Energy News Beat

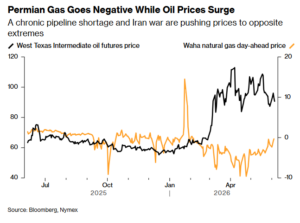

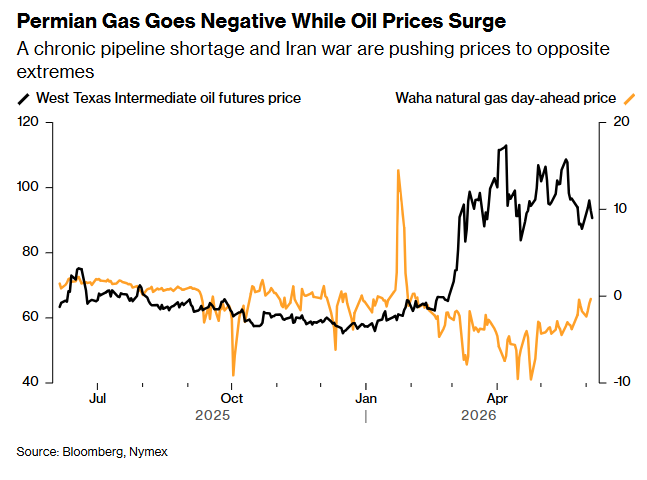

In the heart of America’s oil boom, a tale of two fuels is unfolding in the Permian Basin. While soaring crude prices fueled by the Iran war have oil producers celebrating record revenues, associated natural gas has become a costly burden. At the Waha Hub—the key pricing point for Permian gas—prices have now been negative for 124 consecutive days, forcing some drillers to pay buyers to take the gas off their hands. In response, major operators are shutting in high gas-to-oil ratio (GOR) wells to stem losses, even as oil production remains robust.

Oil vs. Gas: A Stark Contrast in Economics

Permian producers are reaping windfall profits from oil. West Texas Intermediate (WTI) crude has rallied sharply amid global supply concerns tied to the Iran conflict, recently trading near $90–$100 per barrel. Oil output in the basin remains near all-time highs, with the geographic Permian region producing roughly 6.7 million barrels per day (b/d) of crude and associated gas output hovering around 22–29 billion cubic feet per day (Bcf/d) in recent months, depending on tight shale vs. broader estimates.

Natural gas, however, tells a different story. As a byproduct of oil drilling, gas production has outpaced takeaway capacity for years. Waha spot prices hit a record low of -$9.60 per million British thermal units (MMBtu) in late April 2026 and have averaged deeply negative levels for much of the year—recently recovering only modestly to around -33 cents/MMBtu. This marks one of the longest streaks of negative pricing on record, driven by pipeline bottlenecks and seasonal maintenance.

The result? Gas-focused or high-GOR wells are unprofitable or cash-flow negative. Producers like Permian Resources Corp. and Devon Energy Corp. have already curtailed production from these assets. Permian Resources CEO James Walter called it a “no-brainer” on a recent earnings call: shut in the money-losing gas wells while oil economics remain strong.

Midstream players report 600–620 MMcf/d of price-related shut-ins in the Permian this spring, primarily from gas-centric operators—not the big oil-directed producers who can offset gas losses with crude revenues.

What’s Being Done: Short-Term Pain, Strategic Curtailments

Operators are prioritizing oil maximization. Oil wells continue producing because even with negative gas netbacks, the overall well economics remain positive at current WTI levels. Gas shut-ins are targeted and reversible—focused on high-GOR wells that generate disproportionate gas volumes. Flaring has also risen as a stopgap, though regulations and economics limit its use.

Longer term, the industry is betting on infrastructure relief and new demand centers rather than broad production cuts. Permian gas output growth is expected to moderate to about 4% annually in 2026–2027, but new pipelines and power demand could flip the script.

New Pipelines: Relief on the Horizon

The Permian’s chronic takeaway constraints are finally easing. Roughly 4.5 Bcf/d of new outbound pipeline capacity is scheduled to come online in 2026, with more projects following:Gulf Coast Express (GCX) Expansion (Kinder Morgan): ~0.57 Bcf/d, in-service 2Q 2026.

Blackcomb Pipeline (WhiteWater Midstream consortium): 2.5 Bcf/d to Agua Dulce/South Texas, targeted for 4Q 2026.

Hugh Brinson Pipeline (Energy Transfer): 1.5 Bcf/d Phase 1 to DFW (with potential Phase 2 expansion), early 3Q/4Q 2026 service.

Additional projects like the Apex Pipeline (2.0 Bcf/d to Port Arthur) and others could add another 7+ Bcf/d by 2027–2028. Analysts expect these additions to narrow the Waha-Henry Hub spread dramatically in the second half of 2026, reducing the frequency and severity of negative pricing.

Data Centers: A Game-Changing New Demand Sink

One of the most promising outlets for stranded Permian gas is the exploding AI data center boom in Texas. Hyperscalers need reliable, dispatchable power, and on-site gas-fired generation offers a solution that bypasses grid constraints.

Chevron is developing its first gas-powered data center complex in West Texas: initial 2.5 GW capacity, expandable to 5 GW, with first power targeted for 2027.

Pacifico Energy’s GW Ranch Project in Pecos County could deliver up to 7.65 GW of gas-fired power—the largest single power project in the U.S.—directly leveraging local gas supplies.

These “gas-to-power” and behind-the-meter projects turn excess associated gas into electrons for AI computing, creating a new local demand sink that doesn’t rely solely on pipelines to distant markets. Combined with LNG export growth and traditional power demand, data centers could absorb hundreds of MMcf/d of Permian gas in the coming years.

How Long Until Profitability Returns?

For oil-directed producers, the fields remain profitable today. Permian oil breakeven prices for new wells average around $67/bbl (Dallas Fed Q1 2026 survey), well below current WTI levels. Existing wells cover operating expenses at just $32–$47/bbl.

For gas-heavy or pure-play gas production, the timeline is tied to infrastructure:

Near-term (through summer 2026): Continued pressure and selective shut-ins are expected. Waha basis likely remains weak until new pipes ramp.

Late 2026 onward: Significant relief as ~4.5 Bcf/d of new capacity comes online. Forward curves show Waha converging toward Henry Hub pricing by year-end.

2027+: Full normalization is likely as additional pipelines, LNG feedgas demand, and data-center/gas-to-power projects come online. Some analysts warn of potential overbuild, which could keep basis discounts modest long-term.

In short, the Permian isn’t shutting down—it’s recalibrating. Oil keeps the lights on today; new pipes and data centers will make the gas pay again tomorrow.

Energy News Beat will continue monitoring Waha pricing, rig counts, and pipeline in-service milestones. Stay tuned for updates.

- Bloomberg – “Texas Gas Drillers Shut Out of Oil Price Rally Turn to Shutting Off Wells” (June 8, 2026): https://www.bloomberg.com/news/articles/2026-06-08/texas-gas-drillers-shut-out-of-oil-price-rally-turn-to-shutting-off-wells

- Financial Post / Bloomberg syndication (June 8, 2026): https://financialpost.com/pmn/business-pmn/texas-gas-drillers-shut-out-of-oil-price-rally-turn-to-shutting-off-wells

- Aegis Hedging – Permian Basin Gas Price and Fundamentals (recent updates through June 2026): https://aegis-hedging.com/insights/basis-brief-waha-gas

- Natural Gas Intelligence – “Why Permian Basin Natural Gas Prices Can’t Catch a Break” (March 17, 2026): https://naturalgasintel.com/news/why-permian-basin-natural-gas-prices-cant-catch-a-break/

- U.S. Energy Information Administration (EIA) – Permian tight oil & shale gas production updates (March 2026 STEO): https://www.eia.gov/todayinenergy/detail.php?id=67364

- East Daley Analytics & various midstream announcements on Blackcomb, Hugh Brinson, GCX Expansion (2025–2026 project timelines).

- Oil & Gas Watch / BusinessWire – Pacifico Energy GW Ranch Project & Chevron data center plans (Jan–Feb 2026): https://news.oilandgaswatch.org/post/massive-gas-powered-data-center-in-permian-basin-is-latest-in-string-of-texas-ai-computing-hubs

- Dallas Fed Energy Survey (Q1 2026) – Breakeven prices: https://www.dallasfed.org/research/surveys/des/2026/2601

- Additional context from Fortune, Hart Energy, and Enverus reports on Waha pricing and shut-ins (March–May 2026).

This article is for informational purposes and does not constitute investment advice.

The post Texas Gas Drillers Shut Out of Oil Price Rally Turn to Shutting Off Wells appeared first on Energy News Beat.