Energy News Beat

10 big stories on the Energy News Beat Stand Up

It is a wild day on the Energy News Beat Stand Up.

Make no mistake, time will tell if the Strait of Hormuz is open, but do not underestimate the importance that the Bank of London and Lloyds of London play in opening the Strait of Hormuz. They want the war to continue, and are not happy if the war ends.

As we hit Operational Bottoms for oil storage in the US it is a real problem, and President Trump ran out of time. I think that he has a plan and will get it done, but it will be done after the midterms.

President Trump at the G7 has had some major impacts on the news cycle.

1. Cushing, Oklahoma Oil Storage Crisis (Top Story)

The podcast opens with the critical issue that Cushing—the “pipeline crossroads of the world”—has hit operational tank bottoms with only ~21.64 million barrels of crude. This is a major concern because refineries may not be able to access the oil they need, and the situation could spike oil prices. Cushing is the primary delivery and pricing point for WTI (West Texas Intermediate) futures.

2. Global Oil Market Dynamics & Geopolitical Tensions

- Strait of Hormuz concerns: 20% of the world’s oil passes through this strait, creating vulnerability to disruptions

- Iran’s actions: Iran has pulled the trigger on controlling the strait, prompting neighboring Gulf states to seek alternative routes

- Tanker movements: Iranian super tankers are slipping through blockades, with 6 million barrels already moved (likely to China)

3. UAE’s Strategic Independence from Strait of Hormuz

The UAE is accelerating plans to bypass the Strait of Hormuz entirely by expanding pipelines from 1.7 to over 5 million barrels per day, with potential floating LNG terminals planned for the Gulf of Oman.

4. Alternative Pipeline Infrastructure

- Saudi Arabia’s east-west pipeline to the Red Sea (pumping ~7 million barrels/day)

- Plans to bypass the Suez Canal through the Mediterranean

- Iraq’s threat to close the Bab el-Mandeb Strait, forcing reliance on pipelines

5. Qatar’s LNG Export Restart

Qatar is preparing to restart LNG exports with tankers already positioned, which is critical for Europe’s natural gas supply (especially as they lag behind in summer refilling).

6. U.S. Power Grid Crisis

- Severe equipment shortage with power transformer lead times reaching 128 weeks (2.5 years)

- Some special orders taking up to 4 years

- New transformer facilities being built (Hitachi in Virginia by 2028, Siemens in North Carolina)

- Recommendation for homeowners to invest in solar panels and off-grid capabilities

7. California Energy & Infrastructure Problems

- Refinery closures: Only 7 refineries remain in California; losing one would spike gasoline, diesel, and jet fuel prices

- High-speed rail project: Ballooned from $9.9 billion to $231 billion with companies relocating to Morocco due to regulatory burden

- Port congestion: LA and Long Beach ports handling massive container volumes

8. Oil Price Forecasts

- Morgan Stanley lowered Brent crude forecasts to $90 in Q3 and $80 in Q4

- Current prices: WTI at ~$76-77, Brent at ~$79.58, Natural gas at $3.16

9. AI & Grid Infrastructure

Discussion of potential AI bubble concerns and the need for grid validation tools before implementation.

10. U.S. Reshoring & Industrial Recovery

The Trump administration is working to reverse decades of intentional deindustrialization, though the process faces challenges.

The podcast emphasizes that energy markets are at critical junctures with geopolitical tensions, infrastructure constraints, and strategic repositioning reshaping global oil and gas flows.

Cushing’s Central Role in Mixing, Blending, and Pricing

Cushing is far more than just storage. It serves as:

The primary delivery and pricing point for West Texas Intermediate (WTI) crude oil futures on the NYMEX. WTI is the main U.S. benchmark, and physical settlement/delivery occurs at Cushing.

A major blending and mixing hub. Different grades of crude from various U.S. basins are blended here to meet pipeline quality specifications, refinery requirements, or export standards. Low inventory levels complicate these blending operations.

The heart of the U.S. pipeline network connects Permian, Bakken, and other production areas to Midwest and Gulf Coast refineries and export terminals.

Low stocks at Cushing tighten physical supply signals, influence regional price differentials (e.g., WTI vs. Brent spreads), and affect the futures curve structure (contango or backwardation). This can curb record exports as arbitrage opportunities narrow and operational constraints bite.

2.Pain at the Pump: Can It Heal or Curse the Trump Administration?

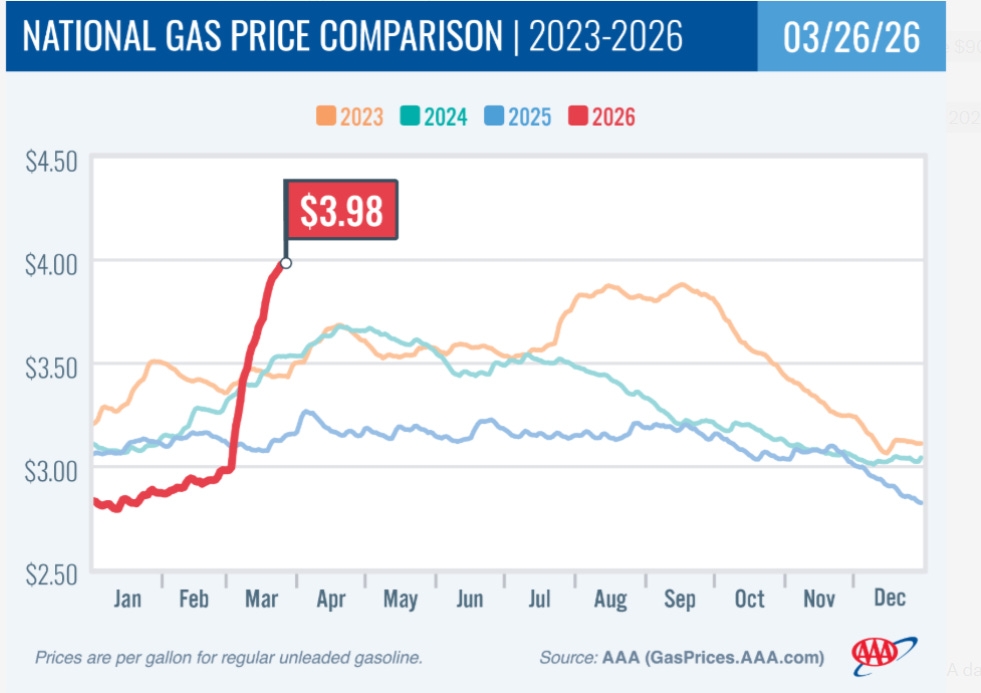

Gasoline prices at the pump are falling fast, offering consumers relief after months of pain. But this relief comes amid depleted strategic buffers and lingering uncertainty over the recent Iran conflict and deal. For the Trump Administration, the trajectory of energy prices could either reinforce its political standing or expose vulnerabilities.

Current Price Snapshot (Mid-June 2026)National averages have eased significantly from spring peaks:

Regular gasoline: $4.025 per gallon (AAA, June 17, 2026) — down ~13 cents from the prior week and nearly 49 cents from a month earlier. EIA reported $4.052/gallon as of June 16.

On-highway diesel: $5.059 per gallon (EIA, June 16, 2026).

Jet fuel: U.S. Gulf Coast spot prices around $3.37/gallon (early June); broader Argus US Jet Fuel Index near $2.80/gallon recently.

Brent crude has dropped to the $78–80 range (WTI below $76), down sharply from highs above $90–100+ earlier in the conflict period.

These declines follow a sharp spike tied to the escalation of U.S.-Iran tensions in late February 2026, which disrupted flows through the Strait of Hormuz.

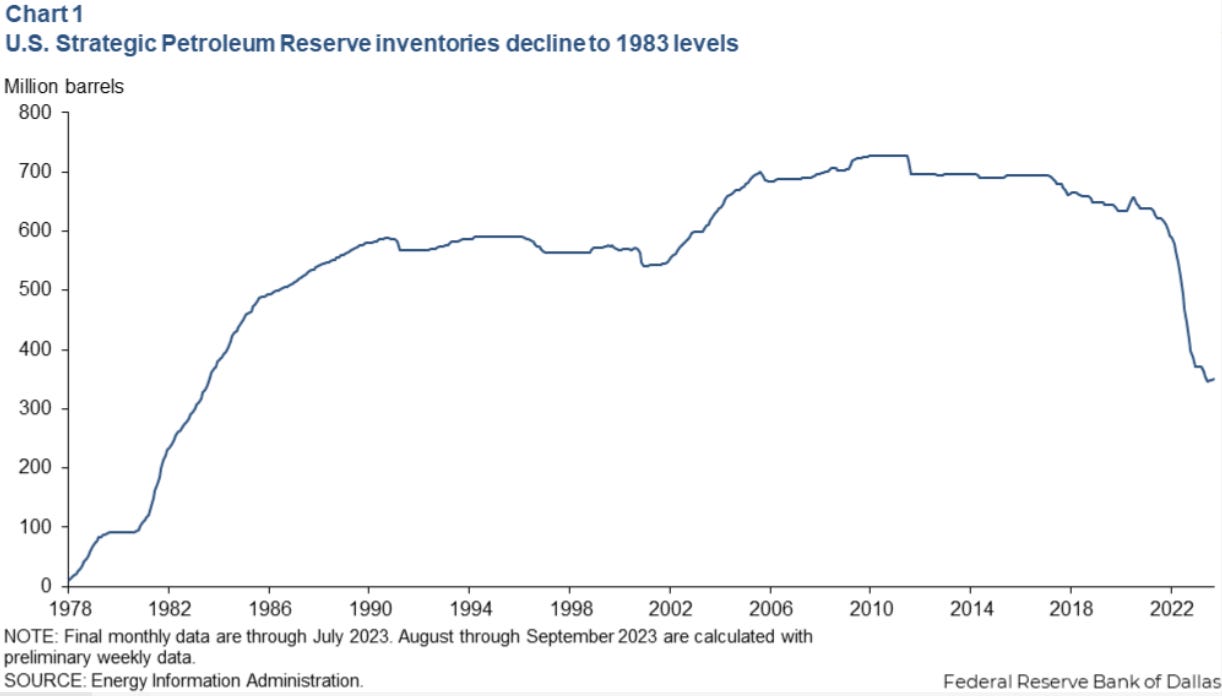

Inventory Levels Signal Tight Supply and Strong Demand

Key storage data reveals a market that has been drawing down buffers aggressively:

Strategic Petroleum Reserve (SPR): Stocks have fallen to approximately 340–349 million barrels — the lowest since 1983. Recent weekly drawdowns reached 8.9 million barrels as part of coordinated releases to ease prices. This follows earlier levels above 400 million barrels in 2026.

Figure: Long-term SPR inventory decline to historic lows.Cushing, Oklahoma (key delivery hub): Commercial crude stocks stood at about 21.64 million barrels as of June 5, 2026, continuing a multi-week decline (e.g., –801,000 barrels in the latest reported week).

3.UAE is moving on plans to never use the Strait of Hormuz

The United Arab Emirates is accelerating an ambitious strategy to achieve zero dependency on the Strait of Hormuz, one of the world’s most critical oil chokepoints. This comes amid recent regional tensions and a temporary closure of the strait following the Iran-US conflict earlier in 2026.

Bloomberg reports, citing an interview with UAE Minister of Foreign Trade Thani Al Zeyoudi, that the country is “moving toward having zero Hormuz dependency.” He emphasized: “We’re moving toward having zero Hormuz dependency and that’s regardless of whether it’s open or not. It’s going to open, and we hope that will happen quickly, but we will not stop the new plan.”

The UAE has had enough of vulnerability to geopolitical leverage and is building permanent infrastructure to reroute crude, refined products, and other energy flows away from the narrow waterway between Iran and Oman.

UAE’s Specific Plans: Ports, Pipelines, and Connectivity

The centerpiece is a major expansion of eastern ports on the Gulf of Oman (outside the Strait of Hormuz): Dibba, Fujairah, and Khor Fakkan. The UAE also plans to build at least one new harbor on its eastern coast.

Supporting this are:

- New pipelines connecting oil and gas fields to these ports.

- Expanded rail and road networks for better inland connectivity to petroleum facilities.

- Feasibility studies for consistent exports of petrochemicals, LNG, and other energy products.

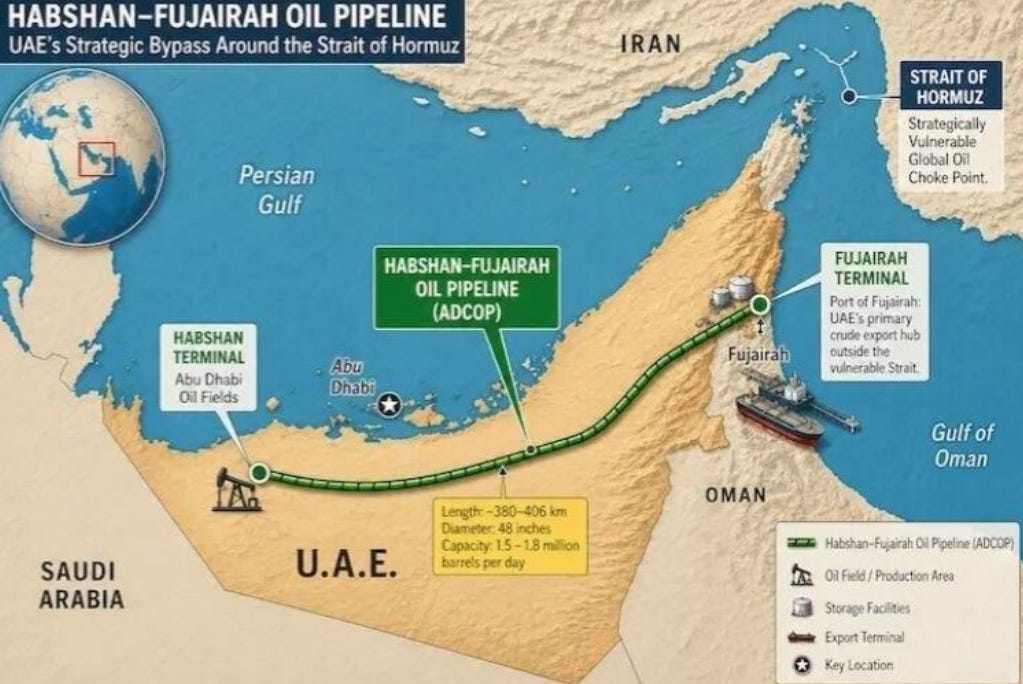

In May 2026, Abu Dhabi Crown Prince Sheikh Khaled bin Mohamed bin Zayed directed ADNOC to fast-track the West-East Pipeline project. This new pipeline will double crude export capacity through Fujairah by 2027.

The existing Abu Dhabi Crude Oil Pipeline (ADCOP / Habshan–Fujairah pipeline) — roughly 380–406 km long with a capacity of about 1.5–1.8 million barrels per day (mb/d) — has run at full capacity during recent disruptions. The new line will bring total bypass capacity through Fujairah to approximately 3.6 mb/d.

ADNOC is also evaluating a multi-fuel pipeline for refined products (gasoline, diesel, jet fuel) to further reduce reliance on tanker traffic through the strait.

These moves align with ADNOC’s broader goal of boosting production capacity while securing export routes.

UAE’s Habshan–Fujairah (ADCOP) pipeline provides a direct bypass from Abu Dhabi fields to Fujairah on the Gulf of Oman.

Regional Bypass Efforts: How Many Other Gulf Countries Are Involved?

While the UAE is the most vocal about achieving “zero dependency,” several neighbors are also advancing bypass infrastructure, though at different speeds and scales. The main active players are Saudi Arabia, the UAE, and Iraq. Kuwait, Qatar, and Bahrain remain heavily dependent on the strait with limited near-term alternatives.

Saudi Arabia

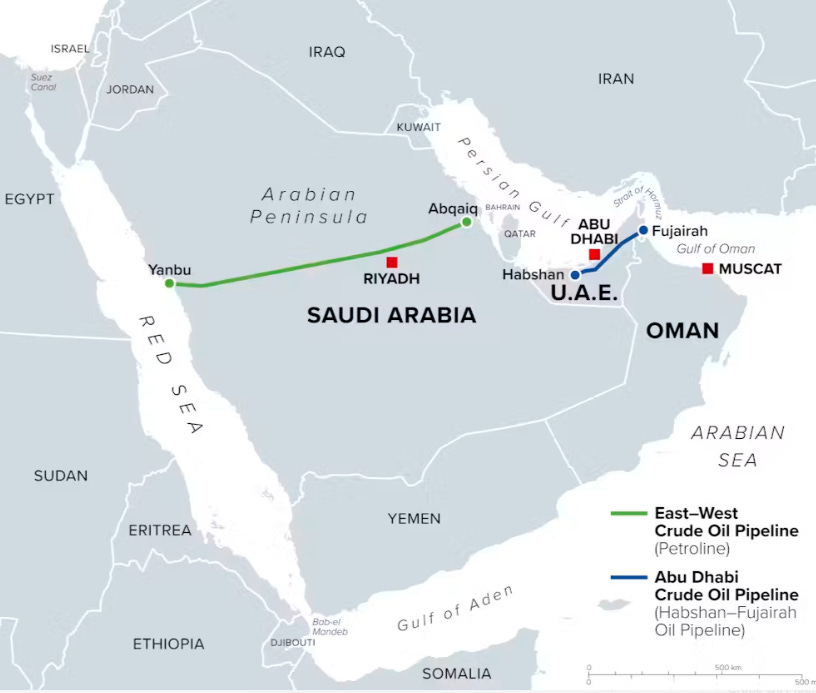

The kingdom operates the massive East-West Pipeline (Petroline / Abqaiq–Yanbu), a ~1,200 km route across the Arabian Peninsula to the Red Sea port of Yanbu. Design capacity: Up to 7 mb/d (after expansions and conversion of parallel NGL lines).

Recently restored to full pumping capacity during tensions, crude exports via Yanbu reached ~5 mb/d.

This is the largest existing bypass and has been a key resilience tool.

Saudi East-West Pipeline (Petroline) and UAE Habshan–Fujairah pipeline on a regional map.

Iraq

Iraq is fast-tracking alternatives for its southern oil (the bulk of exports, normally routed through the Strait via Basra). Key projects include: Basra–Haditha crude pipeline (target ~2.25–2.5 mb/d capacity) to link southern fields northward.

Expansion of the Kirkuk–Ceyhan pipeline to Turkey (Mediterranean), with plans to increase flows significantly.

Exploration of routes to Aqaba (Jordan, Red Sea) and Baniyas (Syria, Mediterranean).

Iraq has also accelerated exports via the Kurdistan–Turkey network. These efforts aim to create inland connections that bypass the southern maritime route.

Other Gulf states, Kuwait, Qatar, and Bahrain, currently have almost no major bypass infrastructure and depend almost entirely on the Strait of Hormuz. Some early discussions or long-term considerations exist (e.g., Kuwait in preliminary talks), but new pipelines would take years and billions of dollars.

Oman: Benefits from ports like Duqm on the Arabian Sea (outside the strait) and has natural geographic advantages for some flows.

Overall, a clear Gulf-wide push for resilience is underway, driven by recent strait disruptions. Combined bypass capacity from existing and planned Saudi/UAE/Iraqi routes is significant but still falls short of fully replacing the ~20 mb/d that typically transits the strait. Expansions are permanent infrastructure investments that will grow over time.

Iran’s Leverage and Long-Term Global Market Impact

Iran has historically used threats to close or disrupt the Strait of Hormuz as leverage in conflicts. The recent temporary closure (linked to the early 2026 tensions) did cause price spikes and supply concerns. However, several factors limit its long-term effectiveness on global markets:Bypass infrastructure is scaling rapidly — Saudi and UAE pipelines alone handled substantial volumes during disruptions. UAE’s doubling of Fujairah capacity and Saudi’s 7 mb/d route provide meaningful alternatives.

Global supply diversification — The US, Russia, other OPEC+ members, and non-OPEC producers can ramp up output. Strategic petroleum reserves (especially in the US and IEA countries) provide buffers.

Economic self-harm for Iran — Closing the strait also blocks Iran’s own oil exports and disrupts its economy, making sustained action costly.

Market adaptation — Recent events showed quick rerouting, higher utilization of bypasses, and price stabilization once partial flows resumed or alternatives kicked in. An interim Iran-US deal is already paving the way for reopening after mine clearance.

As UAE Minister Al Zeyoudi noted, the new plans continue “regardless of whether the Strait is open or not.” These investments make future Iranian threats less impactful because Gulf producers are structurally reducing vulnerability. Global oil markets have proven resilient; while short-term volatility remains possible, the era of easy chokepoint leverage is eroding as infrastructure diversifies.

4.Qatar Returns Tankers in Preparation for Restarting LNG Exports

6.Qatar Plans to Rapidly Restart LNG Output After Hormuz Opens – How will this impact Europe?

7.Banks Slash Oil Price Forecasts After U.S.-Iran Breakthrough

8.US Grid Equipment Shortage Deepens Impacting Repairs and New Installations

9.Another California refinery closure will threaten national and global economies

Great story from Ronald Stein and Mike Ariza. This is important.

Gov Newsom has yet again proved he is incompetent.

The California High-Speed Rail (CAHSR) project, once sold to voters as a transformative $33 billion bullet train connecting San Francisco to Los Angeles in under three hours by 2020, now carries eye-watering cost estimates that have ballooned dramatically. The latest figures from the California High-Speed Rail Authority’s (CHSRA) 2026 Draft Business Plan put the full original Phase 1 scope at approximately $231.3 billion in today’s dollars under legacy assumptions. Even an “optimized” version is pegged at around $126 billion, with full service potentially arriving around 2040.

After nearly two decades, billions spent, and minimal operational progress, the project stands as one of the most expensive and delayed infrastructure endeavors in U.S. history.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

Data2 if you have any business systems, can you trust A? Well, they have the patent on validation. . https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor.

The post Cushing at operational tank bottoms, and Strait of Hormuz updates appeared first on Energy News Beat.