Energy News Beat

Gasoline prices at the pump are falling fast, offering consumers relief after months of pain. But this relief comes amid depleted strategic buffers and lingering uncertainty over the recent Iran conflict and deal. For the Trump Administration, the trajectory of energy prices could either reinforce its political standing or expose vulnerabilities.

Current Price Snapshot (Mid-June 2026)National averages have eased significantly from spring peaks:

Regular gasoline: $4.025 per gallon (AAA, June 17, 2026) — down ~13 cents from the prior week and nearly 49 cents from a month earlier. EIA reported $4.052/gallon as of June 16.

On-highway diesel: $5.059 per gallon (EIA, June 16, 2026).

Jet fuel: U.S. Gulf Coast spot prices around $3.37/gallon (early June); broader Argus US Jet Fuel Index near $2.80/gallon recently.

Brent crude has dropped to the $78–80 range (WTI below $76), down sharply from highs above $90–100+ earlier in the conflict period.

These declines follow a sharp spike tied to the escalation of U.S.-Iran tensions in late February 2026, which disrupted flows through the Strait of Hormuz.

Inventory Levels Signal Tight Supply and Strong Demand

Key storage data reveals a market that has been drawing down buffers aggressively:

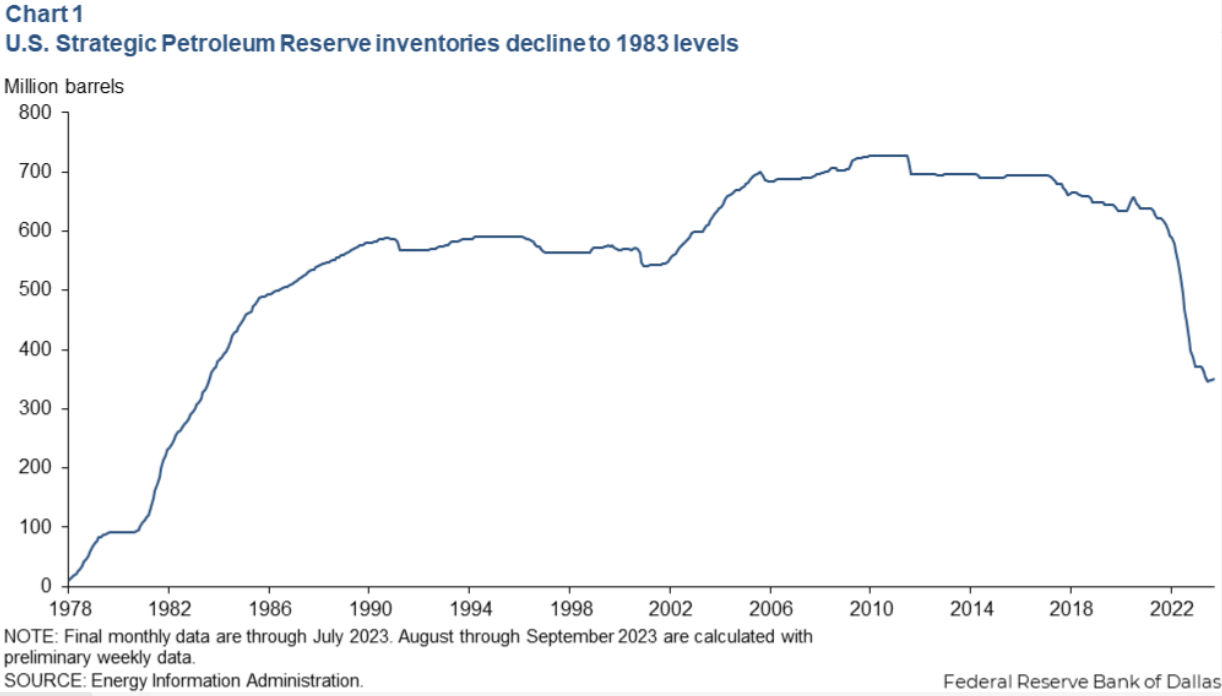

Strategic Petroleum Reserve (SPR): Stocks have fallen to approximately 340–349 million barrels — the lowest since 1983. Recent weekly drawdowns reached 8.9 million barrels as part of coordinated releases to ease prices. This follows earlier levels above 400 million barrels in 2026.

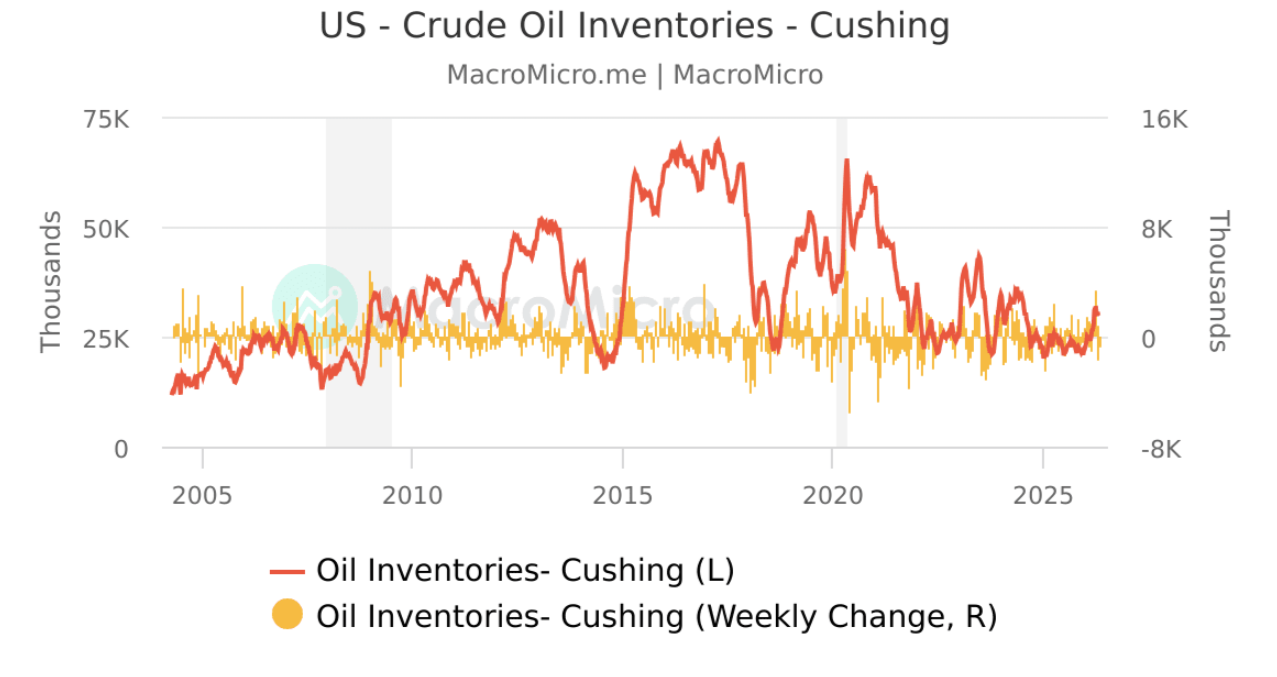

Figure: Long-term SPR inventory decline to historic lows.Cushing, Oklahoma (key delivery hub): Commercial crude stocks stood at about 21.64 million barrels as of June 5, 2026, continuing a multi-week decline (e.g., –801,000 barrels in the latest reported week).

Figure: Cushing crude oil inventory trends (recent levels in the low-to-mid 20,000s thousand barrels range with ongoing draws).Broader U.S. and global inventories (EIA): Commercial crude oil inventories fell 7.2 million barrels in the week ending June 5 to 426.5 million barrels (below five-year averages). This marked the seventh consecutive weekly draw. Refinery utilization hit a high 95.3%, with strong runs supporting gasoline and distillate production. Gasoline and distillate stocks showed mixed builds but overall tight conditions. OECD inventories are on track for multi-decade lows due to conflict-related supply gaps.

These drawdowns reflect strong underlying demand (refining, exports, and domestic consumption) pulling against disrupted global supply. No major demand destruction occurred even at peak prices. The result: a market with thin buffers that can amplify price moves in either direction.

Healing Potential for the Trump Administration

Falling prices deliver tangible relief to American drivers and businesses during the summer driving season. Lower energy costs ease inflationary pressures, support consumer spending, and align with long-standing priorities on affordable energy.

As highlighted in a recent analysis by Mario Nawfal: “Cheap gas could make the whole world forget the Iran war ever happened.” Historical precedents (e.g., post-2022 Russia-Ukraine shock) show that sharp price drops allow geopolitical events to fade from public memory quickly. Drivers absorbed higher costs without major behavioral shifts, and rapid relief reinforces positive sentiment.

For the administration, sustained declines toward or below pre-conflict levels could be credited as effective crisis management and energy leadership — a clear political win heading into future cycles.

Curse Risk: A Hiccup in the Iran Situation

The downside is real and immediate. Recent developments around the Iran agreement (signed around mid-June) include Iran rejecting aspects of a published MoU text, with the full agreement reportedly not being released publicly as initially indicated. Any renewed tensions, incomplete restoration of flows through the Strait of Hormuz, or delays in supply recovery could trigger rapid price rebounds.

With the SPR already at multi-decade lows and commercial/Cushing stocks depleted, the market has limited cushion. A supply shock could produce a quick “bump” at the pump — higher gasoline, diesel, and jet fuel prices that reignite inflation concerns and public frustration. This would likely draw intense scrutiny to the administration’s handling of the conflict and diplomacy.

Bottom Line

Current trends favor healing: Prices are dropping, inventories show the market clearing excess demand, and relief is reaching consumers. However, the combination of low strategic reserves and geopolitical fragility means the situation remains volatile. A smooth resolution and continued supply recovery would strengthen the administration’s position. Any significant hiccup risks turning pain at the pump into a political liability once again.

Energy markets are watching the barrels — and the headlines — closely.

- Mario Nawfal X post (June 17, 2026): https://x.com/MarioNawfal/status/2067238334334750827

- AAA National Average Gas Prices (June 17, 2026): https://gasprices.aaa.com/

- EIA Gasoline and Diesel Fuel Update (data as of June 16, 2026): https://www.eia.gov/petroleum/gasdiesel/

- Reuters: U.S. SPR falls to lowest since 1983 (June 15, 2026): https://www.reuters.com/business/energy/stocks-oil-us-strategic-petroleum-reserve-falls-lowest-since-1983-2026-06-15/

- EIA Weekly Petroleum Status Report (week ending June 5, 2026; released June 10): https://www.eia.gov/petroleum/supply/weekly/

- EIA Cushing, OK crude stocks data: https://www.eia.gov/dnav/pet/pet_stoc_wstk_dcu_ycuok_w.htm

- Additional context: Trading Economics, Macrotrends, YCharts, and contemporaneous reporting on Brent/WTI prices and Iran developments (June 2026).

All data current as of mid-June 2026. Prices and inventories can shift rapidly with new EIA releases or geopolitical events.

The post Pain at the Pump: Can It Heal or Curse the Trump Administration? appeared first on Energy News Beat.