Energy News Beat

But it’s not in housing; it’s spread across much of the economy. And it’s not just the end of the temporary GST (goods & service tax) holiday.

By Wolf Richter for WOLF STREET.

Inflation has a tendency to dish up nasty surprises, and it did that in Canada today for February, on top of the nasty surprises for January and December.

I’ll just walk briefly through some of the key numbers, and then I’ll post the commentary from the Economics and Strategy shop at the National Bank of Canada, the sixth largest bank in Canada, where the frustration with this mess bleeds through thickly, right from the beginning of their discussion: “The data published this morning by Statistics Canada is enough to shake observers’ convictions about the inflation situation in the country.”

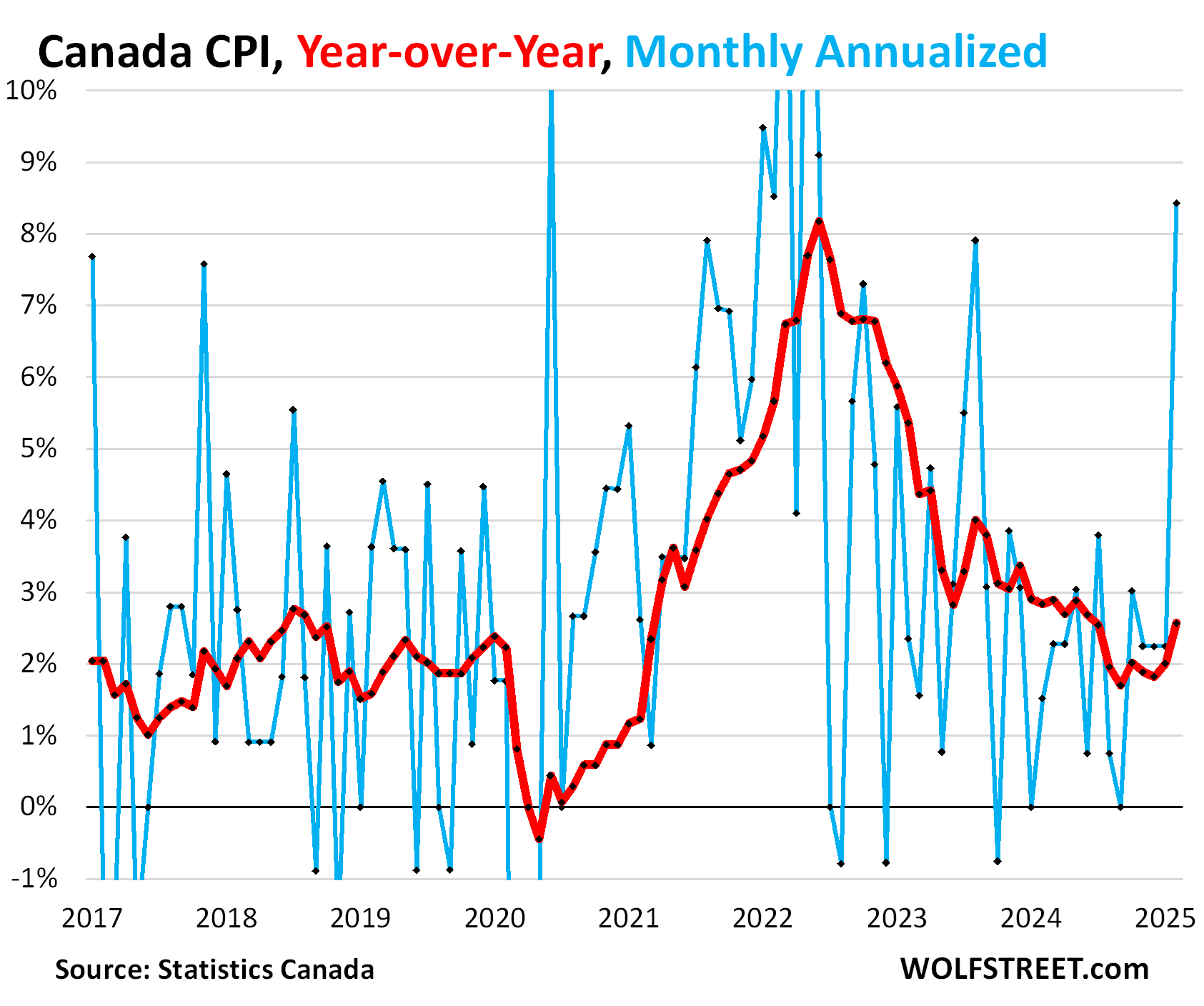

Canada’s overall Consumer Price Index spiked by 0.68% in February from January (8.4% annualized), seasonally adjusted, the worst month-to-month spike since the heady days of June 2022, and way above expectations (blue). The year-over-year CPI rose by 2.6%, the worst increase since July last year (red).

The month-to-month price increases in February were hot to red-hot in 6 of 8 major categories, but were cool in the housing components (shelter) and transportation, which includes gasoline.

In order of month-to-month inflation magnitude:

- Food: +2.04% (+27% annualized)

- Alcohol & tobacco: +1.66% (+22% annualized)

- Recreation & education: +1.16% (+15% annualized)

- Household operations & furnishings: +0.46% (+5.7% annualized)

- Health & personal care: +0.33% (+4.0% annualized)

- Clothing & footwear: +0.32% (+3.9% annualized)

- Shelter: +0.16% (+1.9% annualized)

- Transportation: +0.11% (+1.3% annualized).

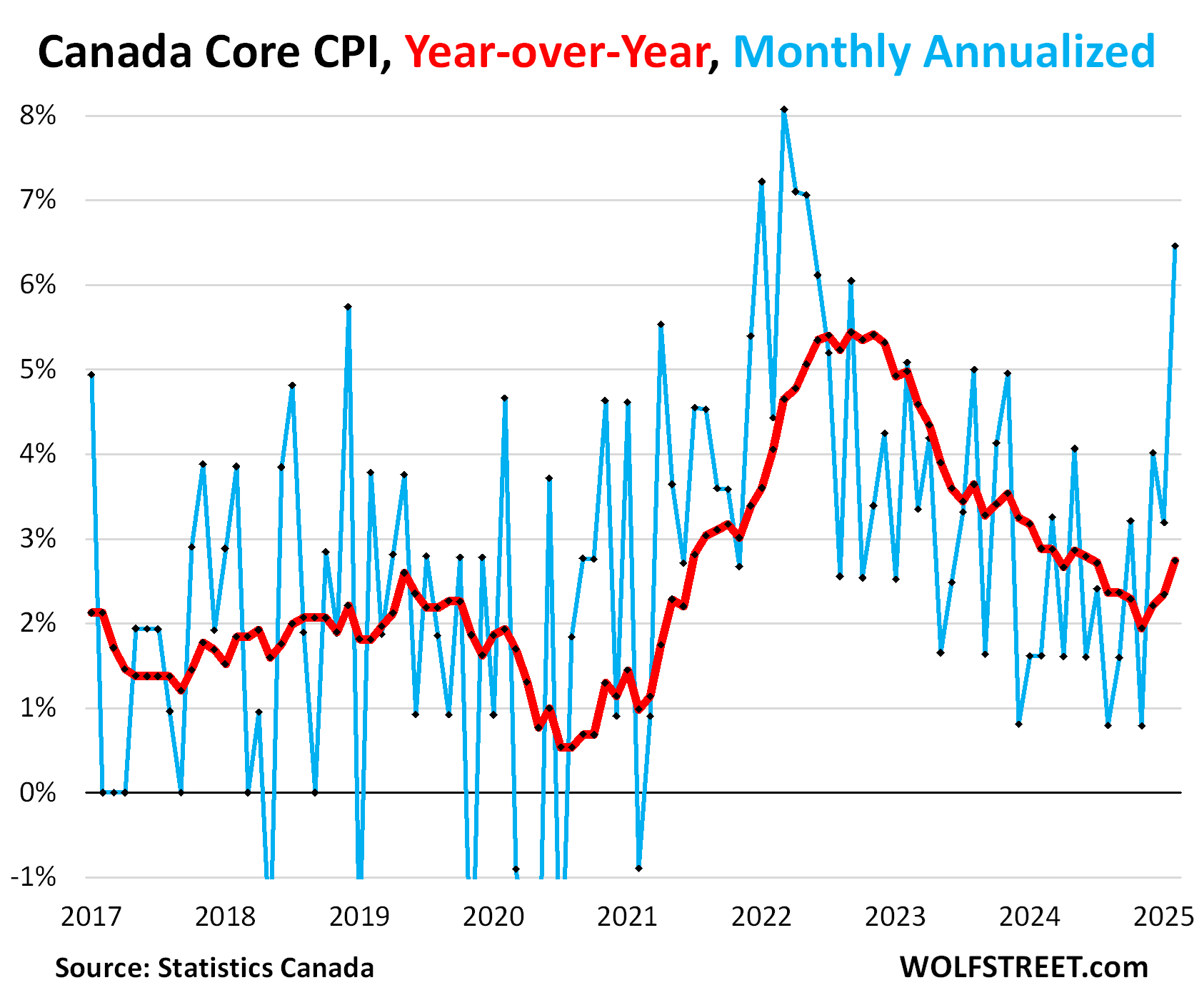

“Core” CPI, which excludes the food and energy components to track underlying inflation, spiked by 0.52% in February from March (6.5% annualized), the worst increase since June 2022, after the already expectation-busting increases in December and January (blue in the chart below).

This pushed the year-over-year increase to 2.74%, the worst increase since June 2024, and the third month in a row of acceleration (red):

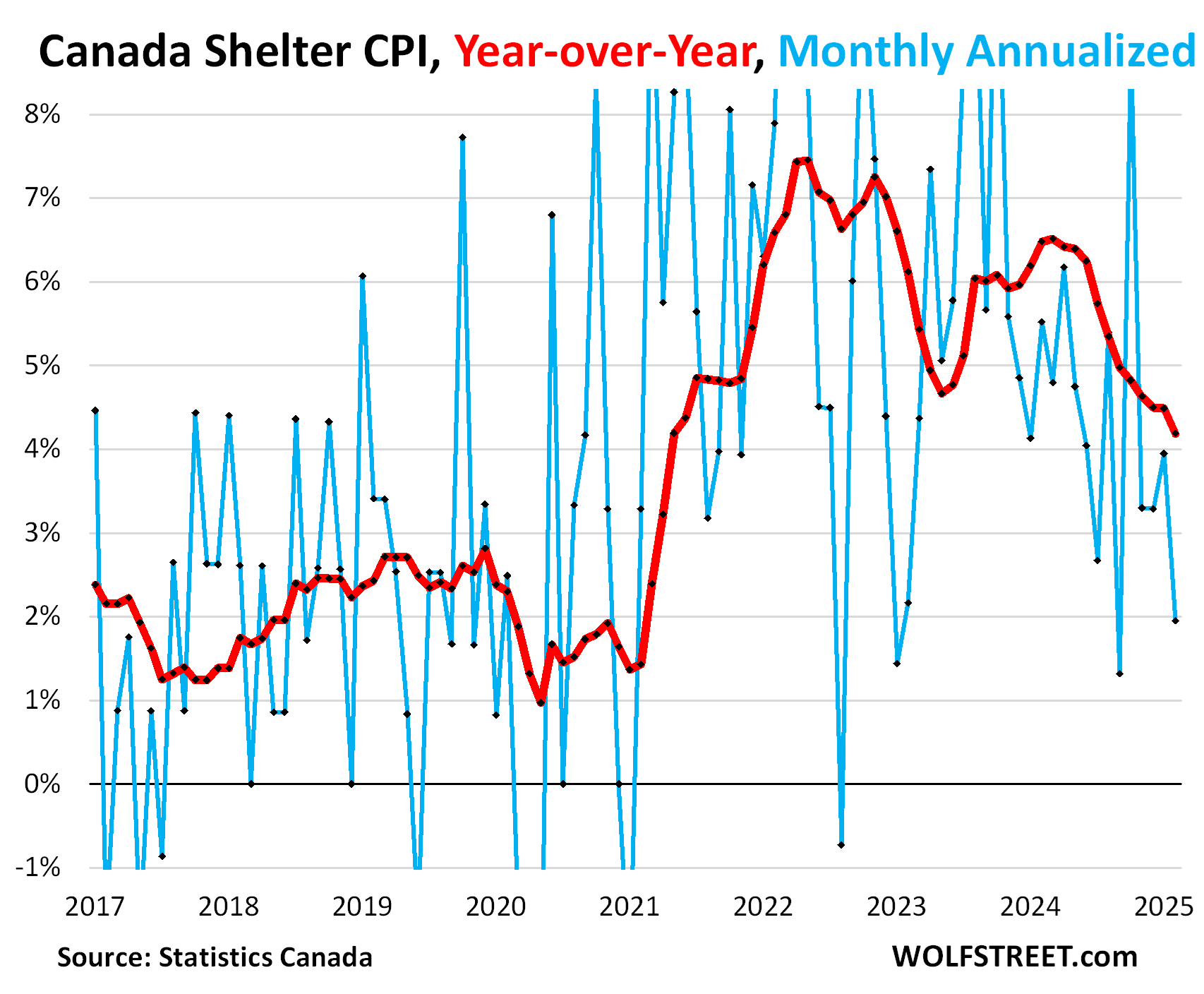

But it’s not the housing components that pushed up CPI this time. The CPI for shelter, which includes a collection of different housing expenses, decelerated further, and rose only 0.16% in February from January (1.9% annualized), roughly back in the middle of the range before the pandemic (blue).

The year-over-year shelter CPI decelerated to an increase of 4.2% (red):

So here is the frustrated commentary from the Economics and Strategy shop at the National Bank of Canada:

“The data published this morning by Statistics Canada is enough to shake observers’ convictions about the inflation situation in the country.

An acceleration of inflation was certainly inevitable in February with the end of the GST [goods and services tax] holiday in the middle of the month, which will also have an upward impact in March.

To get a more accurate picture of the situation, we have been focusing on inflation measures excluding indirect taxes for some months now. In February, the CPI excluding indirect taxes increased by a whopping 0.4% and the annual rate is now 2.9%, which is close to the upper limit of the Bank of Canada’s target range.

On an annualized three-month basis, this measure stands at 5.1%, its highest rate since September 2023.

There are certainly specific factors to mention, notably travel tours surging (+23% y/y). But that does not mean that inflation was not widespread in February, as evidenced by the central bank’s preferred core inflation measures, which have been growing at rates of 0.3% m/m and annualized rates that exceed the Bank of Canada’s target range over the past three months (CPI-Median at 3.4% and CPI-Trim at 3.3%).

We have repeatedly argued that these measures were skewed upwards by the housing component and that care should be taken in their use. But this was no longer the case in February, as monthly inflation in the housing sector had essentially returned to its historical average during the month.

This bias led us, as well as the central bank, to focus on the diffusion recently, which is not a concern over a year but is enough to raise eyebrows over the last three months with no less than 35 components moving above the target of 2.0% at an annualized rate (average 1999-2019 at 27).

There is no doubt that the Bank of Canada was surprised by the recent price developments in a context where the economy had started to improve.

In such a context, there is a strong chance that the rate cut we were expecting in April will not materialize unless the economy deteriorates very rapidly in a context of tariff uncertainty.

It remains that inflation is a lagging indicator, and the central bank may once again focus on economic variables that could weaken rapidly in the coming months if there is no improvement in trade relations with the United States. That scenario would justify lower path for the policy rate.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Not Just in the US: Inflation Dishes Up Another Nasty Surprise in Canada, Throwing Further Rate Cuts into Doubt appeared first on Energy News Beat.