Energy News Beat

US refiners are operating plants at elevated run rates, with some delaying scheduled maintenance amid strong refining margins and steady-to-robust fuel demand. According to a Bloomberg report from June 1, 2026, the industry saw one of its lightest maintenance seasons in recent memory, with an average of only 470,000 barrels per day (bpd) of processing capacity offline from January through May—down significantly from 700,000 bpd the prior year and 900,000 bpd in 2024.

EIA data shows national operable refinery utilization reaching 94.5% for the week ending May 22, 2026 (up from 91.6% the previous week and 90.7% a year earlier), well above the long-term average around 89-90%. Gulf Coast (PADD 3) refineries—the heart of US capacity—have pushed even harder, hitting 98.0% utilization that same week, with multiple weeks in spring 2026 exceeding 95-97%.

Monthly figures for early 2026 fluctuated but peaked at 95.7% in December 2025.

This push to near-maximum levels is driven by favorable economics (including wide heavy-sour crude differentials benefiting complex Gulf cokers), healthy crack spreads, and strong export pull for diesel, gasoline, and other products amid global supply tightness.

US refined product exports have hit records or near-records in 2026, with diesel and gasoline shipments rising notably (e.g., diesel exports to Europe more than doubling in some periods).

Safety Risks and the Maintenance Question

A key question is whether sustained high utilization without adequate downtime creates developing safety issues. Refineries are complex, high-pressure/high-temperature operations handling flammable and corrosive materials. Regular turnarounds (planned major maintenance every 3-5 years on key units) are essential for inspecting pipes, vessels, and equipment, replacing worn parts, and preventing failures like corrosion-induced leaks, mechanical breakdowns, or fires/explosions.

Delaying maintenance to capture profits can increase risks of unplanned outages, equipment stress, and incidents. Industry analyses note that high utilization periods have historically correlated with elevated operational strain. A Marsh report on hydrocarbon losses observed that sustained high US refinery utilization (e.g., near peaks seen post-2017) can contribute to larger losses when combined with inadequate preparation.

Public incident data suggests refinery fires and explosions have increased since around 2018-2020 in some analyses, with reports of tripling or quadrupling in certain periods compared to prior baselines—though industry process safety metrics sometimes show mixed or improved trends depending on the dataset.

Notable historical context includes major incidents often tied to startups after maintenance or stressed operations, such as the 2005 BP Texas City explosion (15 killed during unit restart) and others like Chevron Richmond (2012, corroded pipe) or various Texas events linked to maintenance lapses or high ops.

Texas refineries, in particular, have a documented history of incidents attributed to safety violations, human error, and deferred maintenance.

While direct causation with “longer peak runs” isn’t universally quantified in every report, the consensus in safety reviews is that pushing utilization near 95%+ for extended periods without proportional maintenance heightens cumulative risk.

Recent lighter turnaround seasons and potential deferrals amid strong margins amplify this concern, especially with some forecasts noting heavier maintenance cycles potentially hitting in H2 2026 or later after lighter periods.

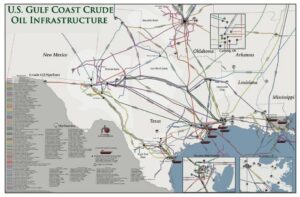

Which Refineries Are Running the Hardest? Volume and Exports

The US Gulf Coast dominates, with PADD 3 holding the majority of capacity and frequently showing the highest utilization (recently approaching 98%). Largest facilities by operable crude distillation capacity include:

Marathon Galveston Bay, Texas (~631,000 bpd)

Motiva (Saudi Aramco) Port Arthur, Texas (~626,000 bpd)

ExxonMobil Beaumont, Texas (~609,000 bpd)

Marathon Garyville, Louisiana (~597,000 bpd)

Other major players: Valero facilities, PBF Energy sites (e.g., Torrance, Chalmette, Delaware City), Phillips 66, and others. Top companies by total US capacity are Marathon Petroleum, Valero, ExxonMobil, Phillips 66, and PBF.

These export-oriented, complex refineries (with coking and heavy processing capability) are best positioned for current conditions, processing discounted heavy/sour crudes and exporting surplus products. High Gulf runs directly support the record US product export volumes seen in 2026.

Note that overall US capacity has seen net reductions from closures/conversions (e.g., impacts from LyondellBasell Houston, California sites like Valero Benicia planned idle, Phillips 66 LA), which concentrate volume on remaining plants and support higher utilization rates.

What Should Investors Look For?

Investors in refining stocks (e.g., MPC, VLO, PSX, PBF) or related plays should monitor:

Utilization and runs data — Weekly EIA reports for national/PADD trends and signs of forced high ops.

Maintenance schedules and announcements — Delayed turnarounds or rising unplanned outages signal near-term profit but longer-term risk.

Margins and cracks — Especially diesel/gasoline cracks and heavy-light differentials; healthy levels sustain runs but volatility looms with potential H2 maintenance or global shifts.

Export and inventory trends — Record exports are a tailwind, but domestic inventory draws (e.g., low diesel/jet) could pressure prices or invite policy scrutiny.

Safety/reliability metrics — Incident reports, OSHA fines, flaring data, and company disclosures on reliability capex. Prolonged high utilization without catch-up maintenance is a red flag.

Company-specific factors — Gulf Coast exposure (advantageous now), complexity (coking advantage for heavy crudes), and balance sheets for handling volatility or capex.

Broader risks — Refinery closures reducing buffer capacity, geopolitical export drivers, and potential seasonal or weather disruptions.

Refiners have benefited from capacity discipline and export strength, but the sector remains cyclical. High utilization boosts near-term earnings but requires vigilant risk management.

In summary, US refiners are capitalizing on strong conditions by running hard and exporting aggressively. However, the lighter maintenance backdrop raises legitimate questions about accumulating safety and reliability risks, echoing patterns where extended peak operations have coincided with higher incident potential. Investors should balance the attractive margins against sustainability indicators to assess whether current runs represent peak opportunity or emerging vulnerability.

- Bloomberg article (June 1, 2026): https://www.bloomberg.com/news/articles/2026-06-01/us-crude-refiners-are-pushing-run-rates-to-maximum-levels?srnd=phx-industries

- YCharts/EIA utilization data: https://ycharts.com/indicators/us_operable_crude_oil_distillation_capacity

- EIA Refinery Utilization and Capacity: https://www.eia.gov/dnav/pet/pet_pnp_unc_dcu_nus_m.htm

- Kpler blog on refinery runs: https://www.kpler.com/blog/whats-sustaining-the-strength-in-us-refinery-runs

- EIA Gulf Coast (PADD 3) data: Relevant weekly/monthly series (e.g., via eia.gov links provided in results)

- Export-related: EIA Today in Energy and other reports (e.g., https://www.eia.gov/todayinenergy/detail.php?id=67184)

- Incident history/safety: Various including CSB reports, legal summaries, Marsh 100 Largest Losses, and analyses from 2025-2026 on trends (e.g., Arnold & Itkin references in results)

- Refinery rankings/capacities: EIA, Wikipedia summaries, company sites, Oilsands Magazine, etc.

- Investor/maintenance outlook: Industrial Info, RBN Energy, BIC Magazine, etc.

All data drawn from publicly available sources as of early June 2026. Markets move quickly—verify latest EIA releases for real-time decisions. This article is for informational purposes and not investment advice.

The post US Crude Refiners Are Pushing Run Rates to Maximum Levels: Safety Concerns, Maintenance Trade-offs, Export Boom, and Investor Implications appeared first on Energy News Beat.