Energy News Beat

Europe is staring down a structural gas deficit heading into the critical summer refill season. Storage levels sit near historic lows, Russian pipeline flows have all but vanished, and Middle East LNG supply disruptions (triggered by the ongoing Strait of Hormuz constraints since late February) have forced buyers to scramble for every available cargo—primarily from the United States.

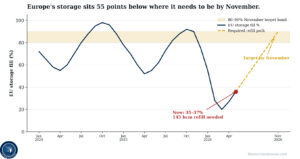

As highlighted in today’s Substack post from The Merchant’s News by Giacomo Prandelli, this crisis has directly repriced 8 of his 12 portfolio positions—all tied to the U.S. LNG value chain supplying Europe. The author reports these positions are up an average of +12.4% since the latest European developments, with the thesis not just intact but reinforced. U.S. LNG exports have hit records near 20 Bcf/d, while Europe’s storage sits around 30-36% full (well below the 5-year average and the 80-90% November target).

Prandelli’s core observation: Europe has no easy alternatives. Russian pipeline gas collapsed from 165 bcm (2019) to roughly 20 bcm (2025). U.S. LNG deliveries to the EU surged from 5 bcm to 81 bcm over the same period. Projections from IEEFA suggest the U.S. could supply up to 80% of EU LNG imports by 2030, backed by the EU-U.S. trade framework committing ~$750 billion in American energy purchases through 2028.

The math is brutal for Europe: low ending-winter storage (e.g., Dutch at ~5.8%, Germany ~20%, France ~27% earlier in the season), backwardated TTF contracts (summer prices higher than winter), and Asian buyers competing aggressively for non-Middle East cargoes. Equinor has publicly modeled TTF prices reaching €90/MWh if Hormuz constraints persist another 1-3 months—well above the 2022 crisis peak.

Current TTF front-month prices hover around €46/MWh (as of late May 2026), elevated but volatile amid ongoing geopolitical risks.

The U.S. LNG Value Chain Is the Clear Winner

The 8 repriced positions in Prandelli’s book span the full LNG supply chain to Europe:The largest U.S. LNG exporter

LNG carrier fleet operators

Carrier-tech/royalty plays paid on new vessel orders globally

Midstream operators feeding Gulf Coast terminals

NGL/LPG exporters adjacent to the same infrastructure

A U.S. integrated major with flagship LNG operations

A global LNG trader

All are positioned to capture margin as Europe bids aggressively for U.S. volumes.

Cross-checked public data confirms the momentum (as of Q1 2026 earnings and May export updates):

Cheniere Energy (NYSE: LNG) — the largest U.S. LNG exporter — reported record Q1 2026 results: 187 cargoes exported (up 11% YoY) and 688 TBtu loaded (up 13%). The company raised full-year 2026 guidance: Consolidated Adjusted EBITDA to $7.25–7.75 billion (from $6.75–7.25B) and Distributable Cash Flow to $4.75–5.25 billion. Corpus Christi Stage 3 is ramping, with Trains 5-7 progressing toward substantial completion. Europe remains Cheniere’s largest destination market.

U.S. LNG feed gas has averaged ~18.9 Bcf/d YTD 2026, briefly hitting 20+ Bcf/d in April. EIA forecasts full-year 2026 LNG exports at ~17 Bcf/d, with further growth into 2027 as new capacity (Golden Pass, Port Arthur, Rio Grande, etc.) comes online.

Shipping and midstream plays (e.g., fleet operators like Golar LNG and midstream giants like Enterprise Products Partners (EPD) and Kinder Morgan (KMI)) have seen strong utilization and volume tailwinds from Gulf Coast LNG demand. Carrier-tech royalty companies (such as GTT) benefit from surging newbuild orders and high-margin (~60%+ EBITDA) licensing.

Venture Global (NYSE: VG) and other pure-play exporters have also posted volume acceleration and stock gains amid the global tightness.

What Investors Should Look For in Companies, Earnings, and Potential Volumes

The repricing isn’t one-off—it’s structural. Here’s the investor checklist for the next 60 days (Q2 earnings season and early refill data):Export Volumes & Utilization — Watch monthly EIA LNG export reports and company cargo counts/TBtu loaded. Cheniere and peers running at 95%+ utilization signal sustained demand. New trains ramping (e.g., Cheniere Corpus Christi Stage 3) add ~0.6 Bcf/d+ in 2026.

Earnings Metrics — Focus on Adjusted EBITDA, Distributable Cash Flow, and realized margins (especially spot/optimization exposure). Non-cash derivative noise (common in IPM agreements) can distort GAAP but ignore it—cash generation is the story. Raised guidance, as Cheniere delivered in Q1, is a strong bullish signal.

Contract Portfolio & Europe Exposure — Companies with destination-flexible or spot-linked cargoes capture the TTF-Henry Hub spread. Long-term contracts provide floor; spot provides upside.

EU Storage Fill Rate & TTF Curve — Track Gas Infrastructure Europe (GIE) data weekly. Need ~145 bcm injected by November for comfort. Backwardation or sharp TTF spikes confirm urgency. Current fill ~30-36% is a deficit vs. norms.

Geopolitical & Supply Catalysts — Hormuz transit updates, Qatar/UAE repair timelines (3-5 years cited for full restoration), and any U.S. policy support for exports. New capacity milestones (FID, first LNG dates) for 2027+ growth.

Risk Datapoints to Monitor — Faster-than-expected Hormuz reopening, demand destruction in Europe/Asia, or a 2027+ global LNG supply wave could pressure margins.

Bottom line: The Merchant’s News thesis aligns tightly with real-time fundamentals. U.S. LNG is no longer a “nice-to-have” for Europe—it’s the primary lifeline. Companies across the value chain with Gulf Coast exposure, strong balance sheets, and volume growth are seeing their earnings power repriced higher.

Energy investors: this chokepoint isn’t going away in the next 12-24 months. Position accordingly, but size for volatility—geopolitics moves fast.

This article is for informational purposes only and is not investment advice. Always conduct your own due diligence.

Appendix: All Sources

- The Merchant’s News Substack: “Europe’s Gas Crisis Just Repriced 8 Of My 12 Positions” by Giacomo Prandelli (May 27, 2026) – https://themerchantsnews.substack.com/p/europes-gas-crisis-just-repriced

- EIA Short-Term Energy Outlook & Natural Gas Monthly (various April-May 2026 releases)

- Reuters, S&P Global, Kpler, GIE/AGSI+ data on EU storage and TTF prices (May 2026)

- Cheniere Energy Q1 2026 Earnings Release & Conference Call Presentation (May 7, 2026)

- Additional reporting from Reuters, Yahoo Finance, Investing.com, and Columbia SIPA Center on Global Energy Policy (March-May 2026 coverage of Hormuz/LNG disruptions)

Stay tuned to Energy News Beat for ongoing LNG market updates, earnings recaps, and volume trackers. What are your thoughts on the U.S. LNG opportunity?

The post Europe’s Gas Crisis Just Repriced 8 Of My 12 Positions – The Merchant’s News appeared first on Energy News Beat.