 2025) now imposes new rules on large loads (>75 MW): mandatory studies, potential curtailment during grid stress, cost-sharing for transmission upgrades, and disclosure of on-site backup. The goal is to prevent BTM projects from pulling existing grid resources offline or shifting costs to other ratepayers.

In contrast, many traditional regulated states (e.g., parts of the PJM region or California) have stricter interconnection rules, longer queues, and higher barriers to true BTM setups—driving developers toward Texas and similar markets. Exact nationwide BTM counts for operating facilities remain lower than planned, but the shift is accelerating.

The Land Grab: Business Opportunity or Consumer Caution?

Developers are snapping up rural land at premium prices—sometimes $100k+ per acre—often in unincorporated counties with cheap power access and fewer zoning fights. This “land grab” has sparked local moratoriums in places like Texas rural counties (Kerr, Hill, Somervell) over grid strain, water use (data centers can consume billions of gallons annually), and fears of stranded infrastructure.

For consumers and energy stakeholders, it’s a mixed bag:Opportunity: Massive capital inflow ($350–650B+ in AI/data center capex projected for 2025–2026 from Big Tech alone) is spurring new power generation, transmission upgrades, and jobs in construction, electrical trades, and energy services. Tax revenues are real—data centers often become the largest local taxpayers, and some projects deliver net savings to ratepayers when new generation spreads costs.

Caution: Permanent operational jobs are limited (often just dozens per facility—highly automated). Most employment is short-term construction. Electricity prices are rising in high-density areas (up to 76% wholesale spikes in PJM), and water/land impacts hit rural communities hardest. Many incentives reduce the net public benefit.

AI itself is creating high-skill tech and engineering jobs upstream, but data centers themselves are capital-intensive, not labor-intensive. Brookings and other analyses show 4–5% local employment growth in host counties over 5–6 years, largely from construction and indirect effects—yet long-term operational jobs taper off sharply.

Money Generated and Jobs Created

Big Tech’s combined AI infrastructure spend is projected to hit $600–700B in 2026 alone, with cumulative data center-related investment in the trillions by 2030. The broader industry contributed ~$162B in taxes (federal/state/local) in 2023. Yet direct permanent jobs remain modest relative to the scale—thousands nationally for operations, tens of thousands counting construction ripple effects.

The Accountability Question

AI without accountability is like a government without checks and balances. As data centers reshape the grid, policymakers, utilities, and communities must demand transparency on power sourcing, environmental impacts, ratepayer protections, and long-term economic returns. Texas’s SB6 is one model; other states are watching. Without balanced oversight—on emissions, water, land use, and cost allocation—the boom risks becoming a burden rather than a boon.

The AI data center surge is real, transformative, and here to stay. For the energy sector, it’s both a historic opportunity and a call for smart planning. Consumers and ratepayers deserve clear answers on who pays, who benefits, and how we keep the lights on for everyone.

- ElectricChoice.com U.S. Data Center Power Consumption Map (2026): https://www.electricchoice.com/datacenters/

electricchoice.com

- ElectricChoice.com Blog on Data Center Electricity (updated May 2026): https://www.electricchoice.com/blog/datacenters-electricity/

electricchoice.com

- LBNL/DOE 2024 United States Data Center Energy Usage Report (projections to 2028): https://eta-publications.lbl.gov/sites/default/files/2024-12/lbnl-2024-united-states-data-center-energy-usage-report.pdf (via energy.gov)

energy.gov

- Cleanview “Bypassing the Grid” BTM Report summary (Feb 2026): https://cleanview.co/content/power-strategies-report

cleanview.co

- Reuters on data center capacity plans (Jan 2026): https://www.reuters.com/business/energy/charting-data-center-development-roadmap-key-us-states-2026-01-22/

reuters.com

- Belfer Center / Harvard on AI & Grid (Feb 2026): https://www.belfercenter.org/research-analysis/ai-data-centers-us-electric-grid

belfercenter.org

- Texas SB6 / ERCOT regulatory updates (various 2025–2026 sources via Mayer Brown, PCI Energy, etc.)

- Brookings on data center employment effects (May 2026): https://www.brookings.edu/articles/new-evidence-on-data-center-employment-effects/

brookings.edu

- Additional context from PwC, S&P Global, EPRI, and state filings referenced across reports.

Data as of May 2026; the landscape evolves weekly. Energy News Beat will continue tracking these developments.

The post What is Going On with AI and Data Centers in the US? appeared first on Energy News Beat.