Energy News Beat

The AI revolution is rewriting America’s energy landscape faster than anyone anticipated. Hyperscalers—Alphabet, Amazon, Meta, Microsoft, and others—are pouring more than $650 billion into data centers in 2026 alone, chasing the compute power needed to train and run next-generation AI models.

Yet a quiet crisis is threatening to derail the entire build-out: the United States still cannot manufacture enough of the basic electrical gear that every data center requires. Transformers, switchgear, and batteries—the unglamorous but essential hardware that steps down grid voltage, protects equipment, and smooths power spikes—are in critically short supply domestically. According to Bloomberg’s April 1, 2026 investigation, nearly half of the U.S. data centers planned to come online in 2026 are now expected to face delays or outright cancellation. Only about one-third of the roughly 12 GW of power capacity slated for 2026 is currently under construction.

The reason? Lead times for critical electrical equipment have ballooned to five years in some cases, forcing developers to turn to China—the very nation Washington is racing against in the AI arms race. Planned Data Centers: Where the Action Is (and Where It’s Stalling)Data-center development remains hyper-concentrated in a handful of states with cheap power, land, and fiber. Virginia’s “Data Center Alley” still leads, but Texas is closing the gap fast and could overtake it by 2030. Here’s the latest snapshot of power-capacity pipelines (planned + under-construction additions): Virginia: ~35 GW in development (an 11× increase over current levels)

Texas: ~27 GW

Pennsylvania: ~14 GW

Georgia, Louisiana, Wyoming: each >3 GW additional

Nationwide, more than 150 GW—and by some trackers up to 241 GW—of new data-center power capacity has been disclosed.

Number of data centers under construction (early 2026): Texas: 140

Virginia: 136

Georgia: 51

Ohio: 45

Arizona: 35

(and double-digit activity in more than a dozen other states)

High-profile examples include: OpenAI / Stargate campus in Abilene, Texas — 1.2 GW initial phase (enough electricity for ~1 million homes), already visible with massive electrical-wire spools and assembly tents.

Multiple hyperscale campuses in Northern Virginia, Dallas-Fort Worth, and emerging hubs in Pennsylvania, Ohio, and Wisconsin.

Yet many of these projects remain “on paper.” Sightline Climate data shows that of the 12 GW targeted for 2026 operation, only ~4 GW is actively under construction.

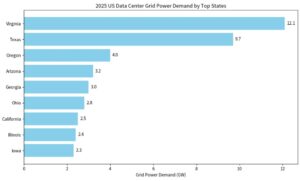

2025 Data Center Grid Power Demand by Top States (GW)

Projected U.S. Data Center Grid Power Demand (GW)

(Data: 451 Research / S&P Global; 2024 baseline approximated from trend lines.) The Electrical Bottleneck: Why China Still Holds the KeysTransformers alone tell the story. U.S. utilities imported more than 8,000 high-power transformers from China through October 2025—up from fewer than 1,500 for all of 2022. While Canada, Mexico, and South Korea remain larger overall suppliers, China’s share of specific high-voltage models hovers around 30 %. Battery imports from China exceed 40 %.

Domestic manufacturers cannot scale fast enough. Even major investments—GE Vernova’s $5.3 billion acquisition of Prolec and Siemens Energy’s $1 billion U.S. expansion—will take years to close the gap. Lead times that used to be 24–30 months are now routinely 5 years. One developer told Bloomberg: “If one piece of your supply chain is delayed, then your whole project can’t deliver.” Hyperscalers and smaller players like Crusoe are improvising: refurbishing old transformers from shuttered plants, building their own switchgear in modular “power distribution centers” that look like shipping containers, and pre-ordering equipment years in advance. But these work-arounds add cost and complexity.

Hyperscalers Are “Bringing Their Own Power”—But Even That Depends on Equipment

Facing grid-connection queues measured in years, the biggest tech companies have pivoted hard to onsite and dedicated generation. Microsoft, Google, Amazon, Meta, and Oracle have collectively announced dozens of gigawatts of new gas, nuclear (including SMRs and restarts like Three Mile Island and Duane Arnold), solar, wind, and storage projects. NextEra alone plans 15 GW (potentially 30 GW) of new generation tied to data-center hubs by 2035. Yet every new power plant—gas turbine, nuclear module, or solar farm—still needs the same transformers, switchgear, and batteries that are already back-ordered. The electrical-equipment crunch is not just a data-center problem; it is now a power-generation problem. Will the Build-Out Actually Happen?Short answer: Some of it will, but far slower than the market expects. Optimistic scenario (full domestic + allied supply-chain acceleration): 80–100 GW of new data-center load by 2030.

Base-case (current trajectory): 60–75 GW online by 2030, with significant delays pushing the rest into the 2030s.

Pessimistic scenario (trade restrictions tighten or China export controls hit): widespread cancellations and a material slowdown in U.S. AI leadership.

The irony is thick. America’s AI dominance rests, in part, on Chinese electrical parts—while China’s AI ambitions still rely on restricted U.S. chips. What Must Happen NextAccelerate domestic manufacturing — tax credits, streamlined permitting, and targeted DoE/DoD funding for transformer and switchgear plants.

Smart permitting for “Bring-Your-Own-Generation” — fast-track co-located gas, nuclear, and storage projects.

Strategic stockpiling and refurbishment programs — turn idle industrial assets into ready-to-deploy electrical infrastructure.

Bipartisan realism on trade — targeted tariffs that protect allies without choking the AI build-out.

The AI race is no longer just about chips or models. It is now a race to build the physical backbone—and the electrical supply chain that makes it possible. America’s energy future, and its technological edge, hinge on solving this bottleneck before the window of opportunity narrows further.

- Bloomberg: “America’s AI Build-Out Hinges on Chinese Electrical Parts” (April 1, 2026) – https://www.bloomberg.com/news/features/2026-04-01/us-ai-data-center-expansion-relies-on-chinese-electrical-equipment-imports

- 451 Research / S&P Global Market Intelligence – Data Center Services & Infrastructure Market Monitor (2025 updates)

- Sightline Climate & Cleanview data trackers (pipeline & construction status)

- JLL North America Data Center Report – Year-End 2025

- Visual Capitalist / Baxtel data on facilities under construction

- Lawrence Berkeley National Lab & EIA reports on data-center electricity consumption

- Company announcements: NextEra, Microsoft Community-First AI Infrastructure, Google/Kairos, Meta nuclear PPAs, etc.

- Wood Mackenzie transformer import analysis (cited in Bloomberg)

All data current as of early April 2026. Charts generated from aggregated public forecasts. Energy News Beat will continue tracking this critical intersection of AI, power, and supply chains. Stay tuned.

The post America’s AI Build-Out Hinges on Chinese Electrical Parts appeared first on Energy News Beat.