German owner Elbdeich Reederei has firmed up orders for two more containerships at Huangpu Wenchong in China.

Brokers report the Drochtersen-based company has lifted options for a pair of 1,900 teu newbuilds it held at the CSSC-affiliated yard, following a deal for two firm units earlier this year.

The ships cost about $32.3m each with deliveries scheduled throughout 2027.

Elbdeich counts more than 30 ships in its fleet. The company also has 1.300 teu methanol dual-fuel newbuilds booked at Wenchong for delivery in 2026. The order is backed by DP World-controlled feeder operator Unifeeder.

Prices for vintage capesize bulkers are rising again, as spot rates are up around 300% in a month driven in part by an armada of ships waiting to load bauxite at West African ports.

Lila Global is widely reported to have sold a pair of 2006-built capes, the 172,000 dwt Maran Sailor and Maran Odyssey, for $19m each. In comparison, Nasdaq-listed Greek owner OceanPal sold a one-year older sister ship in January for $16.2m to China’s Rongchang Shipping.

Meanwhile, Korea Line is reportedly selling the 15-year-old Daewoo-built bulker Rosemary. Initially, bids were seen at mid-$24m levels. Still, by Friday, it was reported sold for $25m.

One of many owners who has decided to cash in is Eastern Pacific Shipping. Brokers note that this owner is letting go of two Koyo Dock bulkers, selling two 15-year-old 180,00 dwt units, Mount Song and Mount Austin, for about $27m each.

The International Chamber of Shipping (ICS) and the Comité Maritime International (CMI), a body responsible for drafting many maritime law conventions, have launched an updated campaign to get governments to ratify urgent maritime treaties.

“For a global industry, comprehensively regulated by the International Maritime Organization (IMO) and other United Nations bodies, it is critical that the Conventions are widely ratified in order to ensure that the same regulations apply to all ships in international trade during all parts of their voyage,” the two organisations said today in a release.

The renewed campaign comes at a time when the US under Donald Trump is increasingly being seen as tearing up the old international rulebook.

The international maritime conventions strongly encouraged to be ratified by governments by ICS and CMI as an urgent priority are the IMO Nairobi Convention on the Removal of Wrecks (Nairobi WRC), 2007, IMO 2010 Protocol to the International Convention on Liability and Compensation for Damage in Connection with the Carriage of Hazardous and Noxious Substances by Sea (HNS), 1996, the IMO Convention for the Safe and Environmentally Sound Recycling of Ships (Hong Kong), 2009, and the United Nations Convention on the International Effects of Judicial Sales of Ships, 2023, also known as the Beijing Convention.

A global industry needs global regulations

The purpose of the campaign is for ICS and CMI members, which represent national shipowner associations and national maritime law associations respectively, to engage with their governments to urge them to ratify these conventions where they are not currently in force.

“Our industry is dependent on a global regulatory system to operate efficiently and safely. Global standards must be uniformly applied and enforced worldwide to prevent significant challenges arising, including a patchwork of unilateral regulations and inferior levels of safety and environmental protection. It is fundamental that the same regulations are equally applied to all ships engaged in international trade, and that the same rules apply during the entire voyage. A global industry needs global regulations,” commented Kiran Khosla, principal director covering legal at the ICS.

Ann Fenech, president of the CMI, added: “Today’s challenging international scene and geopolitical developments in which shipowners, charterers, cargo owners, financiers, flag administrations, and maritime players generally are navigating, make it all the more important, now more than ever before, that the maritime law and regulations in different jurisdictions provide legal certainty and uniformity.”

Liner shipping profits are forecast to slide by more than 80% this year.

Analysts at Sea-Intelligence have calculated that the container shipping industry made a combined EBIT last year of $60bn, the third highest figure recorded in the history of the business, and the highest outside the covid era.

One leading container markets analyst, John McCown, who runs New York-based Blue Alpha Capital, is expecting the liner sector to remain in the black this year, albeit with profits sliding to below $10bn.

“With the downward trend seen in pricing that has continued this quarter, 1Q25 results will certainly be below 4Q24,” McCown wrote in his latest markets update, conceding that the tariff situation unleashed by the new Donald Trump administration in the US has “injected more uncertainty than usual”.

The Bank of International Settlements has warned that the uncertainty generated by Trump’s promises to impose tariffs and embark on a massive job cull threatens the world economy’s soft landing after years of high inflation and elevated interest rates. It stated that “policy uncertainty on tariffs, US fiscal policy, immigration, and regulation … work like a negative demand shock. They would have negative effects on spending, investment and we see some signs of that. If tariffs are implemented – and some have been – then the negative demand shocks can become supply shocks and give rise to inflationary pressure.”

Container spot rates have been on a constant slide in 2025. The overall Shanghai Containerized Freight Index is now down 47% since the start of the year.

Prices on Asia to North Europe, Asia to the Mediterranean, and on the transpacific to the US west and east coasts are now all lower than at any point in time in 2024, according to data from Drewry.

However, comparing spot rates now to the level seen in mid-December 2023 just before the Red Sea shipping crisis, Asia to North Europe remains up 74%, Asia to the Mediterranean remains up 96%, while voyages across the Pacific to both the west and east coasts are still up by more than 40% compared to the lows experienced towards the end of 2023.

“Continued softening in the spot market comes against a backdrop of weaker than usual volumes post-Lunar New Year, increased competition between liner companies amid alliance restructuring, and widespread uncertainty brought about by an ongoing series of tariff announcements from the US and its trading partners,” commented Clarksons Research in a weekly report.

As neatly surmised by Maersk in its annual report published in February, liner profits in 2025 are on a knife edge, largely out of the carriers’ control – what happens in the Middle East ought to dictate the difference between red and black ink.

Maersk reported its third-best financial year ever in February with an EBIT for 2024 of $6.5bn. The Danish carrier forecasted global container volume growth in 2025 will be around 4%. However, the very big dividing line between profit and loss this year, according to Maersk, will centre around the Red Sea.

The Houthis of Yemen have put their campaign against merchant shipping on hold, with no attacks reported in 2025 so far, as Israel and Hamas take steps toward peace. The situation remains tense however with very few liners returning to take the Suez route between Asia and Europe.

Maersk’s EBIT forecast for 2025 ranges from zero to $3bn, depending on whether the Red Sea opens in the middle of the year or the end of the year.

Norwegian offshore vessel owner DOF has won a contract for an FPSO installation project from an undisclosed client in the Atlantic region.

According to an Oslo Bors filing, DOF shall deliver project management, engineering, logistical services, and offshore execution.

DOF will use two anchor-handling tug supply vessels to perform the installation duties. The project is scheduled for execution in the second quarter of 2025 in Africa.

Precise financial details were not provided, however, the company revealed that the contract was significant placing the deal in the $15m to $25m range.

New York-listed suezmax specialist Nordic American Tankers (NAT) has confirmed the addition of another 2016 South Korean-built vessel.

The Herbjorn Hansson-led owner and operator has picked up the unnamed tanker in a deal struck in the mid-to-high $60m range, shortly after agreeing to buy a sister vessel from the same owner.

Both ships were built at Sungdong and will be financed through leasebacks with Ocean Yield. The vessels will be delivered into an eight-year bareboat charter to NAT in the second quarter, with a purchase obligation at the end.

S&P sources suggest the deals at $68m each involve Eastern Pacific Shipping’s scrubber-fitted duo Diamondway and Goldway.

Following the latest confirmed transaction, NAT’s fleet on a fully-delivered basis will stand at 21 ships.

Having attended over 200 shipping events since 2009, Gennadiy Ivanov found last year’s inaugural Geneva Dry gathering to be one of the most “efficient, proactive and practical” conferences he’s ever attended.

“As proof of its value, we registered for the second Geneva Dry the very next day after the first one concluded,” Ivanov, a director at BPG Shipping, tells Splash.

Founded in 2017 in Dubai, BPG Shipping is one of the many ship operators due to attend the world’s premier commodities shipping conference when Geneva Dry reconvenes at the end of April. BPG specialises in dry bulk, handling both major and minor bulks in the handysize, supramax, and panamax segments.

Come the end of April, when Ivanov picks up his delegate pack in the foyer of the Hotel President Wilson on the shore of Lake Geneva, he’s expecting dry bulk prospects to be more healthy, in no small part down to the far higher than average number of dry bulk carriers bound for drydockings in 2025.

He does concede that tariff uncertainties and a possible slowdown in the global economy cloud any projections this year, topics that will be discussed during the summit’s opening Commodities Shipping Outlook, a high-level scene-setter designed to give attendees an indication of what to expect in the coming 24 months. From geopolitics to demand forecasts, new regulations, fuels and new technology this session features the heads of INTERCARGO and BIMCO, Trafigura’s chief economist as well as the president of marine and offshore for Bureau Veritas.

Geneva Dry brings together all elements of the commodities shipping sector to host the ultimate dry bulk shipping event.

Split into sectors, panels will bring together analysts, financiers, miners, traders and shipowners to discuss where the markets are headed. Sessions include:

Minor Bulks

Agri-commodities

Coal

Iron Ore

The full Geneva Dry agenda can be accessed here. Geneva Dry registration, at just $780, can be accessed here. Special Geneva Dry hotel room rates can be found here.

The over 230 companies attending Geneva Dry 2025 include: 2020 Bulkers, ABS, Aderco, Admaren, Aferrari Maritime Advisory, Affinity, Alberta Shipmanagement, Alcos Transport, Amart Shipping, Ambica Logistics, AmSpec, Anglo American, A.O. Schifffahrt, Ariston Navigation, AR Savage & Son, Arrow, Asia Shipping Media, Asiatic Lloyd Maritime, Asyad Shipping Company, AXSMarine, Bahri Dry Bulk, Balena Projects, Baltic Exchange, Banchero Costa, Beaufort Shipping, Berenberg Bank, Bery Maritime Inc., BIMCO, BIS Services, Blue Astra Maritime, Blue Visby Services, BPG Shipping Company, Braemar, BroadPeak Partners, BUDD Group, Bulk Commodity Trade, Bulk Egypt, Bureau Veritas, Burmester and Vogel, CALLS Shipping, Cambiaso Risso, Cargill, Castlewood Capital Partners, Cetus Maritime, Charterers P&I Club, Chesva Enterprises, Chinaland Shipping, Clarksons Port Services, CMA CGM, Coach Solutions, Cobelfret, COFCO International, Colfletar, Consortium Maritime Trading, Copenhagen Commercial Platform, Cross Office, CR International, CSBL, CSN Mining International, CTM, d’Amico Dry, Dataloy, DennisMathiew, Devbulk, DNV, Drydel Shipping, DryLog, Dualog, Earth X Space, Eastern Mediterranean Maritime, Eastmen Shipping Co., EBE, Eksen Chartering, Eltronic FuelTech, EMSS DMCC, Enesel, Eramet, Erhardt Logistics, European Energy Exchange, Exen Global, Fednav, F.G.M. Chartering, Fleet Cleaner, G2 Ocean, GAC, GAC Services, Genoa Sea Brokers, GeoServe, Goulandris Brothers, GP Shipping, Grain Compass Shipping, Granos Oros, Great Eastern Shipping Company, Greenheart Management, Grieg Shipbrokers, Hadley Shipping Group, Harbor Lab, Harren Group, Hartree Partners, Heidelberg Materials Trading, Hempel, HFW, Himalaya Shipping, HR Maritime, H. Vogemann, IFCHOR GALBRAITHS, IHB Shipping, Inchcape Shipping Services, INCOFE, Independent Ship Agents, Infospectrum, Inmarsat, INTERCARGO, InvestHK, Iskele Shipping, Isle of Man Ship Registry, JBG Shipping Agency, JJ Ugland, Kaizen Ship Management, KC Maritime, KGJS/BTG, Klaveness, Kpler, LA Marine, Latitude Brokers, LAM Lyonel A. Makzume Shipping Agency, Leeway Brokers, LETH Agencies, Liengaard & Roschmann, Lloyd’s List Intelligence, Lloyd’s Register, London Stock Exchange Group, Lykiardopulo & Co, Mandarin Shipping, Manta Marine Technologies, Marcura, Marex, Marfin Management, Mariner Communications, Maritime Optima, Marshall Islands Registry, MasOceans, Med Shipping Agency, Metbulk Shipbrokers, Metbulk Shipping, Mid-Ship Group, Montfort Trading, Mulberry Shipping and Consulting, NAPA, Navis, Neptune Maritime Leasing, Nextvoyage, Norbulk Shipping, Norden, NorthStandard, Nova Marine Carriers, Novamaxis, OBT Shipping Group, Oceanbulk Maritime, Ocean Recap, OceanWings, Orion Reederei, Overhorn Swiss, Pan Marine Group, Paralos Asset Management, Paralos Shipping, Paratus, Petro Inspect, Plutofylax Shipping Corporation, P&O Maritime Ukraine, Port Scope, Precious Shipping, Pyxis Logistics, Quest Group, Range Shipping, RightShip, Rustibus, RZHA, S5 Agency World, Safe Bulkers, S-Bulkers, SEA, Seaber, Seanergy Maritime Holdings, SEDNA, Seven Oceans, Seven Seas Marine Management, SGM Shipping Services, SGX Group, Siddhartha Logistics, Signal, SMB Law, Soki Kisen, South32, Southport Agencies, Spinergie, SS Rice News, SSY, Star Bulk, Steamship Mutual, StoneX, SUISSENÉGOCE, SwissMarine, Taylor Maritime Investments, TCC Group, Team Fuel Corp, TheOceann.ai, Thurlestone Shipping, TMA Bulk, Tradeviews, TradeWinds, Trafigura, Triton Bulk, Tsakos Shipping, Two Oceans, United Maritime Corporation, Universal Shipping, Vale, Vale Base Metals, Valiant Shipping, Veson Nautical, V.Group, VPS, Wah Kwong Maritime Transport Holdings, Wallem Group, Walter Cuminns Group, Waypoint Commodities, WBL Shipping Agency, Weathernews, Western Bulk, Wilson Sons, Windward Shipping and ZeroNorth.

Below 2022 highs: Austin, San Francisco, Phoenix, San Antonio, Denver, Sacramento, Dallas-Ft. Worth, Portland, Salt Lake, Seattle, Tampa, Raleigh, Houston, Atlanta, Charlotte, Nashville, Las Vegas, Minneapolis, Orlando…

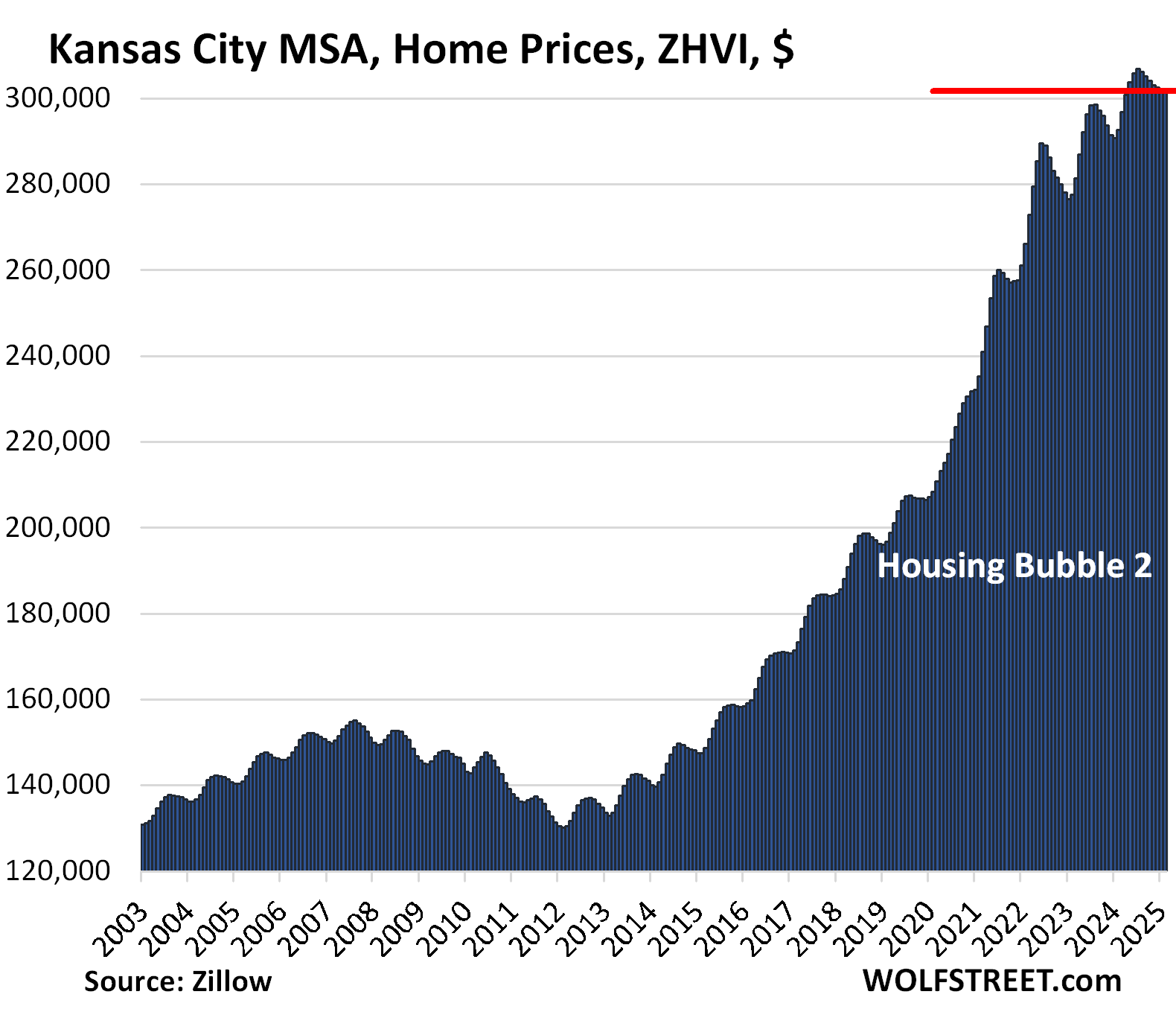

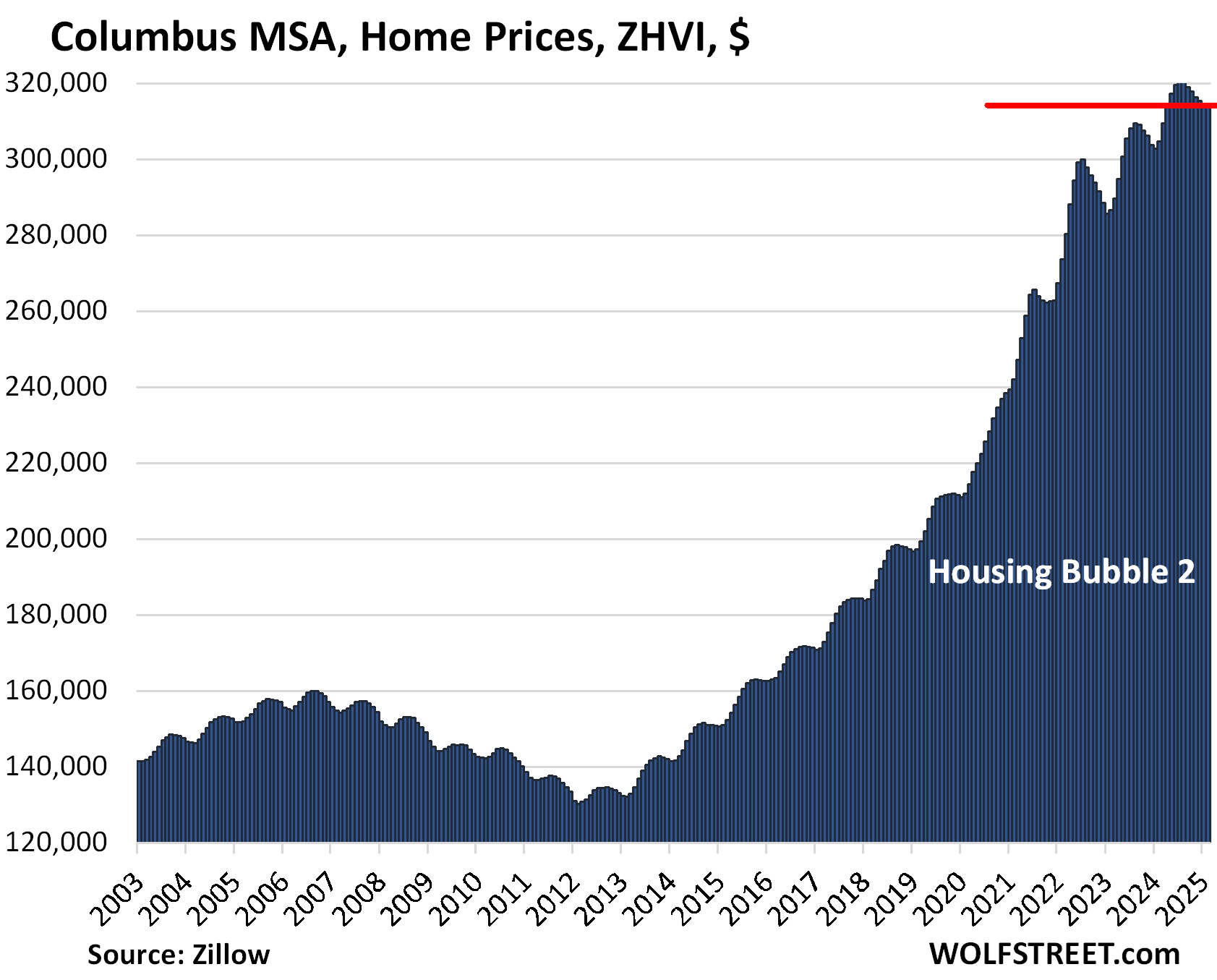

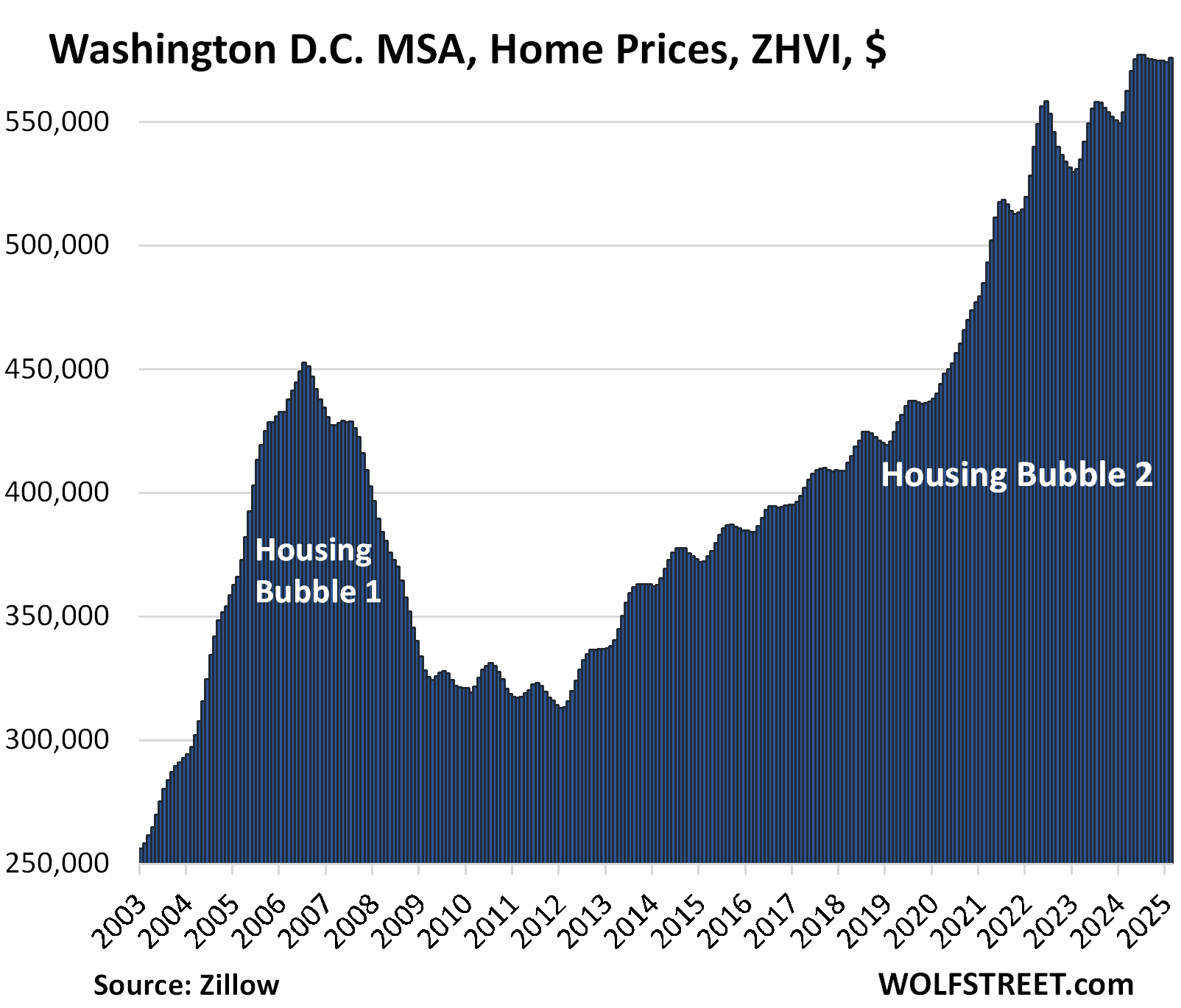

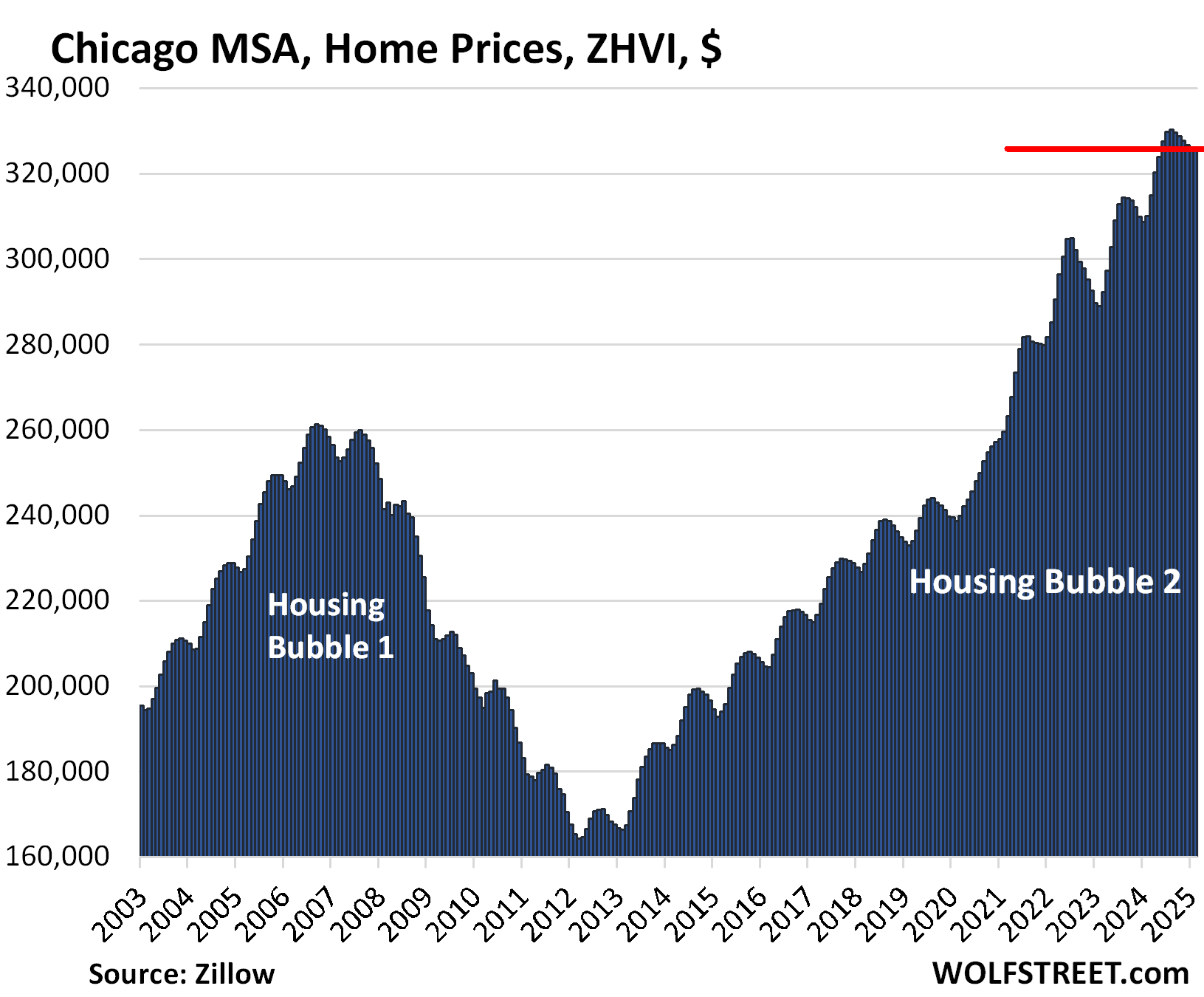

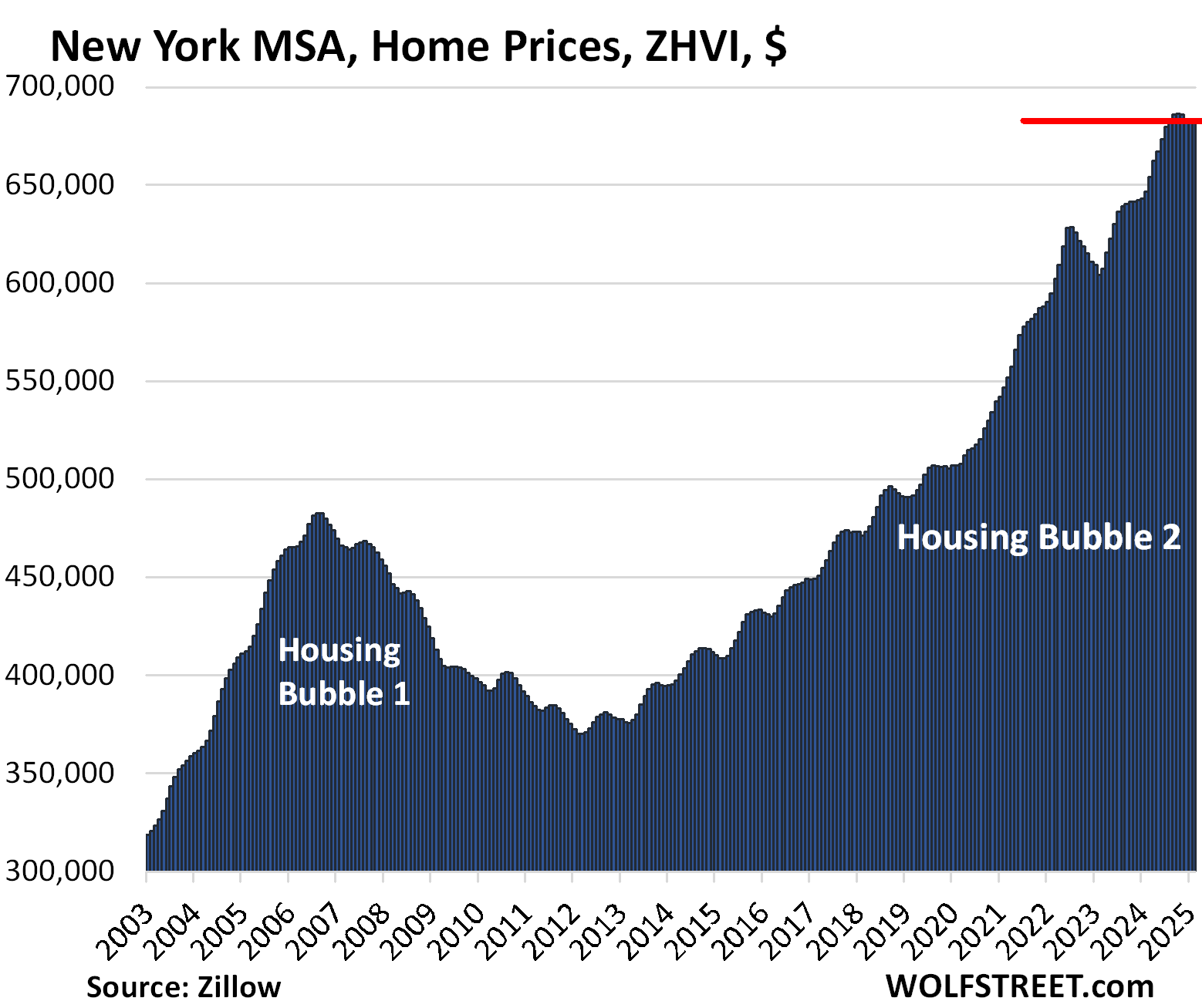

Rose past their 2022 highs (but some are now sagging): Miami, San Diego, Los Angeles, Baltimore, Kansas City, Columbus, Washington D.C., Philadelphia, Boston, Chicago, New York…

Prices of single-family houses, condos, and co-ops in February fell in some of the 33 large Metropolitan Statistical Areas (MSAs) on our list here. And in 21 of these metros, prices are down from the 2022 peaks. In other metros, prices rose. None made new highs in February.

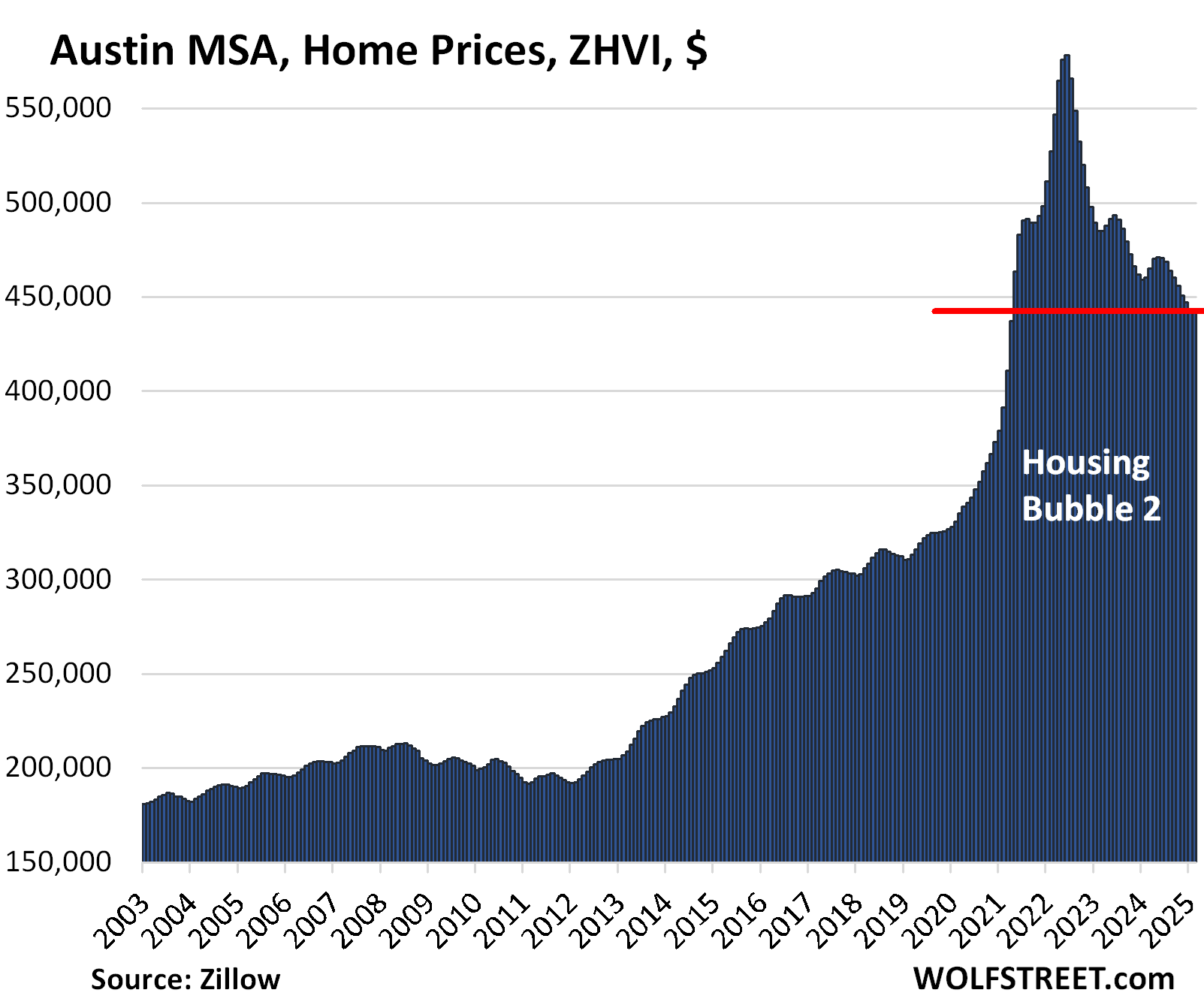

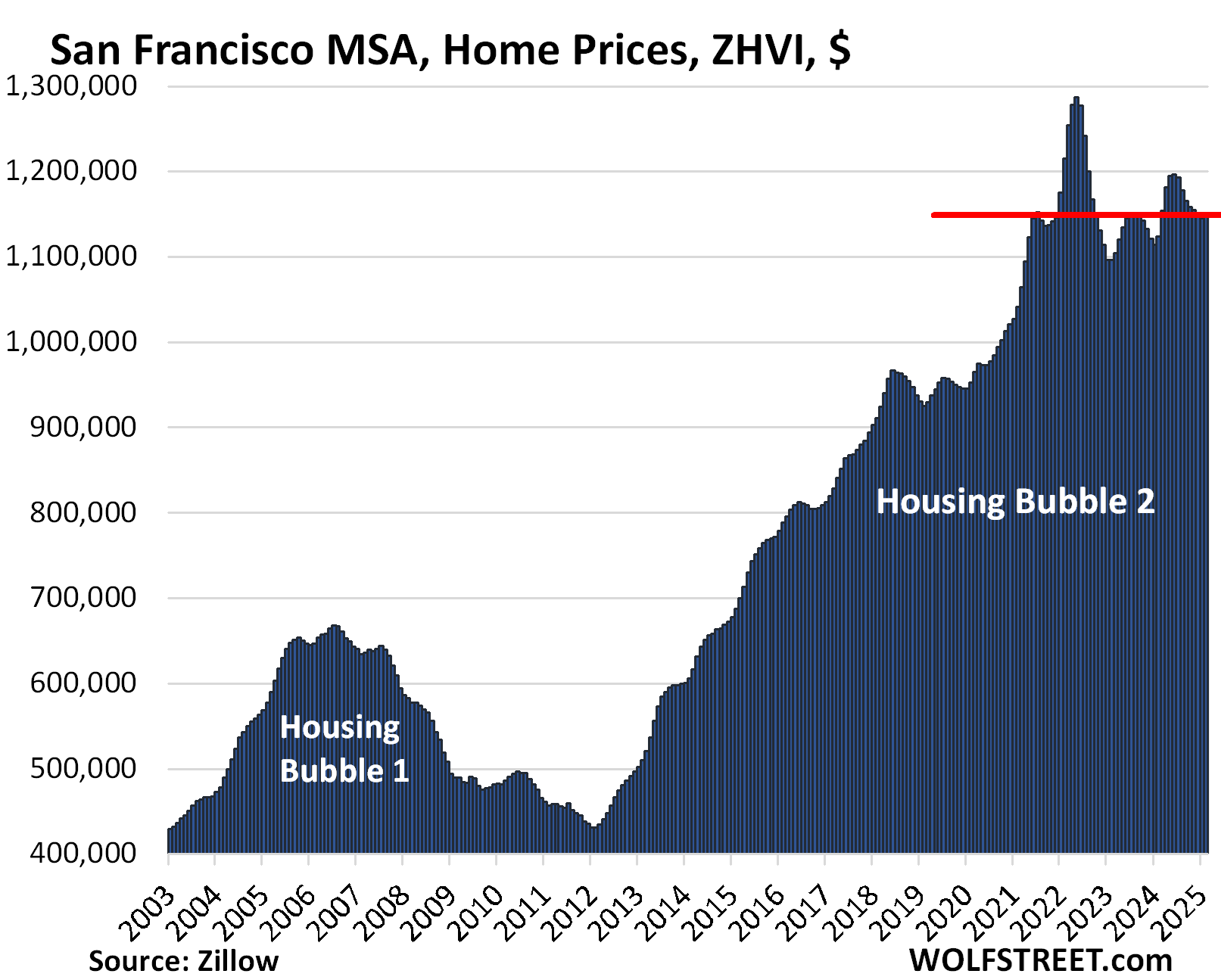

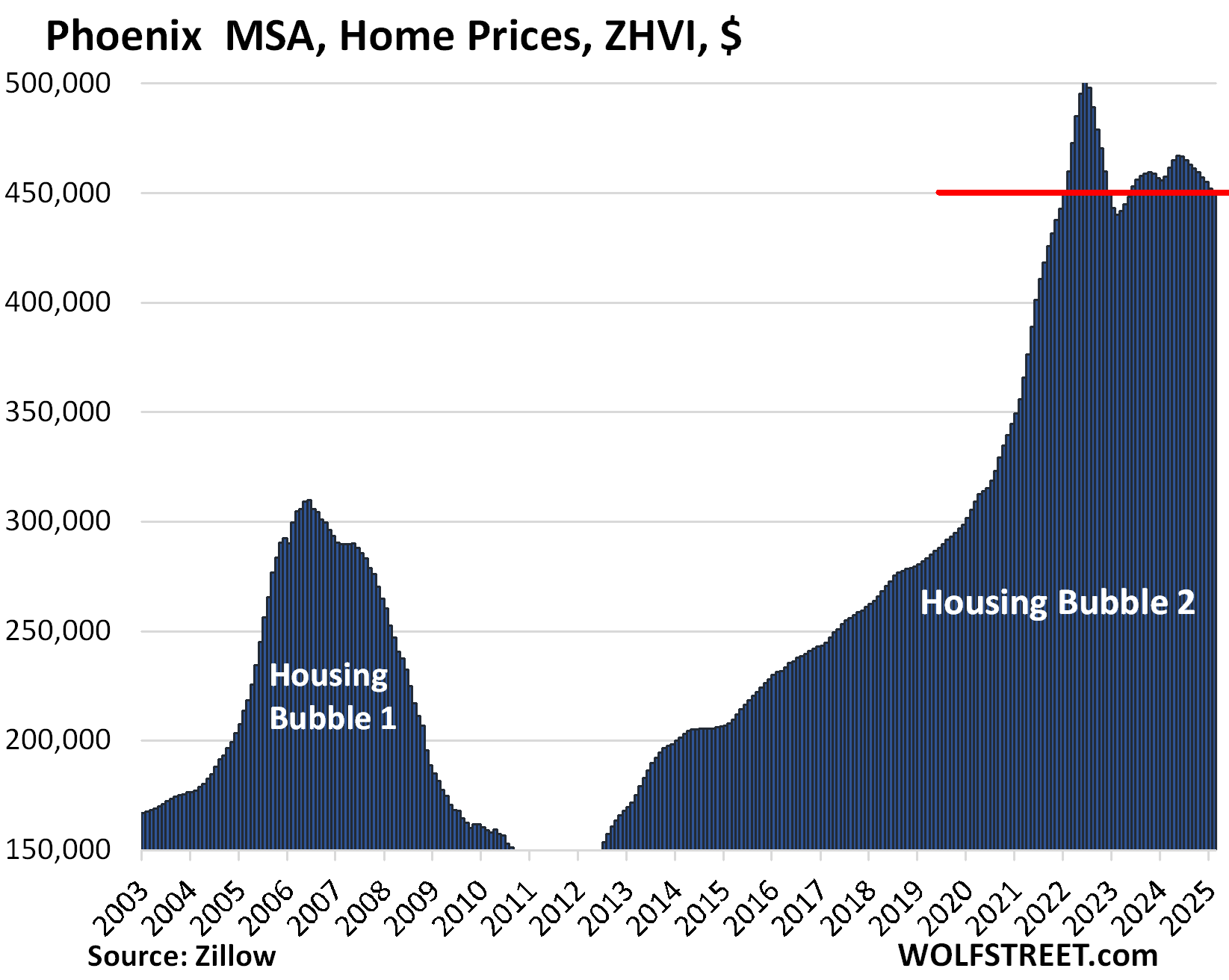

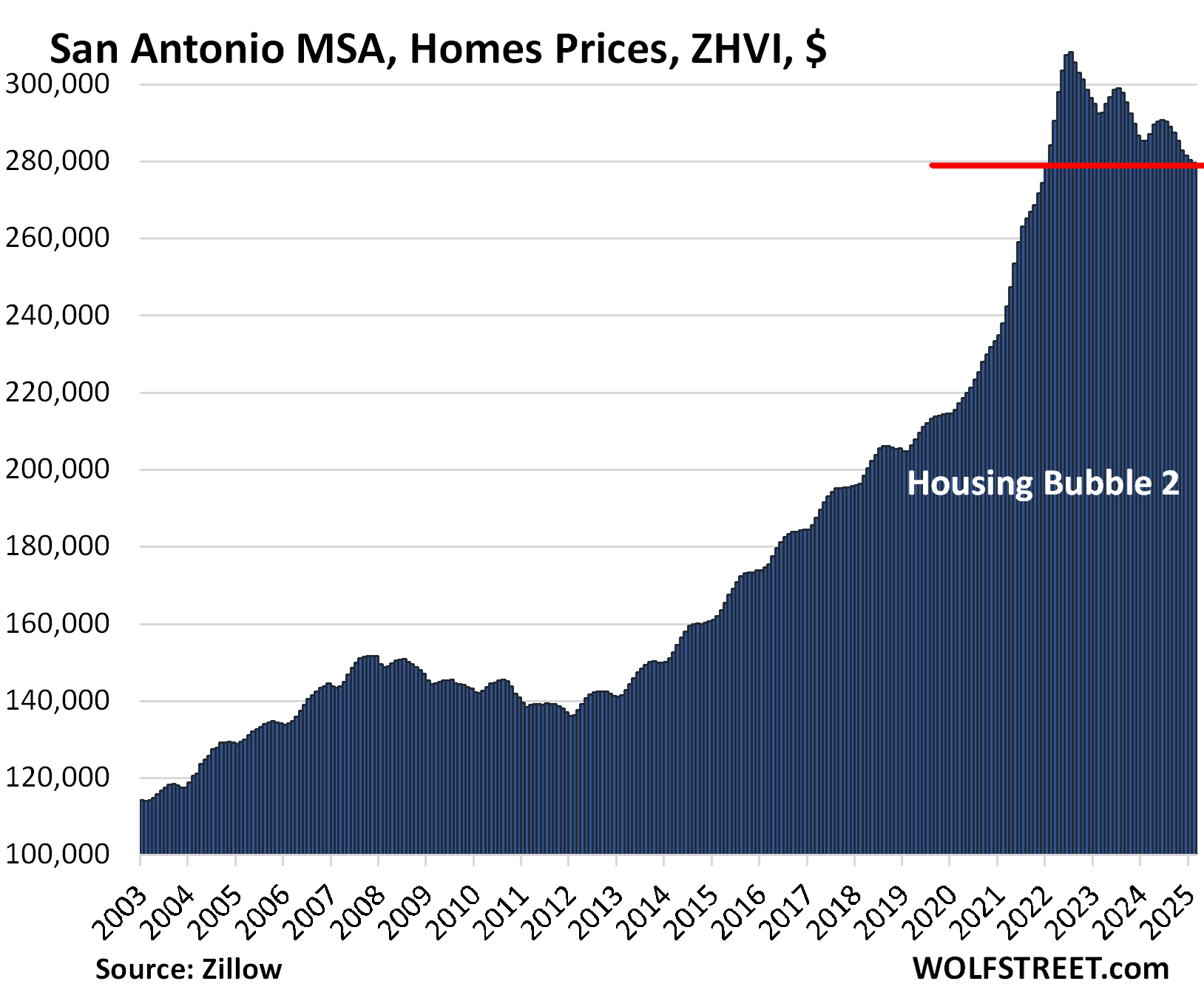

Down from the 2022 peaks: Prices in 21 metros of our 33 metros are down from their 2022 peaks, led by the metros of Austin (-23.4%), San Francisco (-10.6%), Phoenix (-10.1%), San Antonio (-9.4%), and Denver (-8.2%).

Down year-over-year: Prices in 7 metros were down year-over-year, led by Austin (-3.8%), Tampa (-3.6%), San Antonio (-2.0%), Phoenix (-1.6%) … including now Miami (-0.2%). Denver was down just a hair (-0.02%), so essentially unchanged.

No New highs in February 2025: No metro of the 33 metros here made a new highs.

Some technical points. All data is from the “raw” mid-tier Zillow Home Value Index (ZHVI), released Sunday. The ZHVI is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. Zillow’s Database of All Homes also has sales-pairs data.

In some markets, there is no seasonality to home prices, as you can see in the charts below, which are not-seasonally-adjusted. In other markets, there is distinct seasonality, with annual price peaks occurring at roughly the same month of the year.

To qualify for this list, the MSA must be one of the largest by population, and must have had a ZHVI of at least $300,000 at the peak. The metros of New Orleans, Oklahoma City, Tulsa, Cincinnati, Pittsburgh, etc. don’t qualify for this list because their ZHVI has never reached $300,000, despite the surge of home prices in recent years, but from low levels.

The 21 metros below their highs of mid-2022.

Home prices exploded during the pandemic and through mid-2022 in these markets, driven by the Fed’s interest rate repression, including trillions of dollars of QE at the time, resulting in below-3% mortgages.

But the Fed gradually backed away from interest-rate repression starting in 2022, hiked rates, and has shed $2.2 trillion in assets from its balance sheet. Since September 2022, mortgage rates have been around 7%, give or take some – they’re currently at 6.65%, according to the Mortgage Bankers Association – and these rates were normal before QE started in 2008.

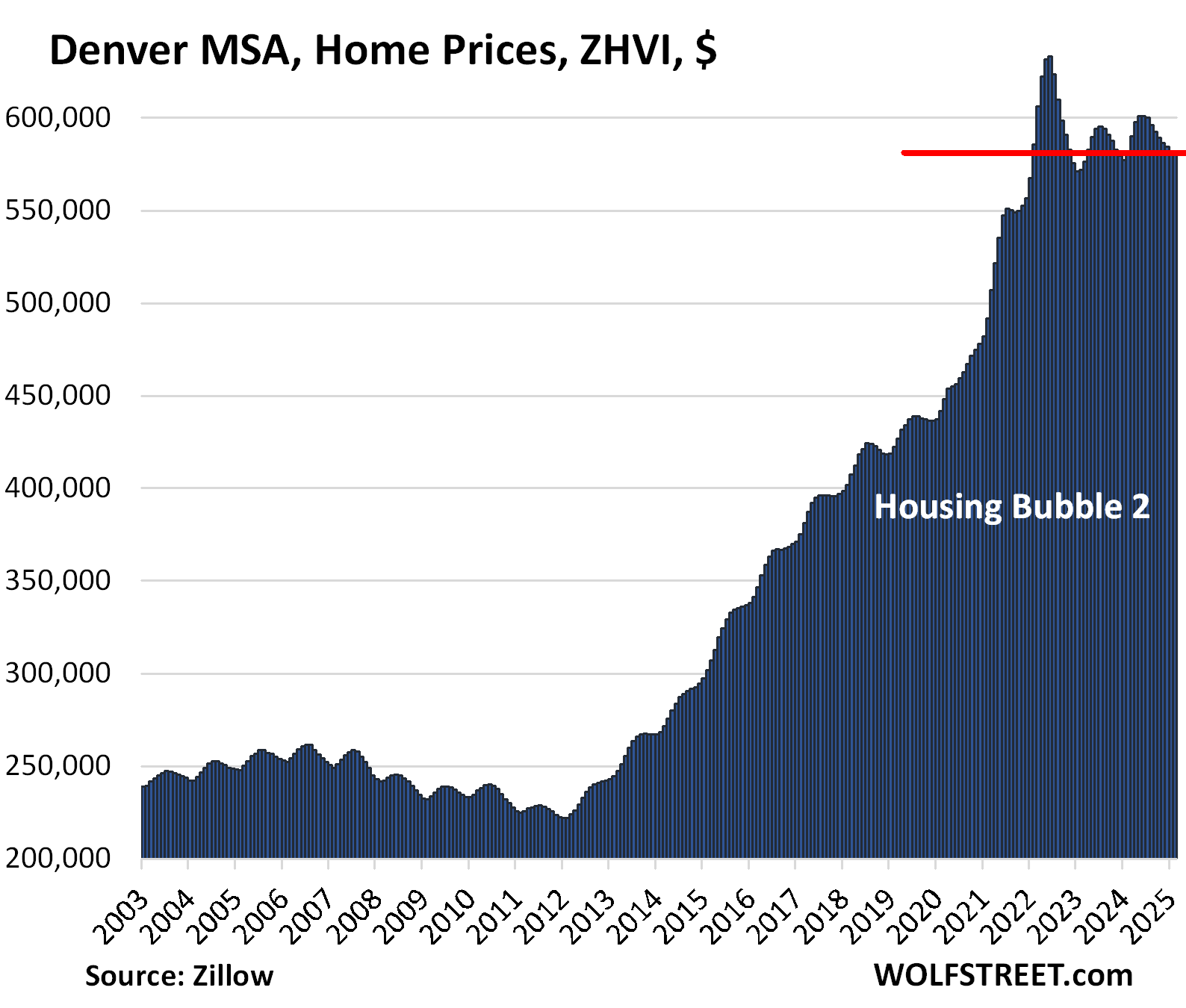

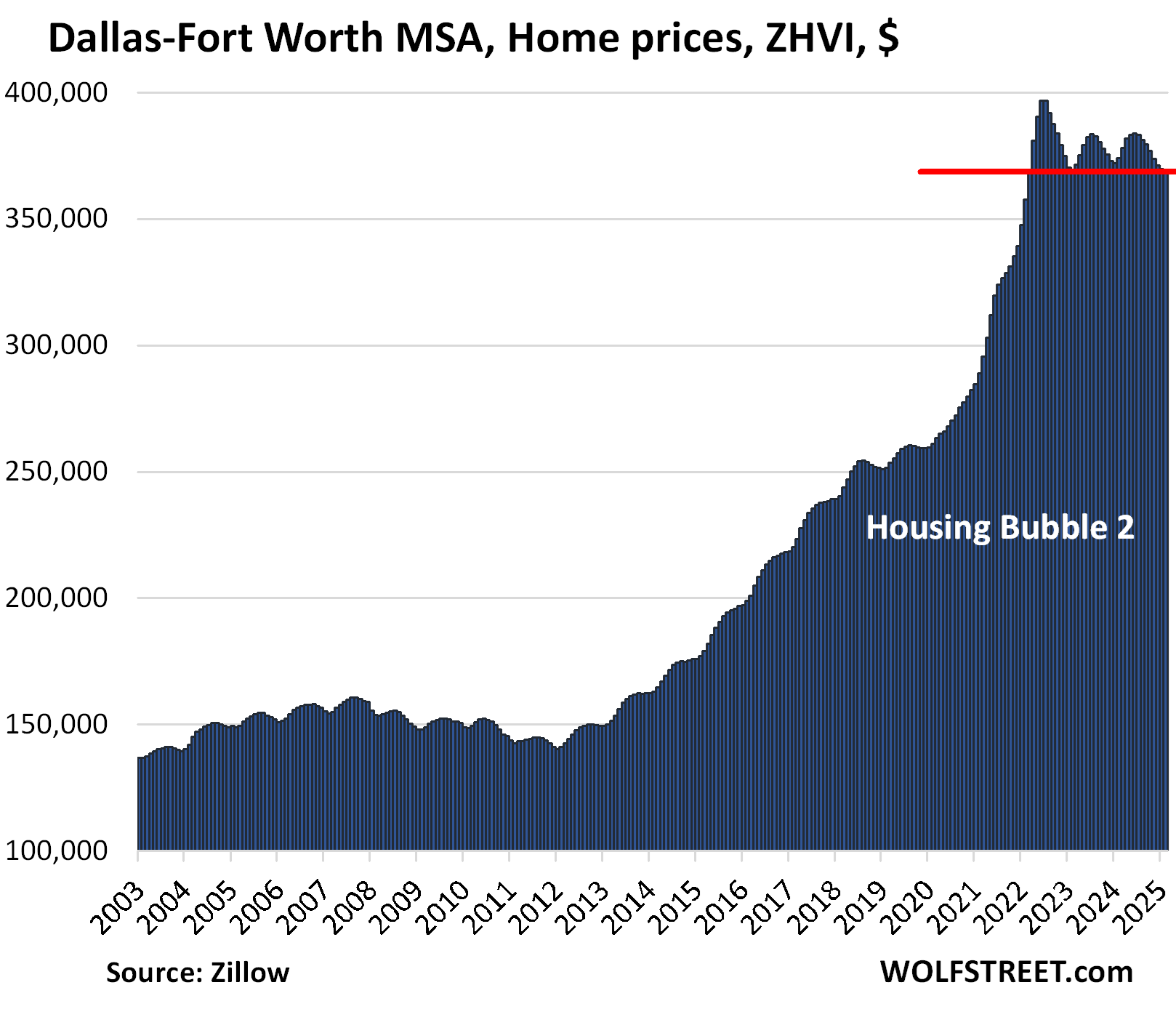

One curious thing visible in the charts – on top of their inherent absurdity – is that the metros in Texas, the Denver metro, and a few other metros didn’t experience Housing Bubble 1 which began to implode in 2006. Texas had finally gotten through with a huge housing bust some years earlier, and it therefore didn’t experience the big price drops in 2006 to 2012, just moderate declines. But its Housing Bubble 2 was a doozie.

Austin MSA, Home Prices

From Jun 2022 peak

MoM

YoY

Since 2000

-23.4%

-0.1%

-3.8%

153%

The Austin MSA includes the counties of Travis (Austin-Round Rock), Williamson, Hays, Caldwell, and Bastrop.

Prices are back where they’d been in April 2021. No real estate chart should ever look like this absurdity.

San Francisco MSA, Home Prices

From May 2022 peak

MoM

YoY

Since 2000

-10.6%

0.5%

2.4%

290%

The MSA includes San Francisco, Oakland, much of the East Bay, much of the North Bay, and goes south on the Peninsula into Silicon Valley through San Mateo County.

Prices are back where they’d first been in June 2021.

Phoenix MSA, Home Prices

From Jun 2022 peak

MoM

YoY

Since 2000

-10.1%

-0.4%

-1.6%

216%

Prices are back where they’d first been in January 2022:

San Antonio MSA, Home Prices

From Jul 2022 peak

MoM

YoY

Since 2000

-9.4%

-0.3%

-2.0%

145.6%

Prices have dropped to the lowest level since January 2022.

Denver MSA, Home Prices

From Jun 2022 peak

MoM

YoY

Since 2000

-8.2%

0.0%

0.0%

209%

Prices are back where they’d first been in February 2022.

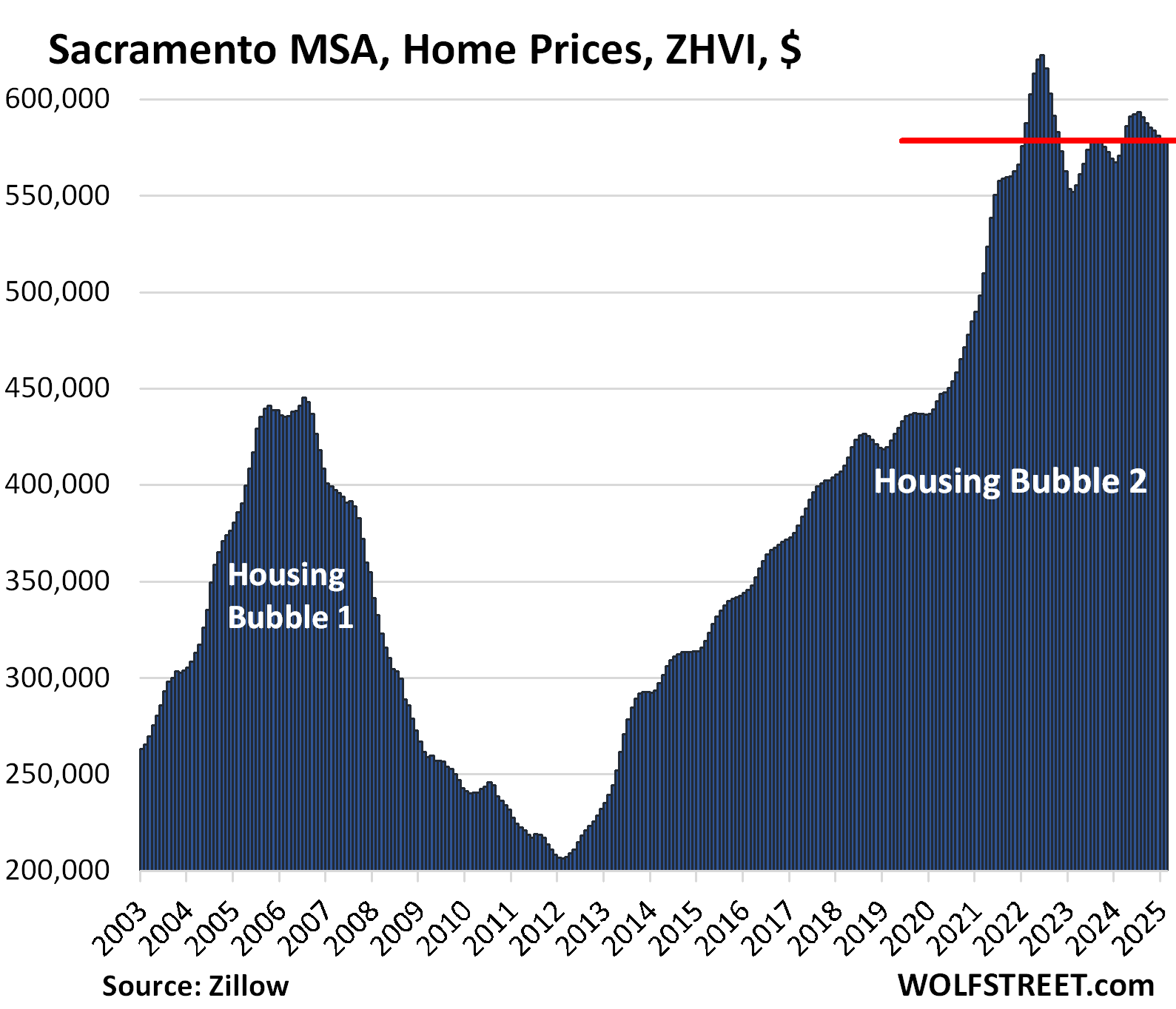

Sacramento MSA, Home Prices

From July 2022 peak

MoM

YoY

Since 2000

-7.2%

0.0%

1.3%

243.1%

Dallas-Fort Worth MSA, Home Prices

From Jun 2022 peak

MoM

YoY

Since 2000

-7.1%

-0.2%

-1.4%

190%

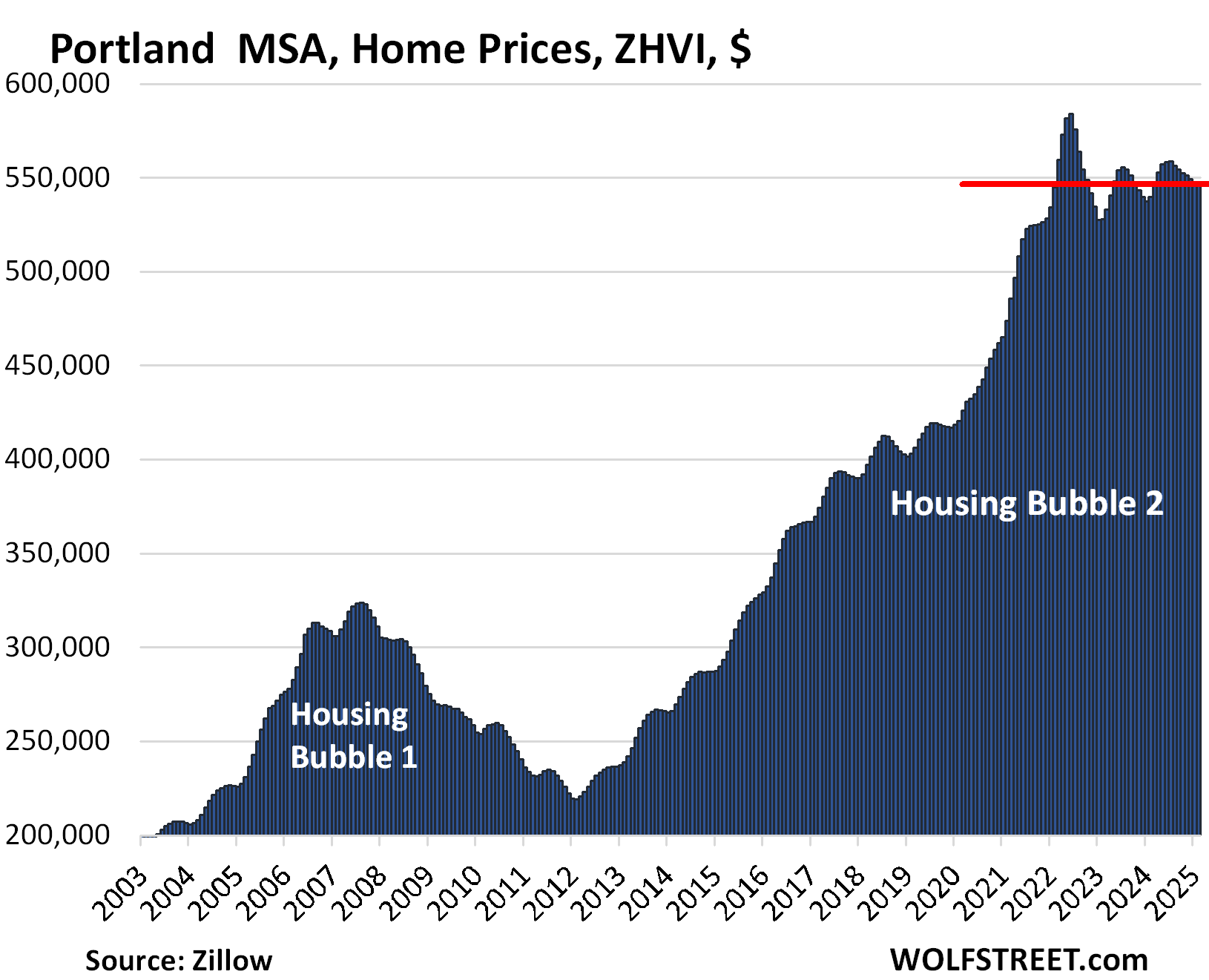

Portland MSA, Home Prices

From May 2022 peak

MoM

YoY

Since 2000

-6.3%

0.1%

1.3%

216%

Prices are back where they’d first been in January 2022.

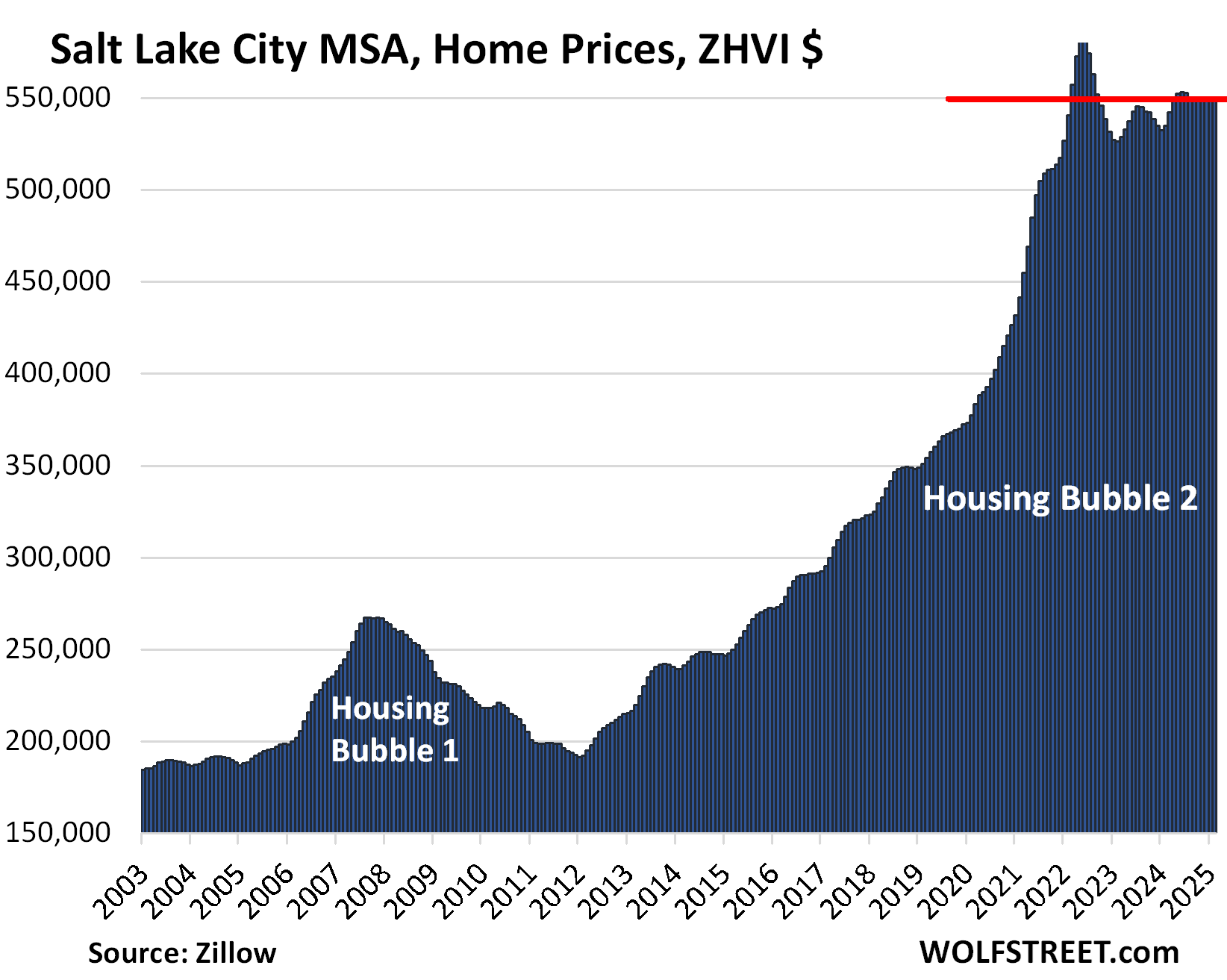

Salt Lake City MSA, Home Prices

From July 2022 peak

MoM

YoY

Since 2000

-5.8%

0.2%

2.7%

214%

First seen in March 2022:

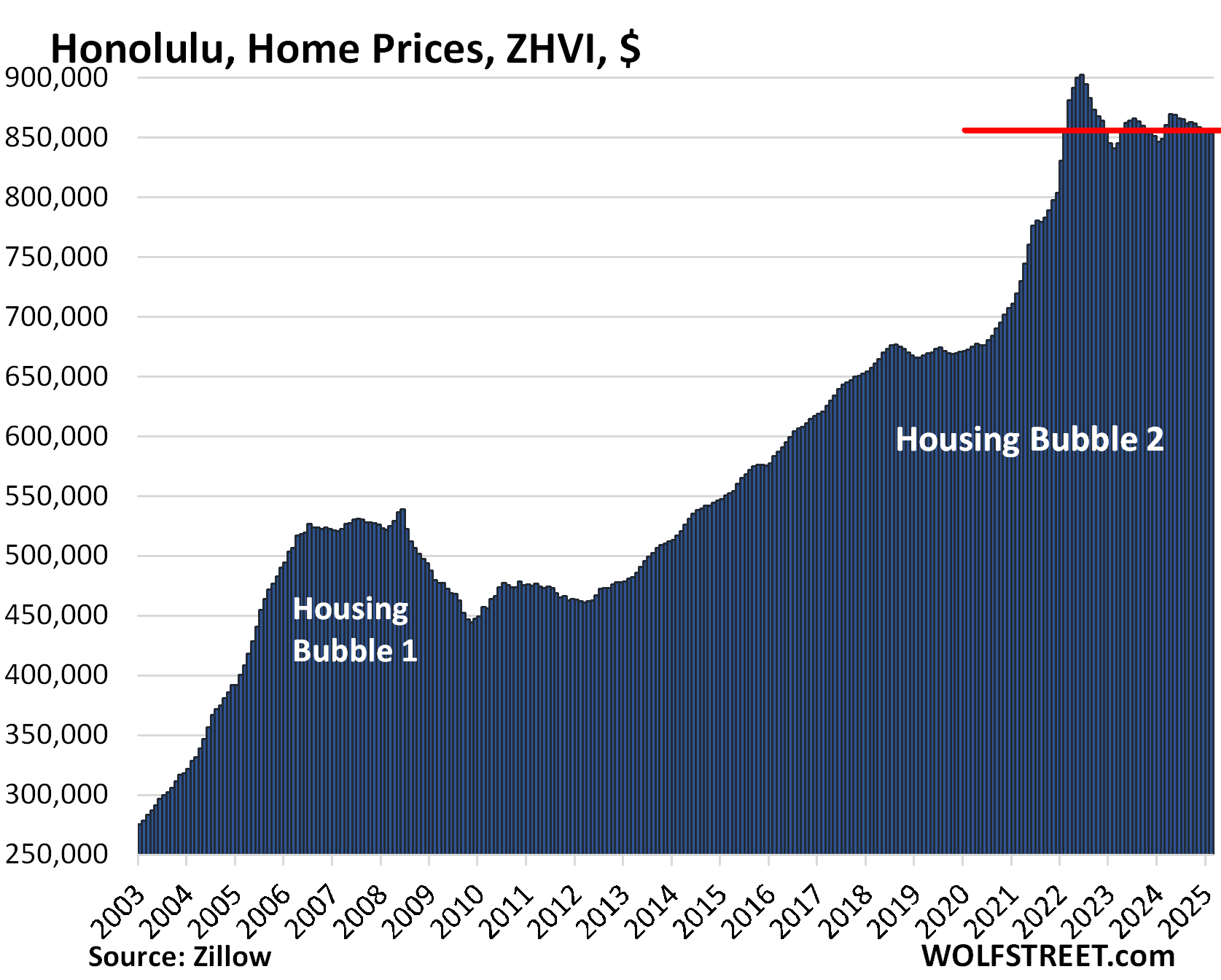

Honolulu, Home Prices

From Jun 2022 peak

MoM

YoY

Since 2000

-5.4%

0.0%

0.6%

278%

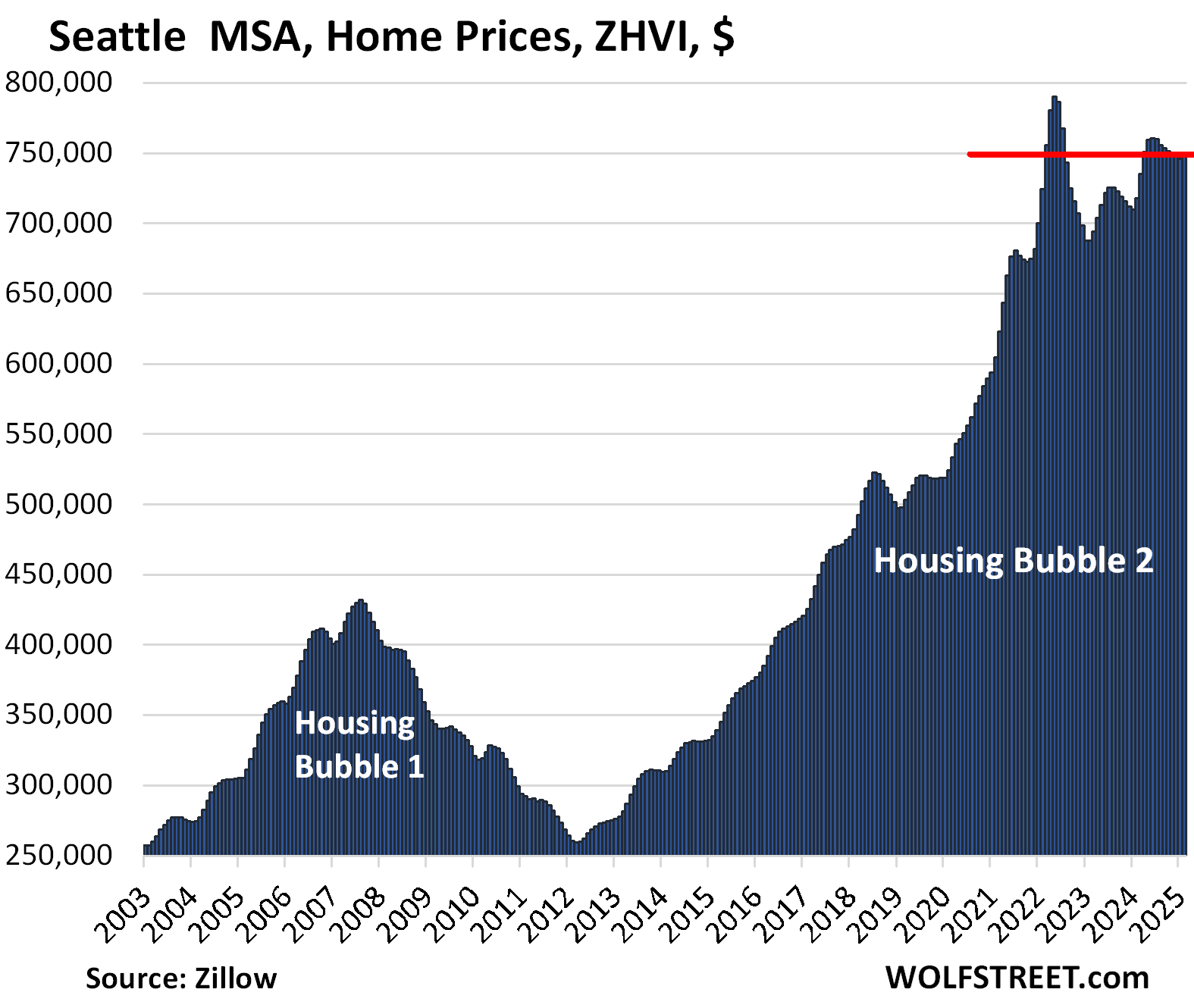

Seattle MSA, Home Prices

From May 2022 peak

MoM

YoY

Since 2000

-5.2%

0.4%

4.3%

238%

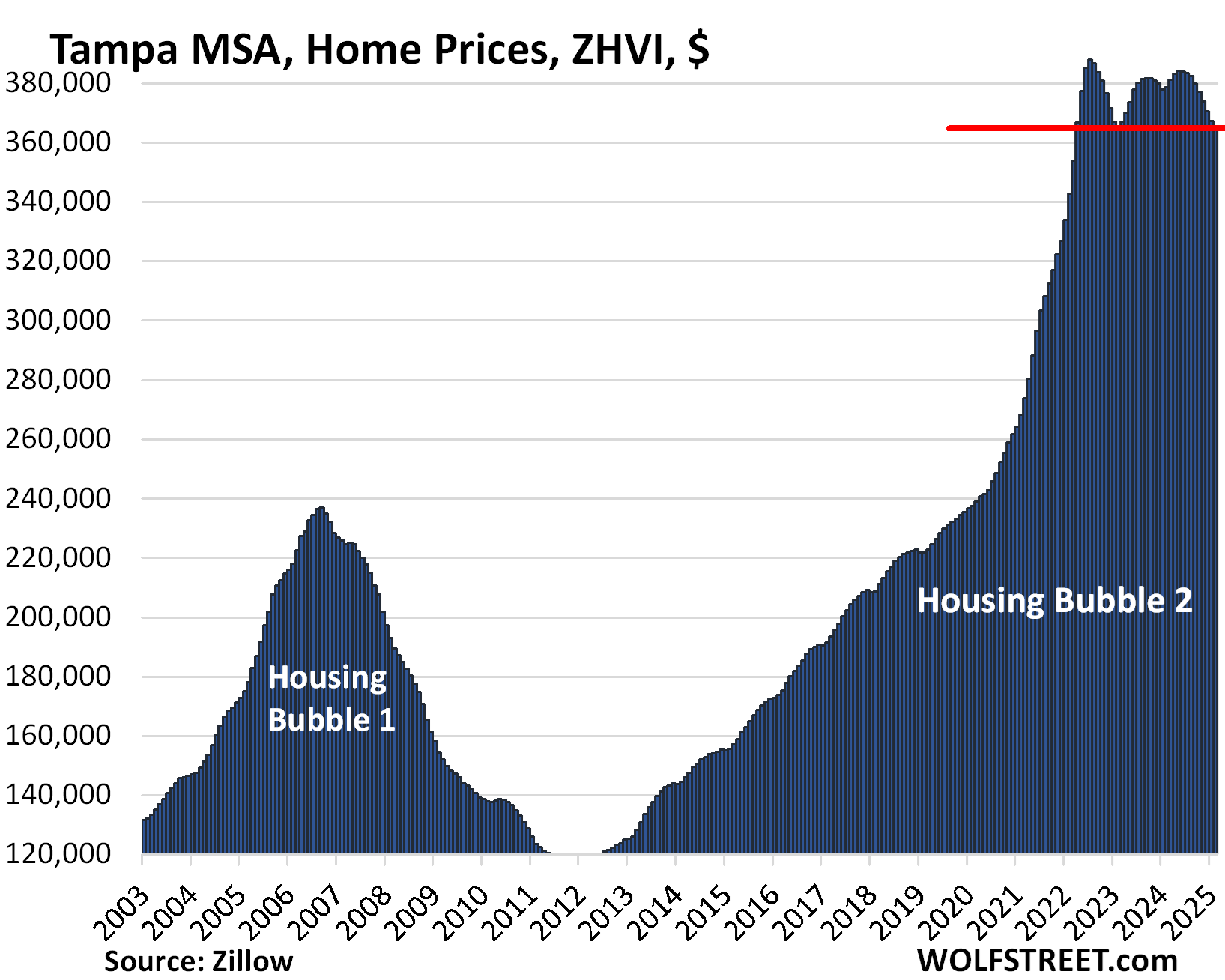

Tampa MSA, Home Prices

From Jul 2022 peak

MoM

YoY

Since 2000

-4.9%

-0.4%

-1.5%

207%

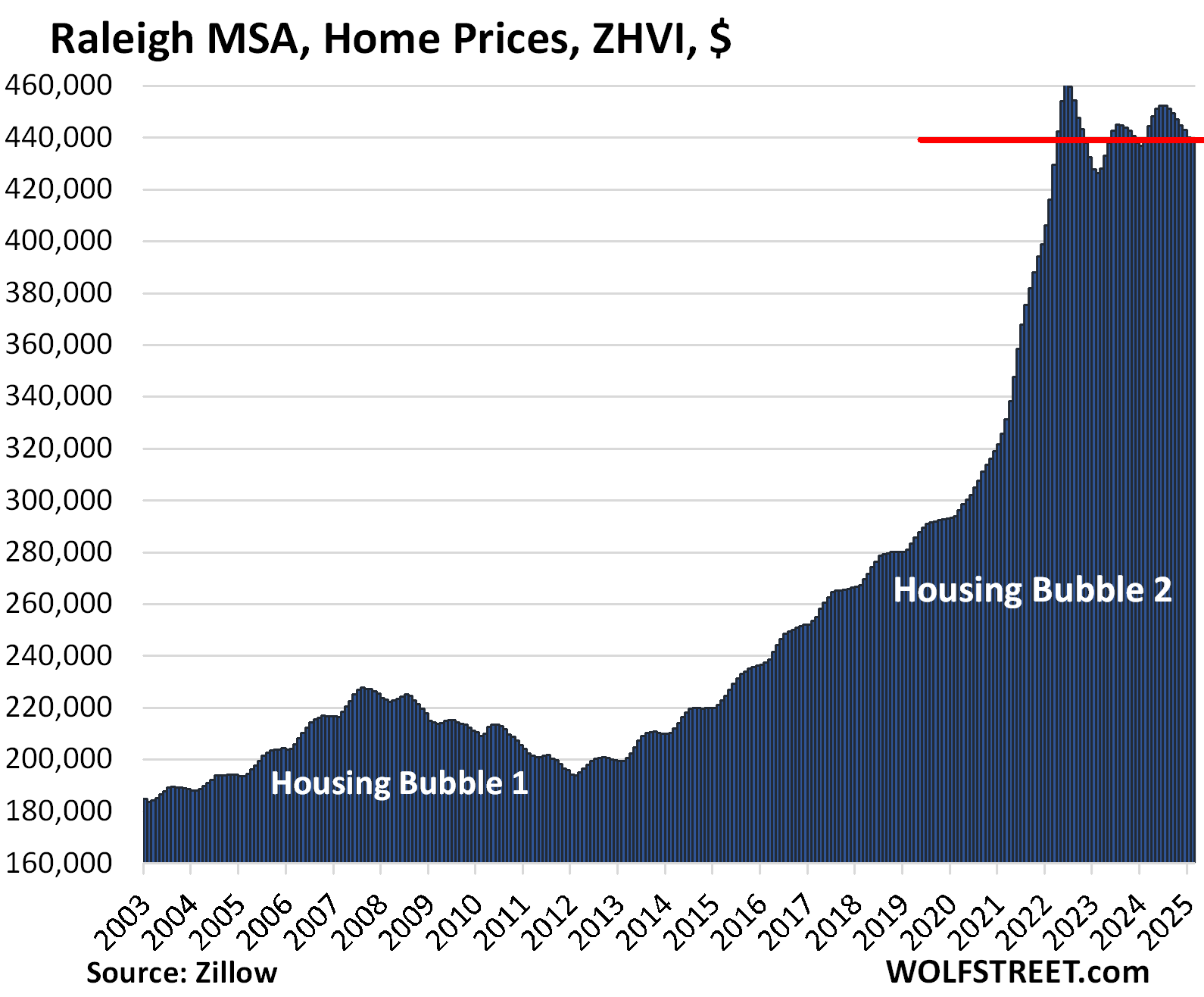

Raleigh MSA, Home Prices

From July 2022 peak

MoM

YoY

Since 2000

-4.6%

-0.2%

0.0%

155%

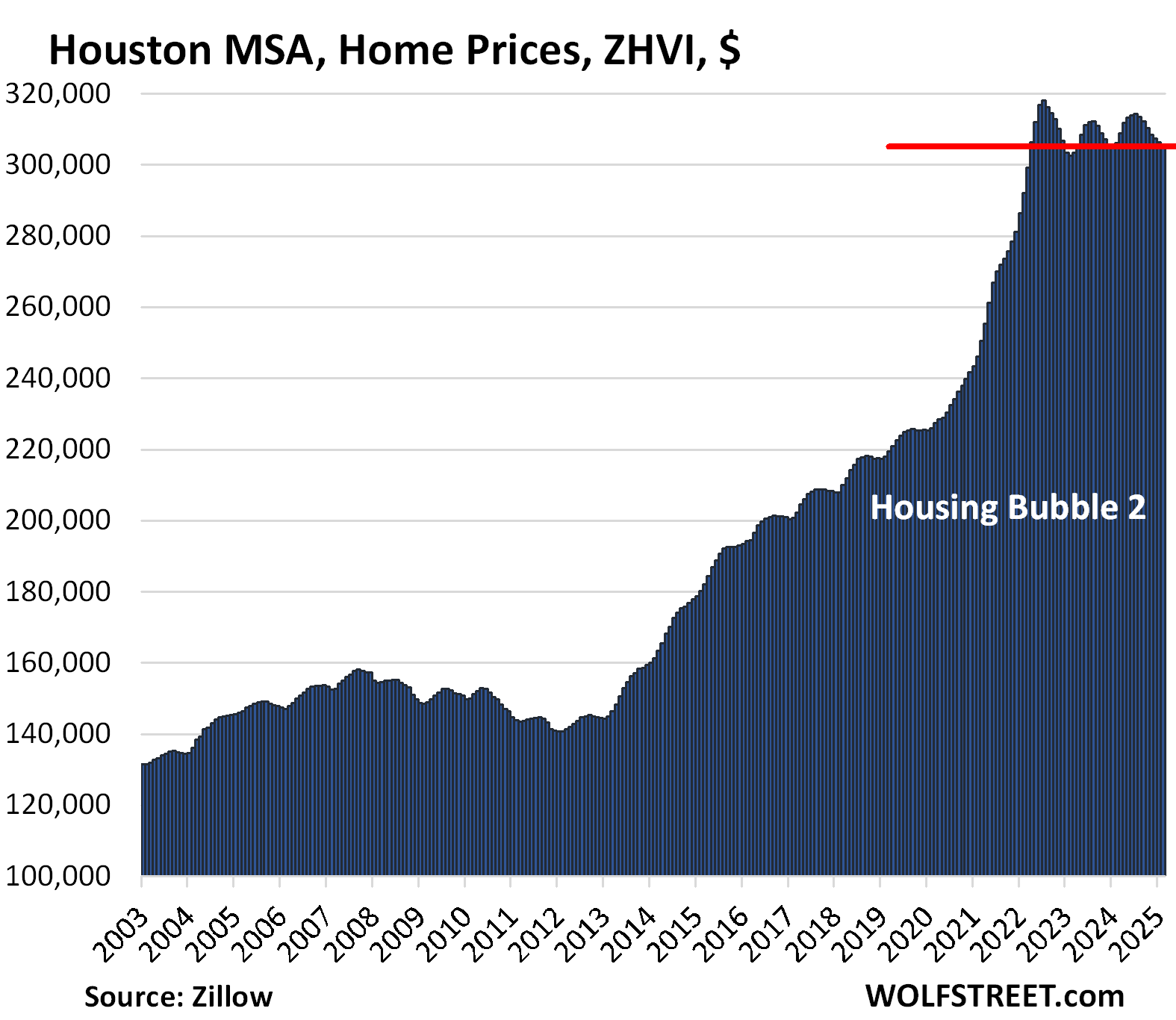

Houston MSA, Home Prices

From Jul 2022 peak

MoM

YoY

Since 2000

-3.9%

-0.2%

-0.2%

148%

First seen in April 2022.

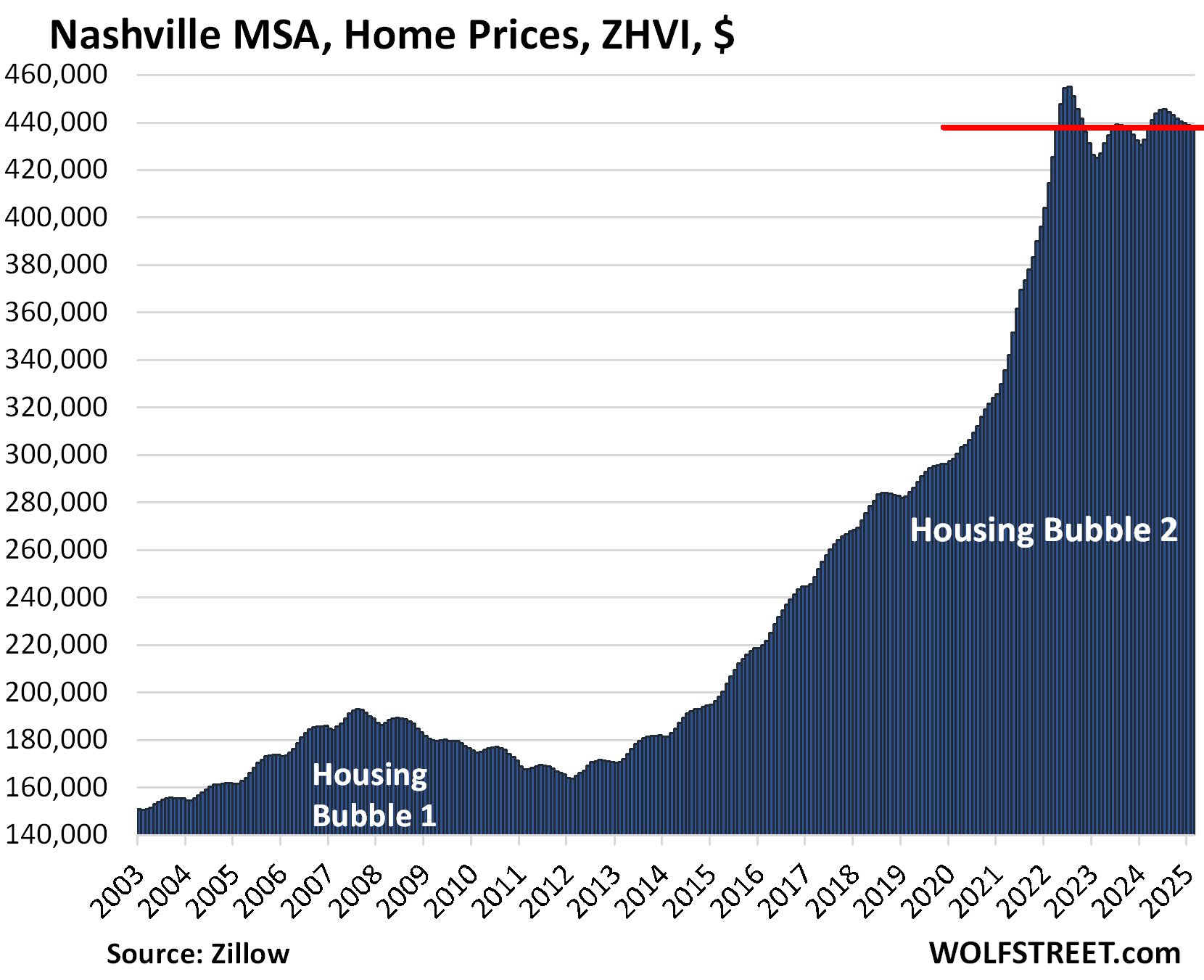

Nashville MSA, Home Prices

From July 2022 peak

MoM

YoY

Since 2000

-3.7%

-0.1%

1.3%

216%

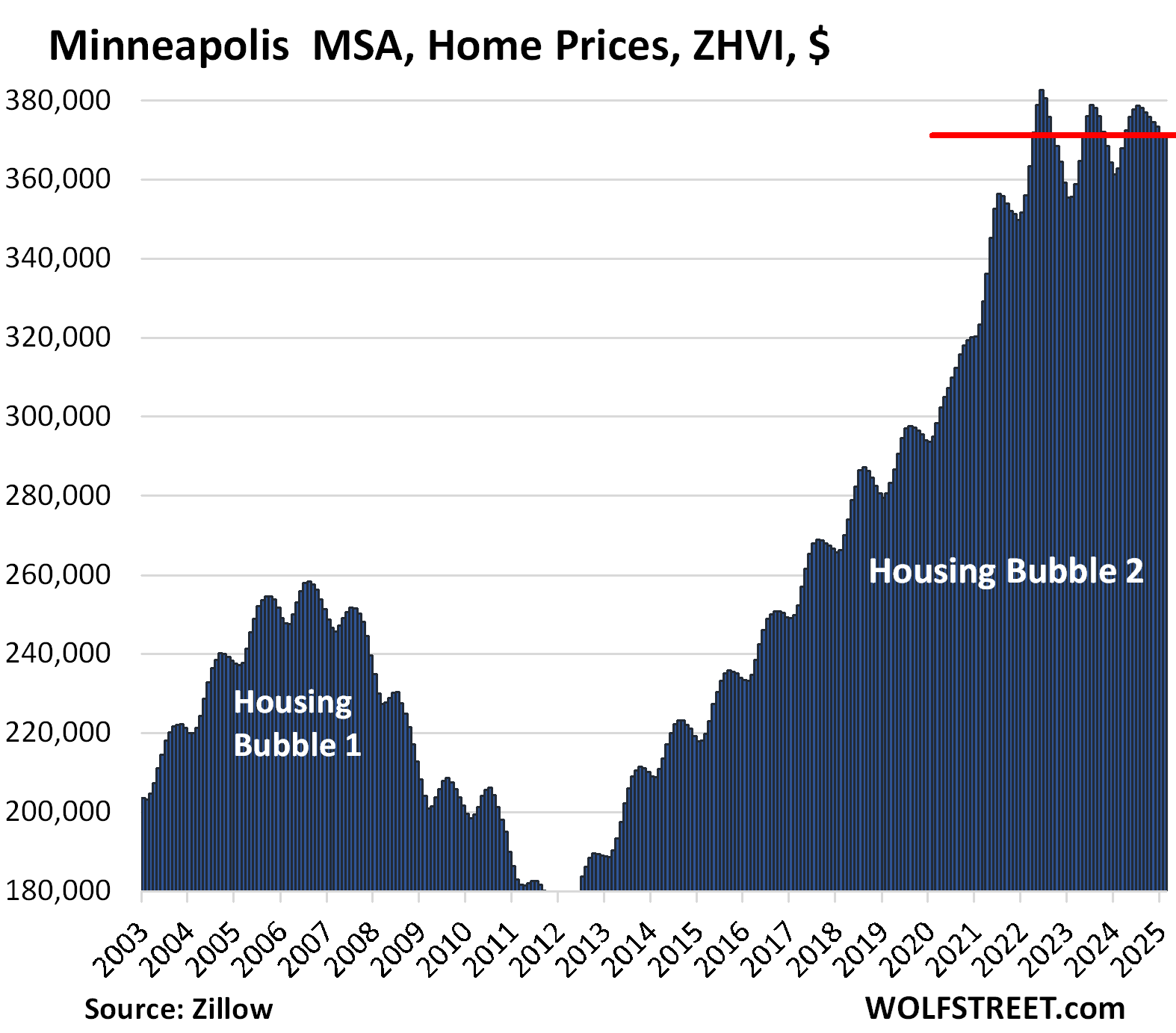

Minneapolis MSA, Home Prices

From May 2022 peak

MoM

YoY

Since 2000

-3.0%

-0.1%

2.4%

155%

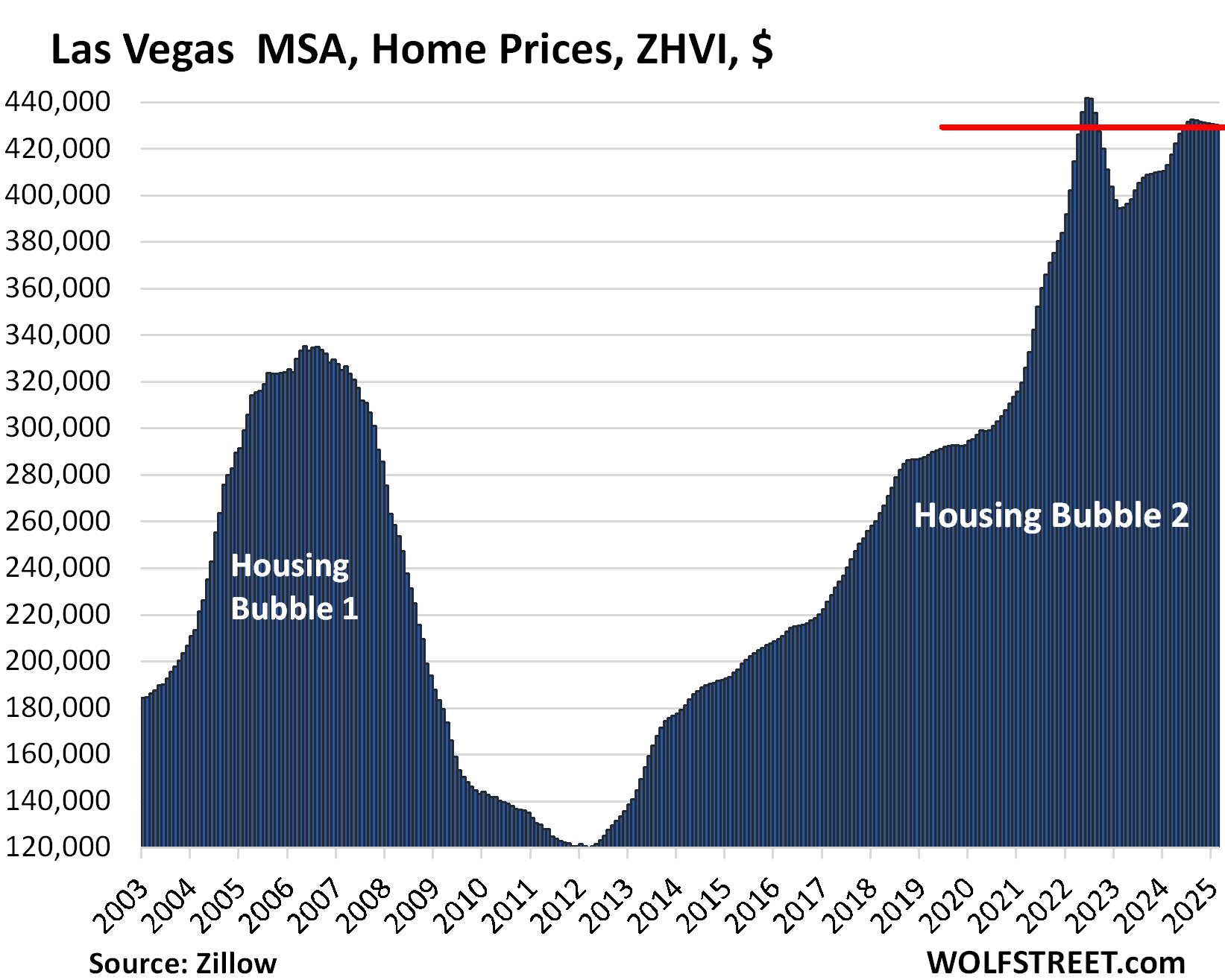

Las Vegas MSA, Home Prices

From June 2022 peak

MoM

YoY

Since 2000

-2.6%

-0.1%

4.2%

178%

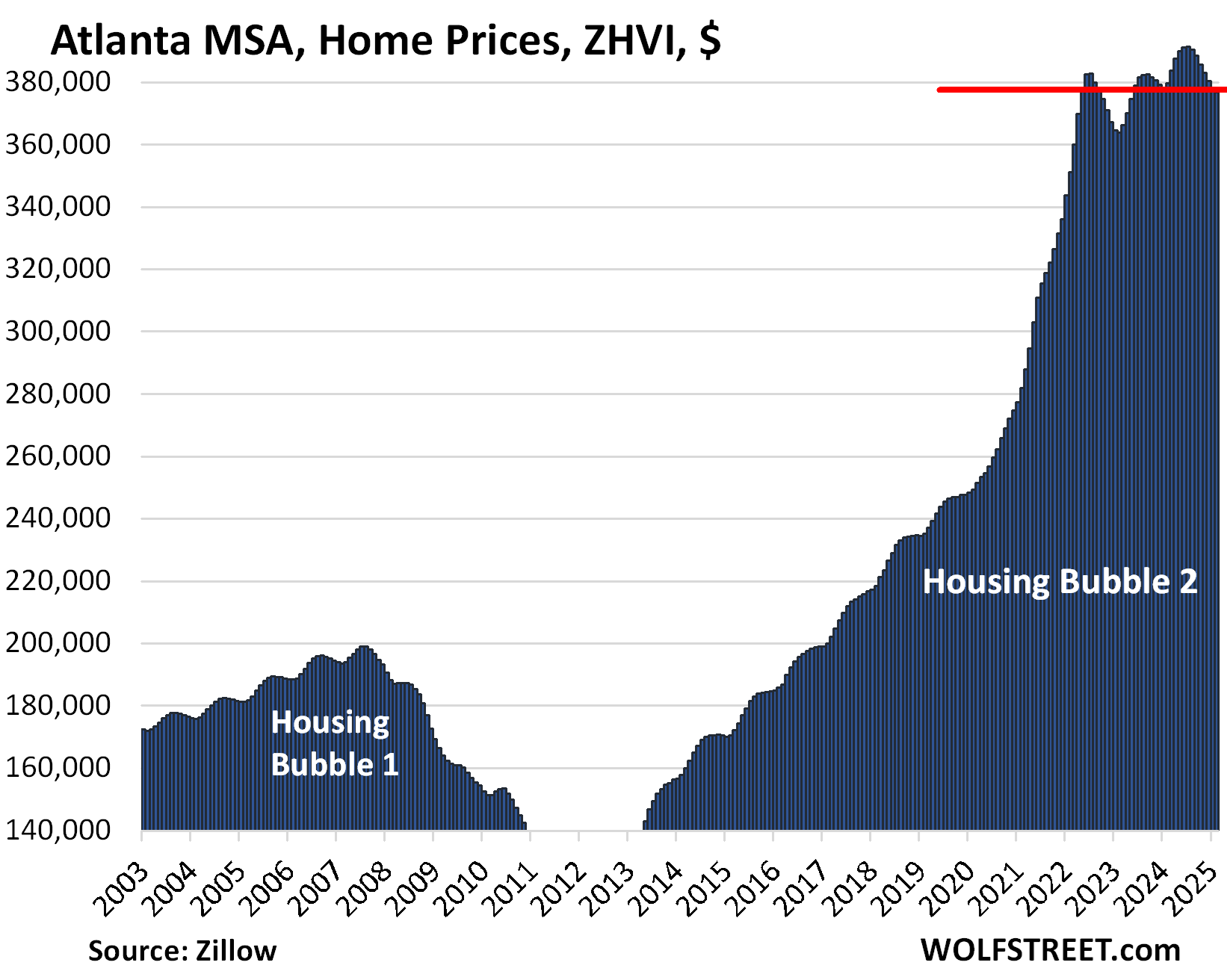

Atlanta MSA, Home Prices

From July 2022

MoM

YoY

Since 2000

-1.6%

-0.3%

-0.7%

158%

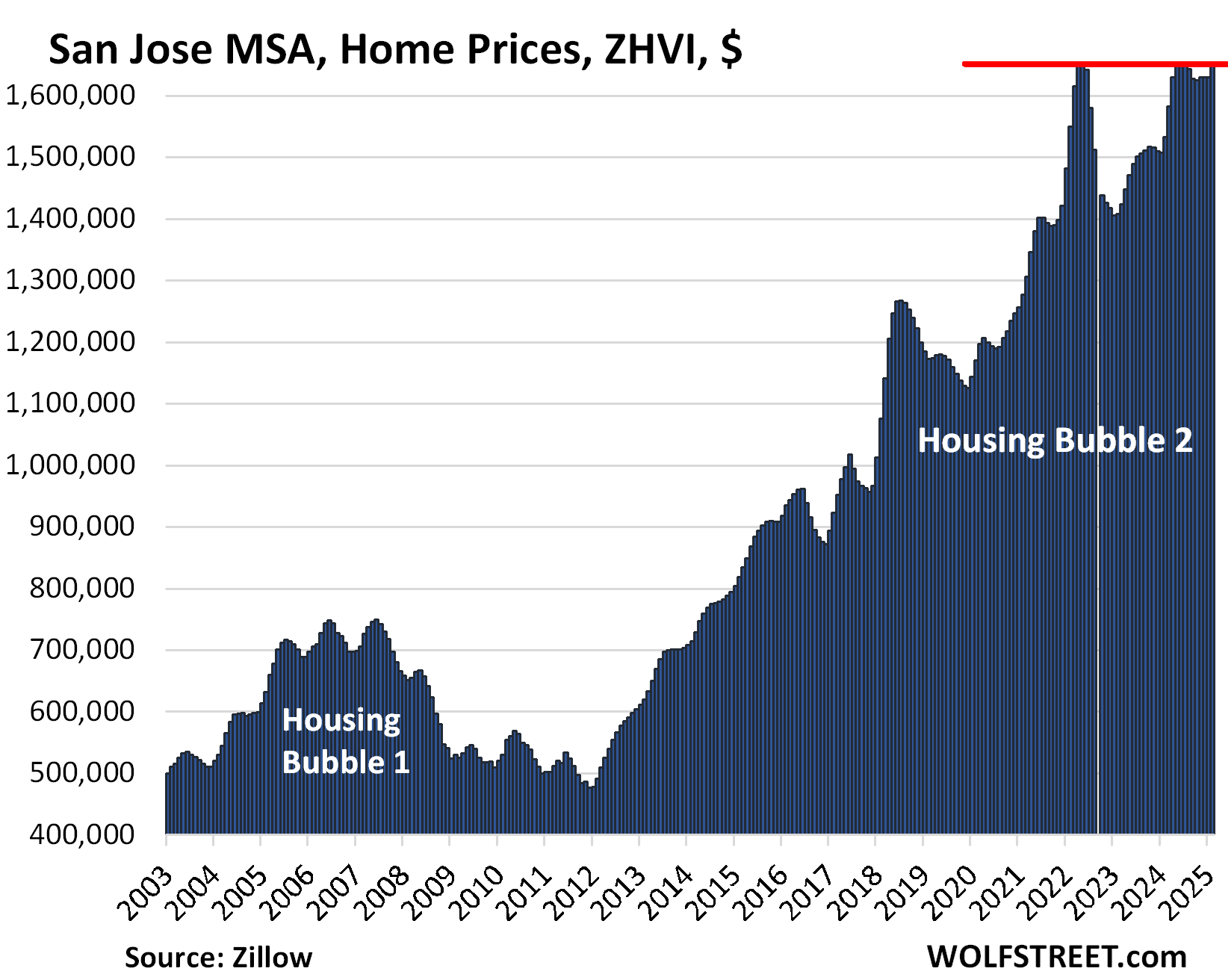

San Jose MSA, Home Prices

From May 2022 peak

MoM

YoY

Since 2000

-1.1%

1.1%

7.6%

342%

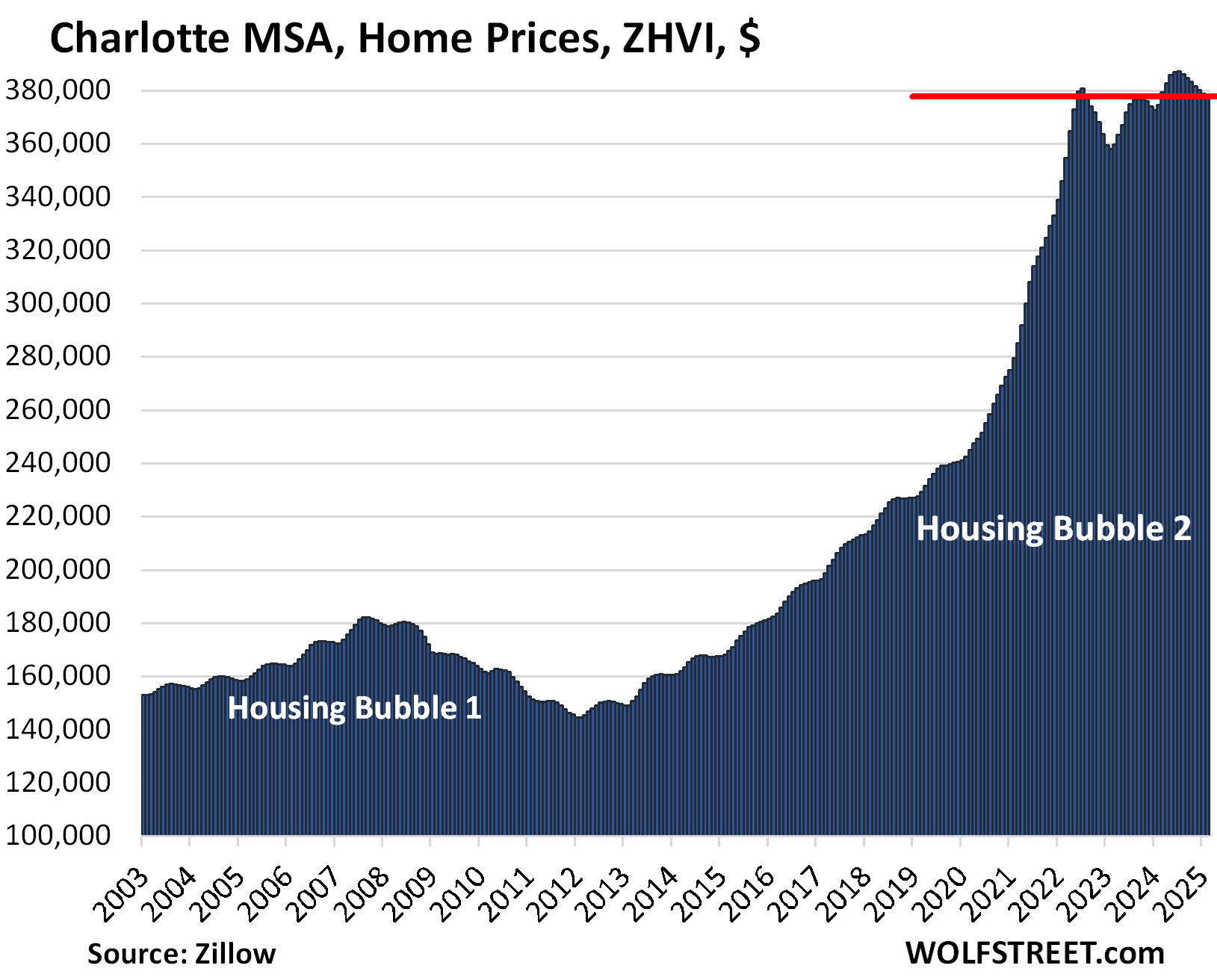

Charlotte MSA, Home Prices

From June 2022

MoM

YoY

Since 2000

-0.7%

-0.2%

0.9%

168%

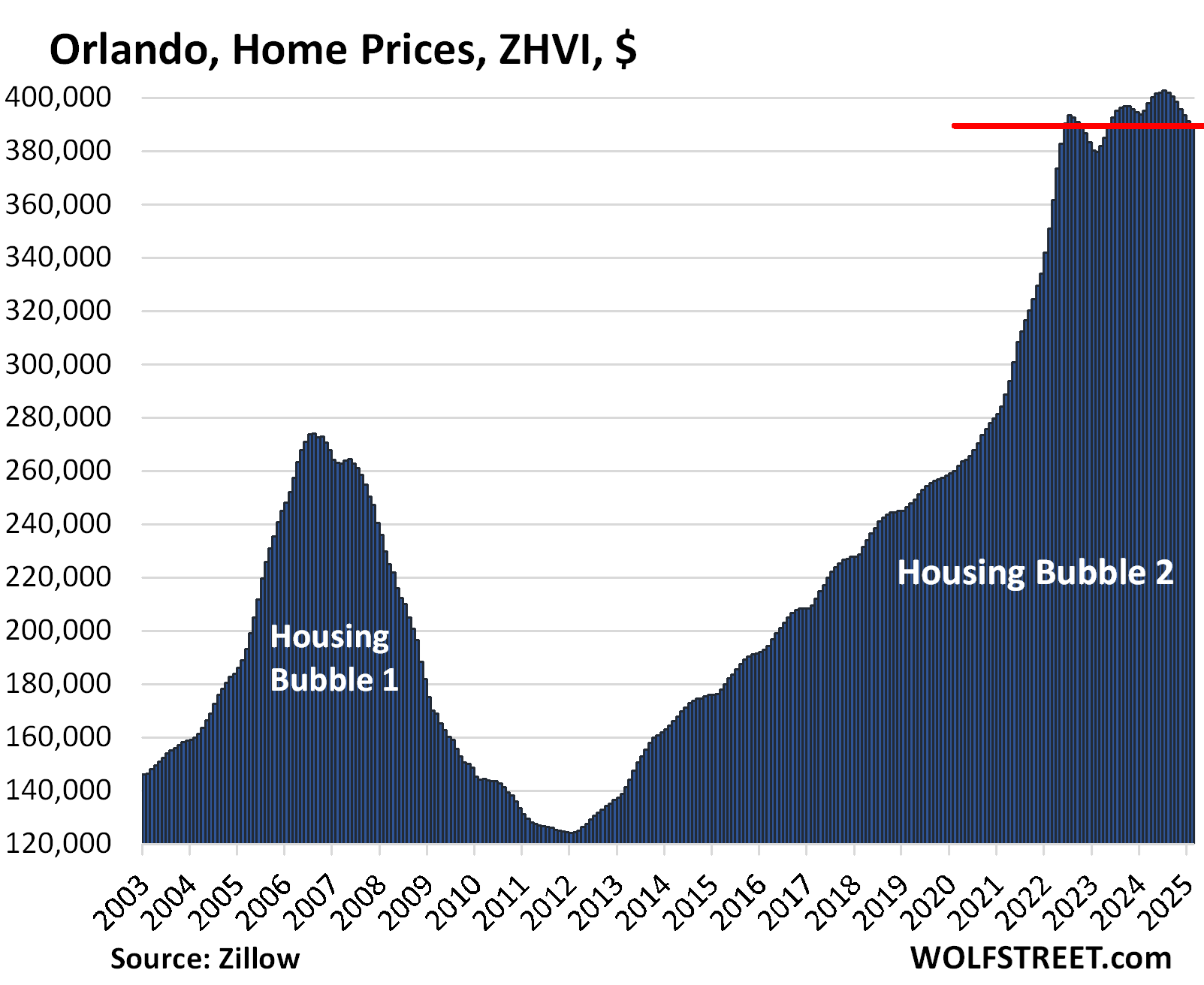

Orlando MSA, Home Prices

From June 2022

MoM

YoY

Since 2000

-0.92%

-0.4%

-1.4%

231.4%

The 12 markets that rose after mid-2022 (but some are now sagging):

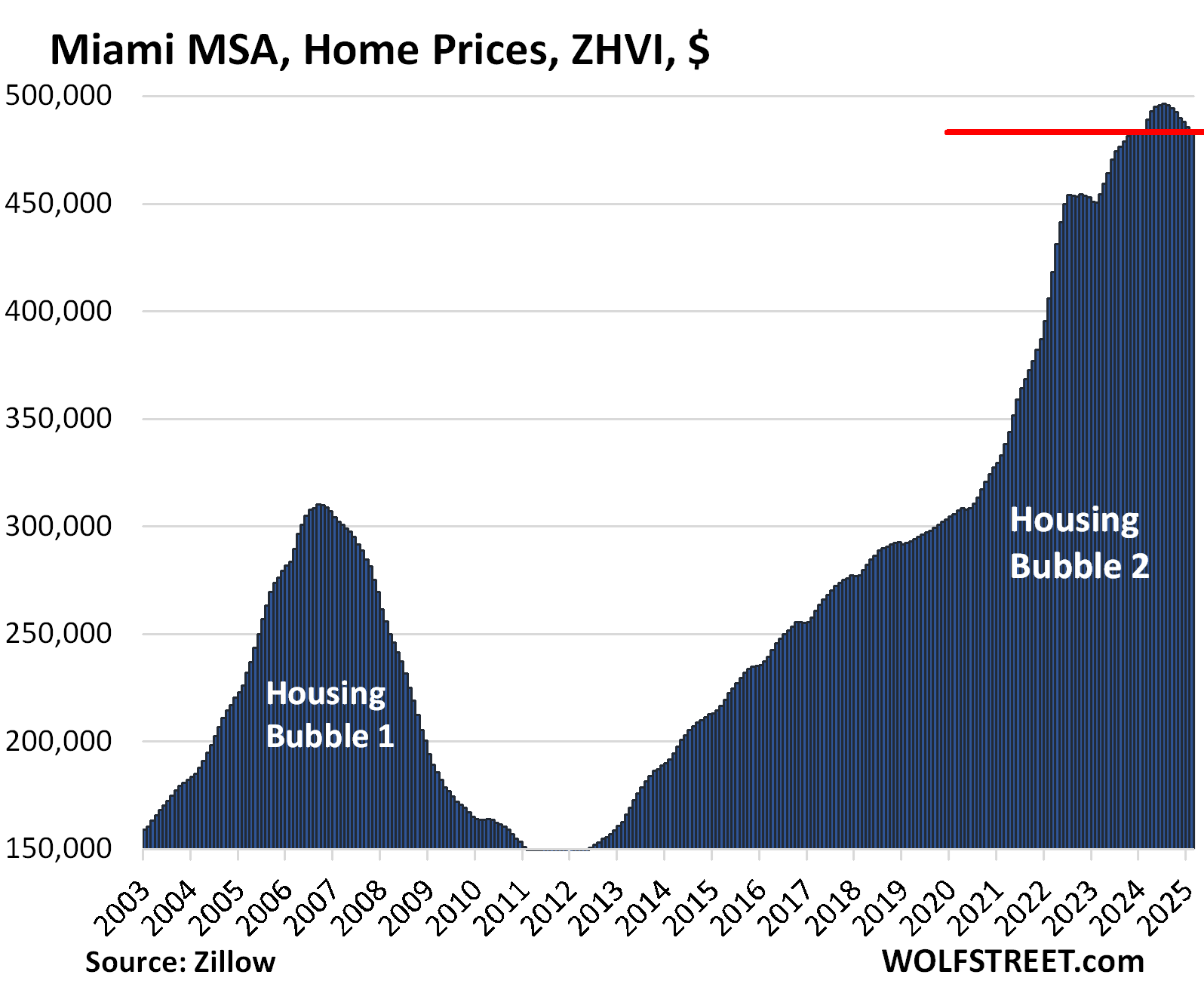

Miami MSA, Home Prices

MoM

YoY

Since 2000

-0.4%

-0.2%

325.6%

Miami prices have dropped enough to where they’re not down year-over-year.

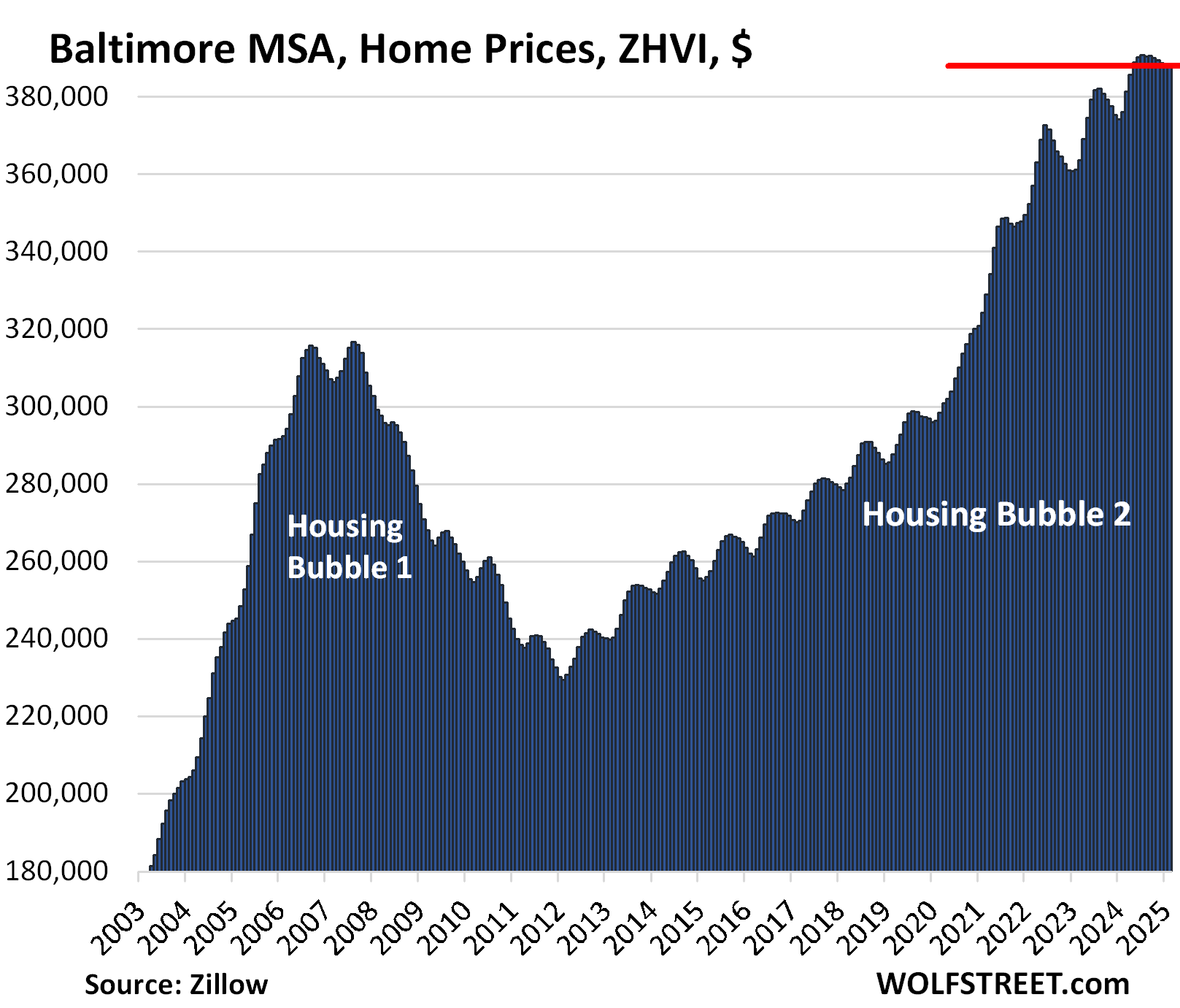

Baltimore MSA, Home Prices

MoM

YoY

Since 2000

0.0%

3.1%

173%

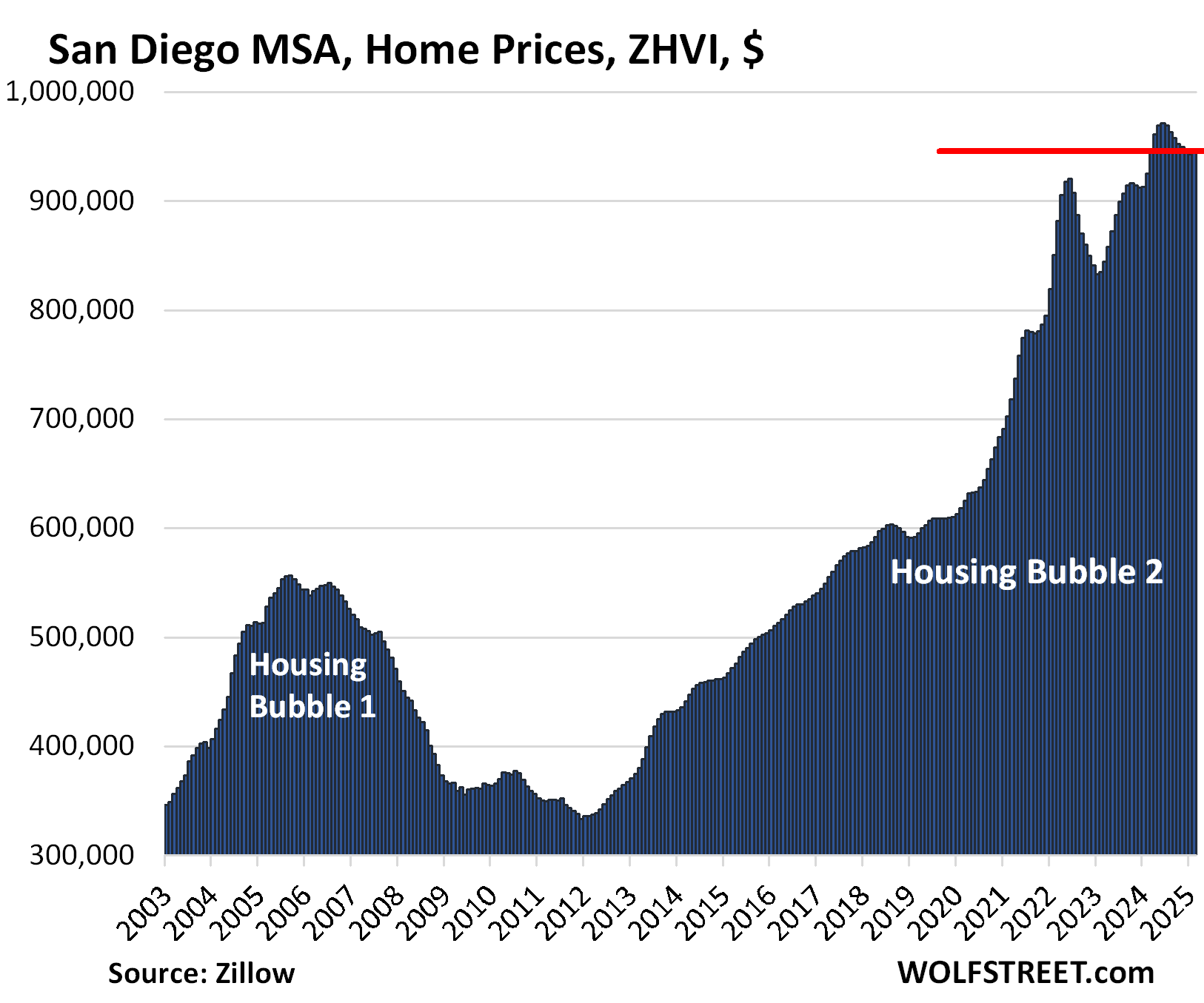

San Diego MSA, Home Prices

MoM

YoY

Since 2000

0.3%

2.3%

332%

Kansas City MSA, Home Prices

MoM

YoY

Since 2000

0.1%

3.1%

175%

Columbus MSA, Home Prices

MoM

YoY

Since 2000

0.0%

3.1%

152%

Washington D.C. MSA, Home Prices

MoM

YoY

Since 2000

0.3%

4.0%

216%

The vast and diverse metro includes Washington D.C. and parts of Maryland, Virginia, and West Virginia.

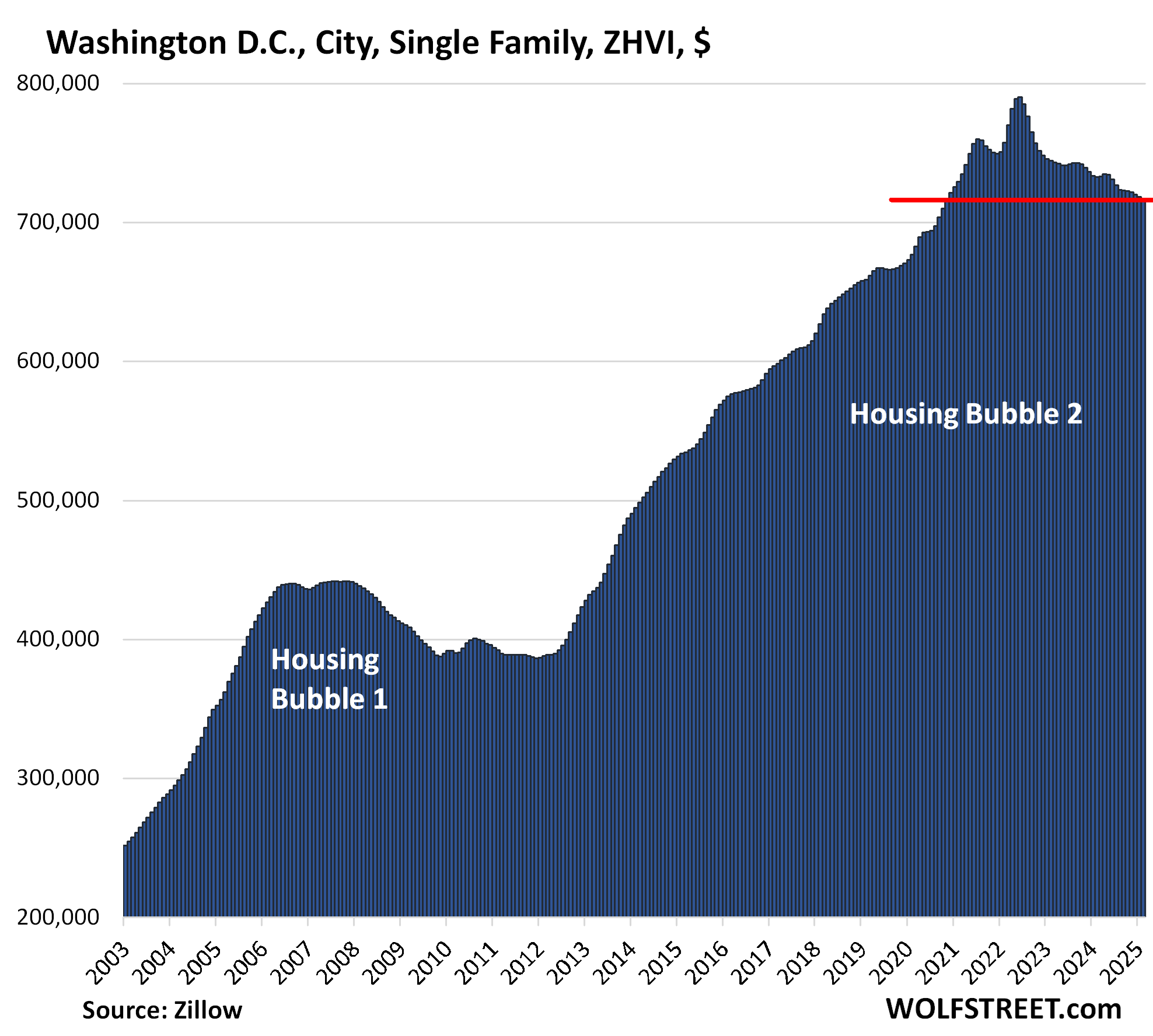

But in the city of Washington D.C., prices of single-family houses, seasonally adjusted, have dropped by 9.1% from the peak, and by 2.1% year-over-year, to the lowest level since November 2020. The example of Washington D.C. and the D.C. MSA shows how the dynamics can differ when narrowing down to the city itself:

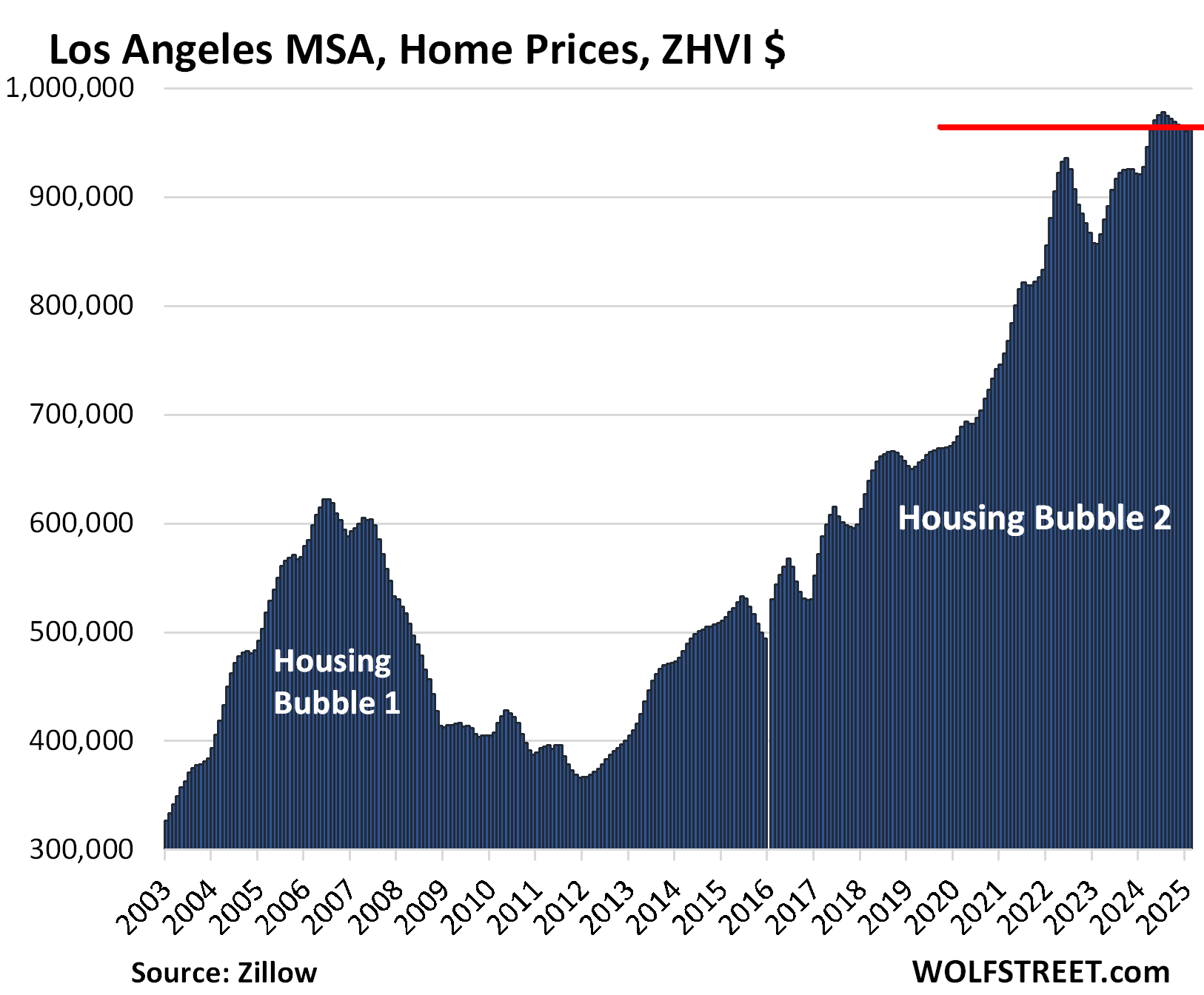

Los Angeles MSA, Home Prices

MoM

YoY

Since 2000

0.4%

3.9%

329%

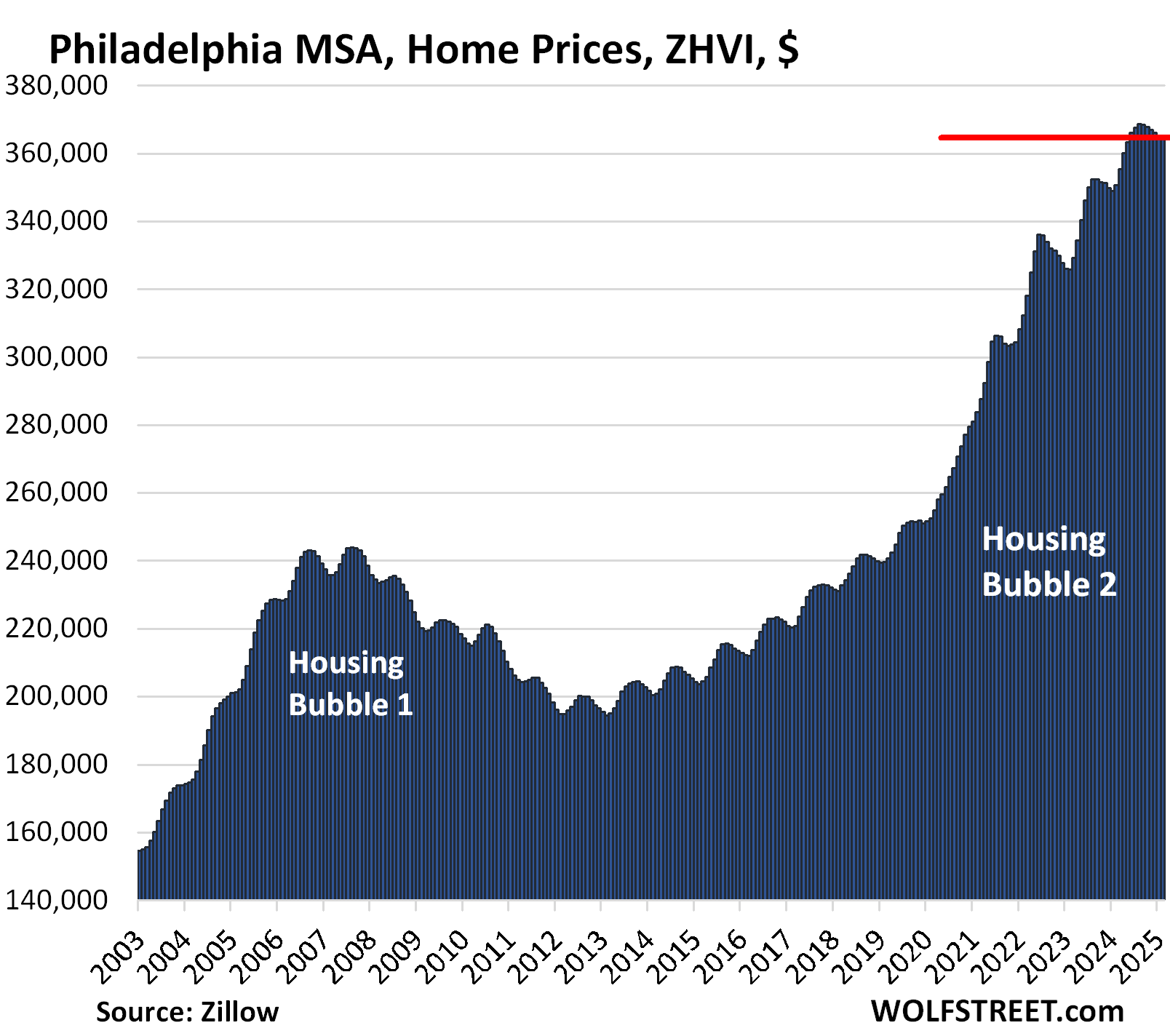

Philadelphia MSA, Home Prices

MoM

YoY

Since 2000

0.0%

4.1%

199%

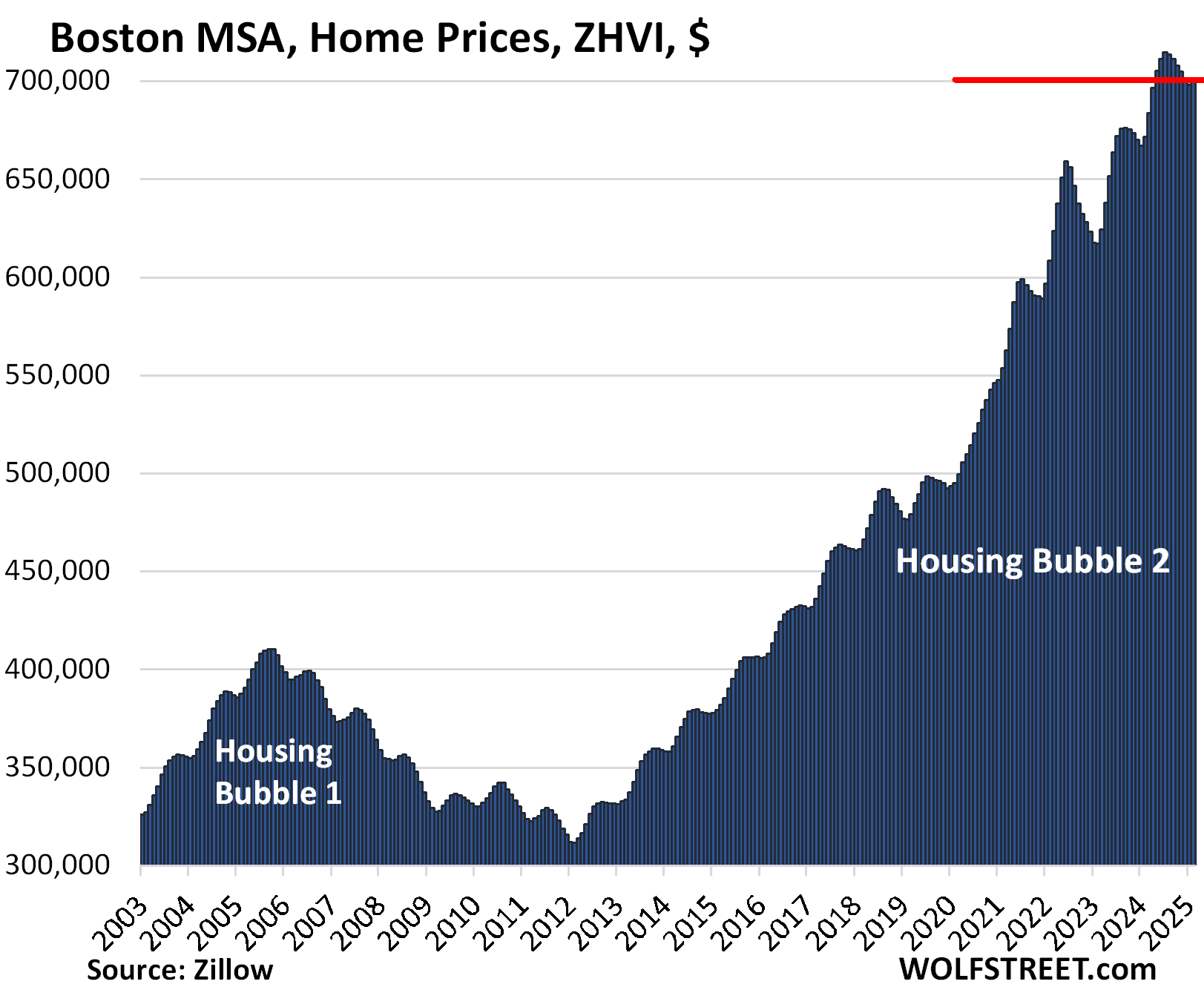

Boston MSA, Home Prices

MoM

YoY

Since 2000

0.2%

4.2%

223%

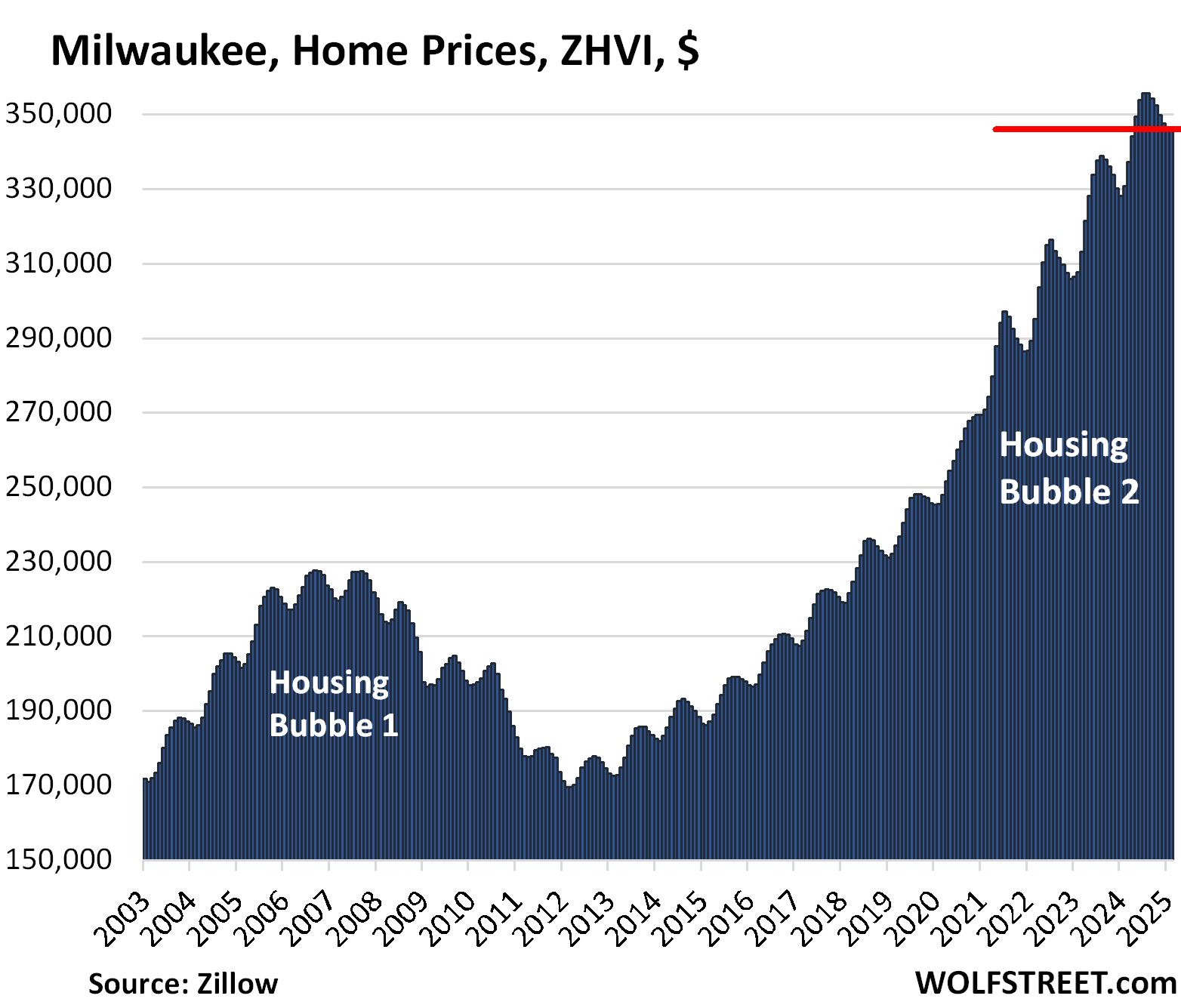

Milwaukee MSA, Home Prices

MoM

YoY

Since 2000

0.0%

4.7%

141.3%

Chicago MSA, Home Prices

MoM

YoY

Since 2000

0.1%

5.1%

111%

New York MSA, Home Prices

MoM

YoY

Since 2000

0.1%

5.6%

210%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

We have a new magazine launching today, designed to give the shipping industry an idea of how the markets might play out in the coming months. Today’s opening instalment looks at the trajectories of the world’s two largest economies.

Economists have been left flabbergasted by the opening months of Donald Trump’s return to power in the US, the international rulebook torn up, policies raining in and often being rescinded by the hour. Making a call on how the global economy plays out in the coming months has rarely been more tricky, or down to the whims of one man.

At no point since tracking began on the subject have global trade policies been more uncertain than right now, according to one index developed in the US.

I’ve rarely seen a year start with more uncertainty

The Trade Policy Uncertainty (TPU) Index developed by four employees at the Federal Reserve Board analyses the frequency of joint occurrences of trade policy and uncertainty terms in major newspapers, firms’ earnings conference calls, and aggregate data on tariff rates in a way that is similar to existing volatility indices in mainstream financial markets, spanning equities and derivatives.

Since Donald Trump returned to the White House on January 20, the index, which goes back to 1960, has spiked to record levels, twice as high as previous peaks registered during Trump’s first term in office.

A paper submitted by the creators of the TPU index documents that increases in trade policy uncertainty reduce investment and activity using both firm-level and aggregate data.

Trump’s first months back in the White House have dominated shipping headlines for tariffs, a push for peace in Ukraine, a renewed ‘maximum pressure’ strategy on Iran, the creation of a National Energy Dominance Council, and a planned tax on Chinese-built tonnage calling US ports.

The war of tariffs is beginning to make its way into the macroeconomic forecasts. As an example, Goldman Sachs just revised their US Q4 2025 GDP growth downwards from 2.2% to 1.7% whilst at the same time increasing their likelihood for a US recession within 12 months from 15% to 20%.

“As the Trump 2.0 reality show unfolds, as it does daily, often with singular market-moving tweets, we might as well suspend trying to make credible forecasts of future supply-demand balance across shipping sectors. Underwhelming spot earnings render shipping sentiment downbeat while we seek greater clarity on today’s geopolitical, trade and social threats,” notes a recent report from broker Hartland Shipping.

“I’ve rarely seen a year start with more uncertainty,” says Tim Huxley, the veteran head of Hong Kong shipowner Mandarin Shipping, adding: “Both the US and China want to see growth and they will do everything they can to achieve that. A stronger domestic economy in China will probably see the target of 5% growth met, in the USA, tariffs could lead to inflation and that could preocupy the new administration.”

If shipping markets in the 2020s can be characterised by disruption, then the two decades prior could similarly be defined with one word – China.

Without the growth in Chinese demand for commodities, manufactured exports and shipbuilding capacity witnessed since the start of the millennium, the shipping world would be an entirely different place.

China’s demand has been a solid factor supporting shipping markets amid economic and political upheaval, pandemic and war. But this drive was, at least initially, itself a disruptive factor.

Snakes like big ideas and understanding how things work

The opening of China’s economy, often marked by the country’s accession to the WTO in the early 2000s, changed the shipping game. Since then, the industry has become in large part dependent on ever-expanding Chinese demand.

For large oil tankers and dry bulk carriers, this is put in stark relief when we consider that Chinese imports of crude oil and iron ore do not just constitute the majority of global incremental import growth in these sectors over the period 2000-2024. Due in part to declines elsewhere, they exceed it.

Could this era of expansion go into reverse? In Maritime Strategies International’s view, the answer is yes.

There are structural shifts in China’s economy, MSI analysts point out, which will reduce demand for some of the major commodity types it will import. Perhaps the two of the most important of these trends are reduced rates of urbanisation and increased vehicle electrification.

John Michael Radziwill, a high profile owner who chairs Monaco-based C Transport Maritime, concedes that China has domestic challenges to its economy that it must address or risk slowing growth and internal discontent.

“We see the Chinese government as willing to drip feed support without really enacting enough policies that could turnaround the situation quickly,” Radziwill tells Splash.

The full ramifications for how relations between China and the US, the world’s two largest economies, will develop between Trump and his counterpart, Xi Jinping, still remain unclear.

“While we are all kept guessing as to what Mr Trump has in mind for US-China relations, let’s consider the Chinese astrological Snake: it is wise, mysterious and thoughtful,” says Mark Williams, who heads up consultancy Shipping Strategy: “Snakes like big ideas and understanding how things work. In this Year of the Snake, we could all do with some of these characteristics if we are to come out the other side in better shape.”

As well as markets coverage, this new magazine also covers pressing regulatory issues and likely tech breakthroughs. Click here to access the full magazine.

ENB Pub Note: This is an excellent article from Bloomberg about the potential for low-cost Russian natural gas to return to the European market. There are several key points to note while reading this article. President Putin has done an excellent job for Russia, replacing Europe as a customer with the Asian markets. As George McMillan has said, “All Putin has to do is nothing, and he has won,” not only the Ukraine war but also the financial battle with the West. The left governments have de-industrialized Germany and much of Europe even without the removal of Russian natural gas. Their horrific energy policies have killed economic growth, and it will be decades of recovery with or without Russian natural gas. Russia has moved on, and it would be nice to sell to the European markets, but make no mistake: they do not need the EU’s markets and only want the land that they occupy in Ukraine to block an invasion. History has shown that was the path for the last three invations into Russia. So, the European markets need Russian gas more than Russia needs a new customer. Not many countries grew their GDP in 2024, and Russia was in the 4% growth range even with heavy sanctions and shipping fewer products to Europe.

Russian President Vladimir Putin seems confident that pipeline flows of natural gas to Europe could be stepped up if a US-brokered deal to end the war in Ukraine is agreed — raising questions about whether the continent is willing to reverse course and revive that relationship.

“If, say, the US and Russia agree on cooperation in the energy sector, then a gas pipeline for Europe could be ensured,” Putin said at a briefing in Moscow on March 13. “And this will benefit Europe, as it will receive cheap Russian gas.”

But while some traders are speculating that Russian supply will increase, many expect limited volumes to return, if any. The European Union is working on plans, albeit delayed, to end its dependence on Russian energy by 2027.

None of the options to ramp up pipeline flows are particularly straightforward. The simplest would perhaps be a resumption of last year’s levels of gas transiting through Ukraine, which came to a halt at the end of December. These volumes met less than 5% of Europe’s total gas demand.

Source: Grida data

Why would Europe consider pivoting back to Russian gas?

It’s the “cheap” aspect that Putin mentions that could convince some countries in Europe to overlook their geopolitical concerns. The EU has made considerable headway in curbing its appetite for Russian gas after more than five decades of overwhelming reliance, but continued pricing pressures could test the bloc’s resolve.

Europeans are still paying more for gas three years after the region’s worst energy crisis in decades. And in the EU’s largest economy, Germany, some industries are hoping for a return of Russian supply as high energy costs weigh on their ability to compete with manufacturers abroad. Countries in Eastern Europe that used to rely on the Soviet-era flows of gas, especially Slovakia, have also been pushing for Russian pipeline volumes to come back.

On top of that, gas storage has become a bigger concern this year after a cold winter and drop in wind power generation saw the continent burn through its reserves more quickly. Europe faces a tough and expensive refilling season before the next winter starts, and any meaningful increase in gas supply in a tight market would bring much-needed relief.

Why is Putin optimistic that Europe will buy more Russian gas?

The potential for warmer relations between the US and Russia is key here. Russian and European officials say the US is exploring ways to work with Russian state-run gas giant Gazprom PJSC on global projects. Gazprom is keen for the US to help restart its Nord Stream pipelines between Russia and Germany, people familiar with the matter told Bloomberg News.

Gazprom has a majority stake in Nord Stream and is the sole owner of Nord Stream 2. For the latter pipeline, its Switzerland-based operator — a subsidiary of Gazprom — is in the middle of insolvency proceedings. An American investor with experience doing business in Russia, Stephen Lynch, was reportedly interested in acquiring the operator if it’s declared bankrupt. That would effectively give the US a stake in the project.

Sanctions relief could also unlock more exports of Russian liquefied natural gas, which Europe imported record volumes of last year. Russia has spare capacity as its newest project, Arctic LNG 2, controlled by Novatek PJSC, only managed to start limited shipments in 2024 before stopping due to sanctions imposed by the US and its allies. The curbs restricted access to ice-class tankers needed to navigate frigid northern waters and made foreign buyers reluctant to buy cargoes.

US President Donald Trump has previously said some sanctions on Russia could be lifted as part of a peace deal in Ukraine, but muddying the picture are his own ambitions to sell more US LNG to Europe.

How much Russian gas is Europe buying right now?

Prior to the invasion of Ukraine, Russia was Europe’s biggest provider of gas, serving around 40% of the region’s demand and delivering the fuel through several pipelines to more than 20 countries.

That share had fallen to around 14% in 2024, according to the International Energy Agency. Most European buyers turned to alternative sources after dropping or being cut off by Russian suppliers, or found ways to use less gas. Some countries, such as the UK, Baltic states and Germany decided to stop imports of all Russian gas back in 2022, although Germany still receives some volumes from its neighbors that buy LNG from the east, including Belgium and France.

Europe’s imports of Russian LNG mean Russia is still one of the continent’s top sources of gas. But in terms of pipeline flows, Russia now sends a mere fraction of what it used to, as only one route — a single leg of the TurkStream pipeline that feeds into Hungary, Serbia and Slovakia via Turkey and under the Black Sea — remains operational.

What are the barriers to Russian pipeline gas returning to Europe?

For one, the EU has been working on a plan to phase out its remaining imports of Russian energy by 2027. While publication of the document has been postponed, the European Commission has said that the strategy is still being prepared.

In addition, many of Europe’s ties with Russian gas suppliers have been severed or soured in recent years. Some of the biggest and oldest customers of Gazprom, including German utility Uniper SE and Austrian energy firm OMV AG, have terminated their long-term contracts to buy gas after arbitration rulings.

Others, such as Eni SpA in Italy and Engie SA in France, have pending lawsuits against the Russian company, seeking compensation for the halt of deliveries in 2022. They would likely be reluctant to resume purchases before all claims are resolved.

There are also infrastructure bottlenecks. Both lines of the undersea Nord Stream pipeline were damaged by sabotage in 2022, with the perpetrators still unknown. The explosion took out one of the lines of the Nord Stream 2 pipeline too. While the other string remains intact, the system has never been certified for use by Germany.

Putin has repeatedly said that the undamaged string of the Nord Stream 2 pipeline is ready to supply Europe with Russian gas. Even in the unlikely event the German government reversed its opposition to this, the link would first require some maintenance as the last technical tests were conducted more than three years ago. It’s unclear how long such work would take.

Source: AW Consulting

Flows through another network, the Yamal-Europe pipeline that runs across Poland, could be revived after stopping in 2022, but the Polish government would need to approve the reopening and has been firmly opposed to receiving gas from Russia.

And then there’s the possibility of restoring the transit of Russian gas via Ukraine after a five-year agreement expired at the end of last year. While this option could be win-win for both sides — bolstering the revenues of Gazprom and bringing back transit income for Ukraine — talks between the Russian gas giant and its Ukrainian counterpart Naftogaz have historically been painful and lengthy.

There’s also uncertainty over how much damage the gas network in the area has sustained after both Russia and Ukraine recently intensified their military efforts, including in Russia’s Kursk region, home to a key cross-border gas point that used to transit gas last year.

The Reference Shelf

Bloomberg Opinion’s Javier Blas explains why the return of Russian commodities to the global market isn’t a question of if, but when.