Energy News Beat

This BLUFF is the reverse corollary to the Russian Natural Gas and Global Geopolitical Realignment series of papers and videos that was originally posted on Energy News Beat beginning on December 10, 2023.

It is also based on the “Role of Energy in the Kennan Five Power Center” Sea Power versus Land Power series of slide sets and videos that I recorded on the Felix Rex/Black Pigeon Speaks channel since March of 2022, and subsequently the Working Brother and Monster Consortium channel in YouTube since December of 2022.

The bottom line is that Europe in general, and Germany in particular, has created an energy calamity in Europe all of its own making and there is no reason for Trump to let the American economy go down the tubes with the “strange death of Europe” as Douglas Murray expresses the phenomenon.

The Greens shut down the coal-fired energy plants and the nuclear energy plants as the neoconservatives and neoliberals were weening themselves from Russian natural gas and the Russian electrical grid.

Throughout this multiyear process from the COVID-19 lockdown period to the present, the German industry has been declining for multiple reasons, but cannot stay in business with higher energy costs. The automotive industries are collapsing across Europe due to several longstanding inefficiencies and the rising energy costs are the final nail in their collective coffins.

They are no longer globally competitive for several reasons, energy being a major reason.

Populist Parties in the UK and Europe

Because of the rising energy costs and the declining economies, populist movements have been increasing across Europe.

This has created the conditions under which “all Putin has to do is nothing.”

COA 1, the European economies become non-competitive globally and collapse.

COA 2, the populist parties rise to power in the entire Danube River Valley in 2025 and 2026, and rebuild Nordstream, buy Russian natural gas to rebuild their economies, pay in Rubles and exit the EU, NATO, the Petrodollar and the neoconservative disaster in Ukraine.

Putin and Xi Jinping are fine with either outcome. This is why the theme for “The Kellog Plan is DOA” series of papers and videos is “all Putin has to do is nothing.”

The EU and the CDU/CSU floated the idea of purchasing Russian natural gas via the single functioning pipeline of Nordstream to avoid election losses across Europe.

But it is simply not in Putin’s best interest to save the EU and the CDU/CSU and therefore save NATO.

It is in Putin’s best interest to “do nothing” other than watch the EU and the WEF-backed globalist politicians either collapse their economies or get replaced by populist politicians and political parties.

It is apparent that Keith Kellogg (and the rest of the television generals) were/are not the least bit aware of the role of “energy” in the Sea Power versus Land Power Grand Strategies. Kellogg’s idea that “Trump can deal with Putin from a position of strength” to end the war in Ukraine before Spring is ludicrous to anyone who understands the role of “energy in geopolitical realignment.”

The Kids’ Table in Europe and the Adults’ Table in Riyad

This is why Kellogg was left at the kids’ table in Europe while the adults were discussing “Pipelines and Petrodollars” and “the role of energy in geopolitical realignment” at the adults’ table in Riyad.

As discussed on the Energy News Beat and Working Brother channels over the Winter where I began to explain why Putin was winning the War in the Orthodox Christian Russian-speaking areas in the Donbas against the Catholic Ukrainian speakers who are experiencing a 7:1 KIA/WIA ratio catastrophic loss in the Donbas. The effort of the WEF Globalist neoconservatives to take over the Russian Black Sea Fleet in Crimea and Russia’s only warm water ports has failed.

Meanwhile, the Western mass media complex repeats the trope that “Putin invaded for no reason” and Ukraine is winning the War” on a 24/7/365 non-stop news cycle and employs mass censorship on anyone who has an understanding of the history of the Sea Power versus Land Power Grand Strategies.

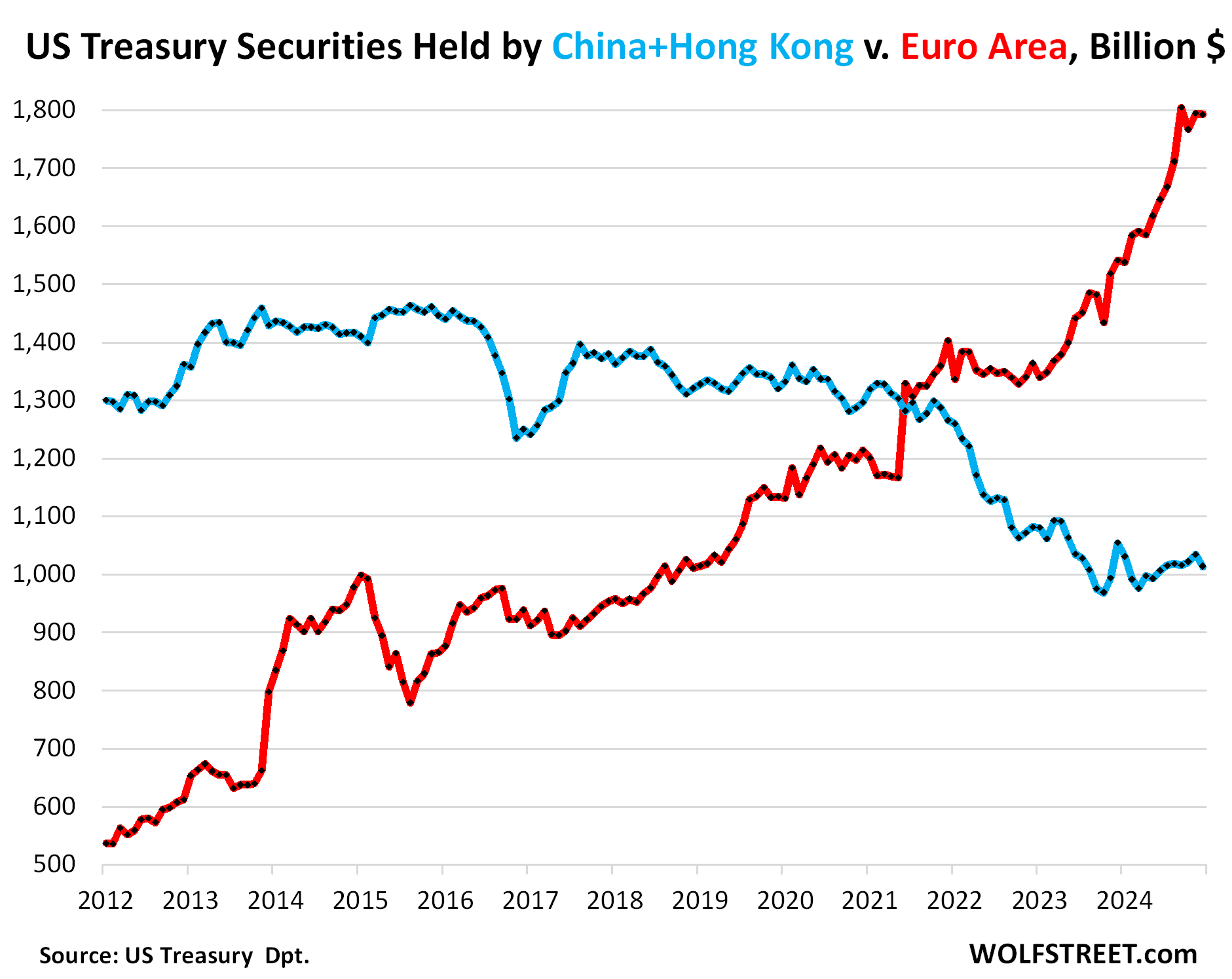

Now Putin has all the cards because he is (a) still selling petroleum products on the global market, (b) the oil, natural gas, and LNG are still being purchased by Europeans at much higher prices because more middlemen are involved, and (c) Putin is selling more energy to China whose products are becoming more globally competitive.

For these three basic reasons, the Kellogg Plan was a complete non-starter from its inception last April and, surprisingly, Trump’s team did not know this until the articles appeared on Energy News Beat and were pushed forward by Michael Yon’s Green Beret grapevine in late January (2025).

Since late January the Trump advisors have come to realize that “all Putin has to do is nothing” only after they realized that Putin was avoiding having any meetings with Trump and came to learn of the stories posted on Energy News Beat.

Putin and Trump both Need to Distance themselves from the Leftists and Globalists

Now all Putin has to do is focus on the Russian economy while watching the populist parties win in Europe and exit the petrodollar, the EU, NATO, and the Ukraine war while rebuilding Nordstream and their industrial economies.

This combination of events can (a) be blamed on Trump by the mainstream media and Leftist alternative media relentlessly so the Democrats (Leftists and Globalists) can win the 2026 midterm elections, take over the Senate and The House in the midterm elections, and (b) immediately impeach Donald Trump, then (c) win “all three Houses” in the 2028 election and complete the “Seven P Plan of the Left” single-party socialist state objective.

The “Seven P Plan of the Left” series of papers has also been discussed on the Working Brother and Energy News Beat shows, and the entire series will soon be posted on Energy News Beat the Ravengeostrategic websites.

The Trump Administration is Stocked with “Tactical and Operational” Level Personnel

The administration, along with the mainstream media and alternative media channels are at a loss as to what Trump’s strategy is going to be since Putin has avoided talking to any Trump administration advisors until Witkoff went to Moscow to repatriate Fogel.

It appears that the Trump administration was eager to begin the dialogue because he had stated on his first day in office that Putin was going to be eager to end the war in Ukraine.

Trump was told by Kellogg and the Fox News Generals that “Ukraine was winning” and the “Russian economy was collapsing.” He quickly found out that neither of the two mainstream media narratives repeated non-stop by the Fox News anchors was true.

Now the cable news “experts” are baffled by what should be obvious that the European economies cannot exist without fossil fuels and nuclear energy is that they (a) do not know about the Sea Power versus Land Power Grand strategies, and (b) the vital role of “energy” in strategic planning. The cable news “journalists,” or “stenographers,” are neither methodologically trained analysts and grand strategists.

The problem is that the military academy and war college graduates are supposed to be methodologically trained analysts and Kellog and the other television generals clearly are not.

It begs the question “How did they get their stars?”

The Trump administration is stocked with tactical, operational, and regional strategic personnel and lacks the grand strategic level of expertise. The Kellogg disaster means that Hegseth needs to overhaul the curriculum at the military academies and the war colleges as well.

Conclusion-Sit Back and Watch the Globalist Politicians’ Demise

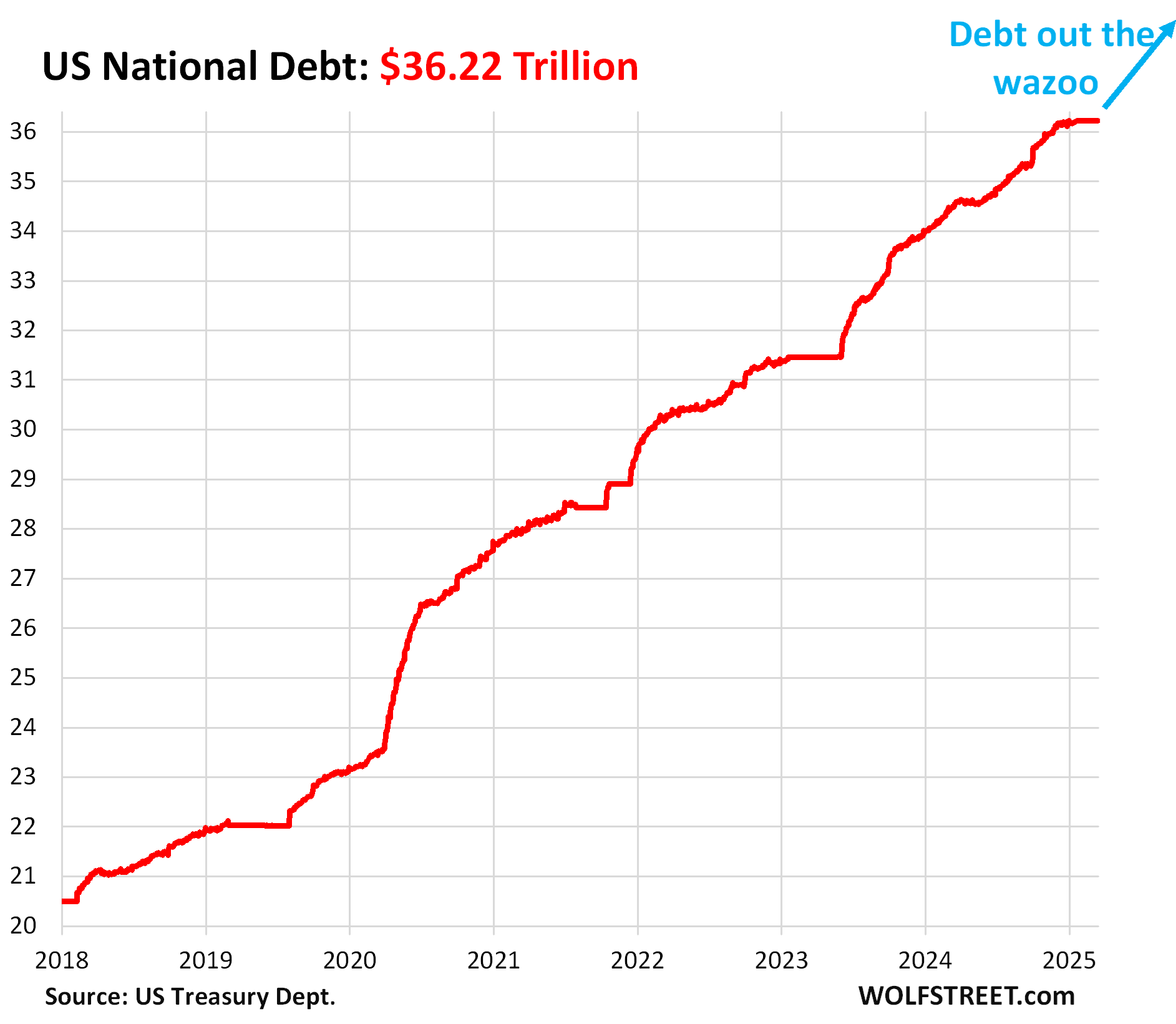

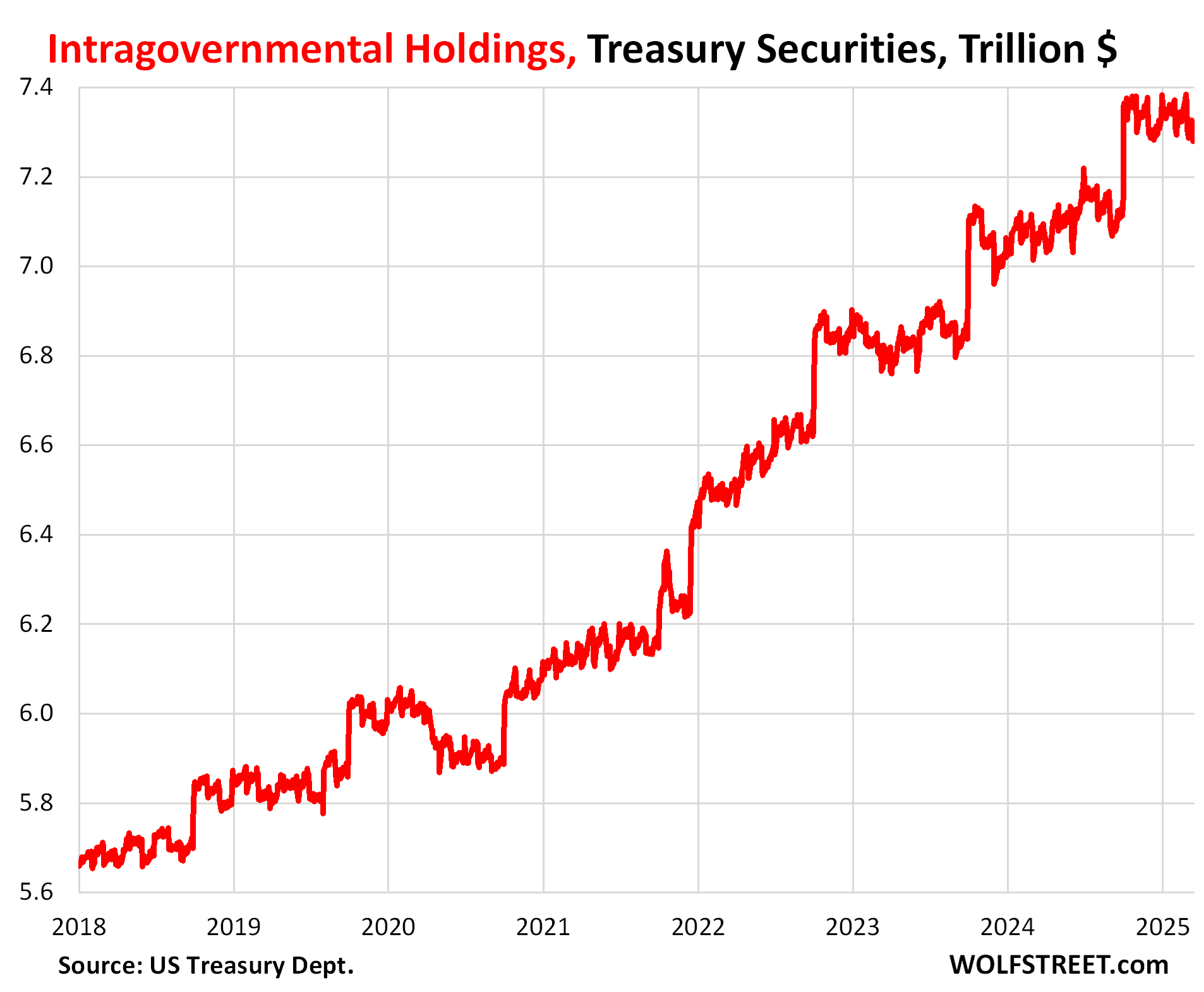

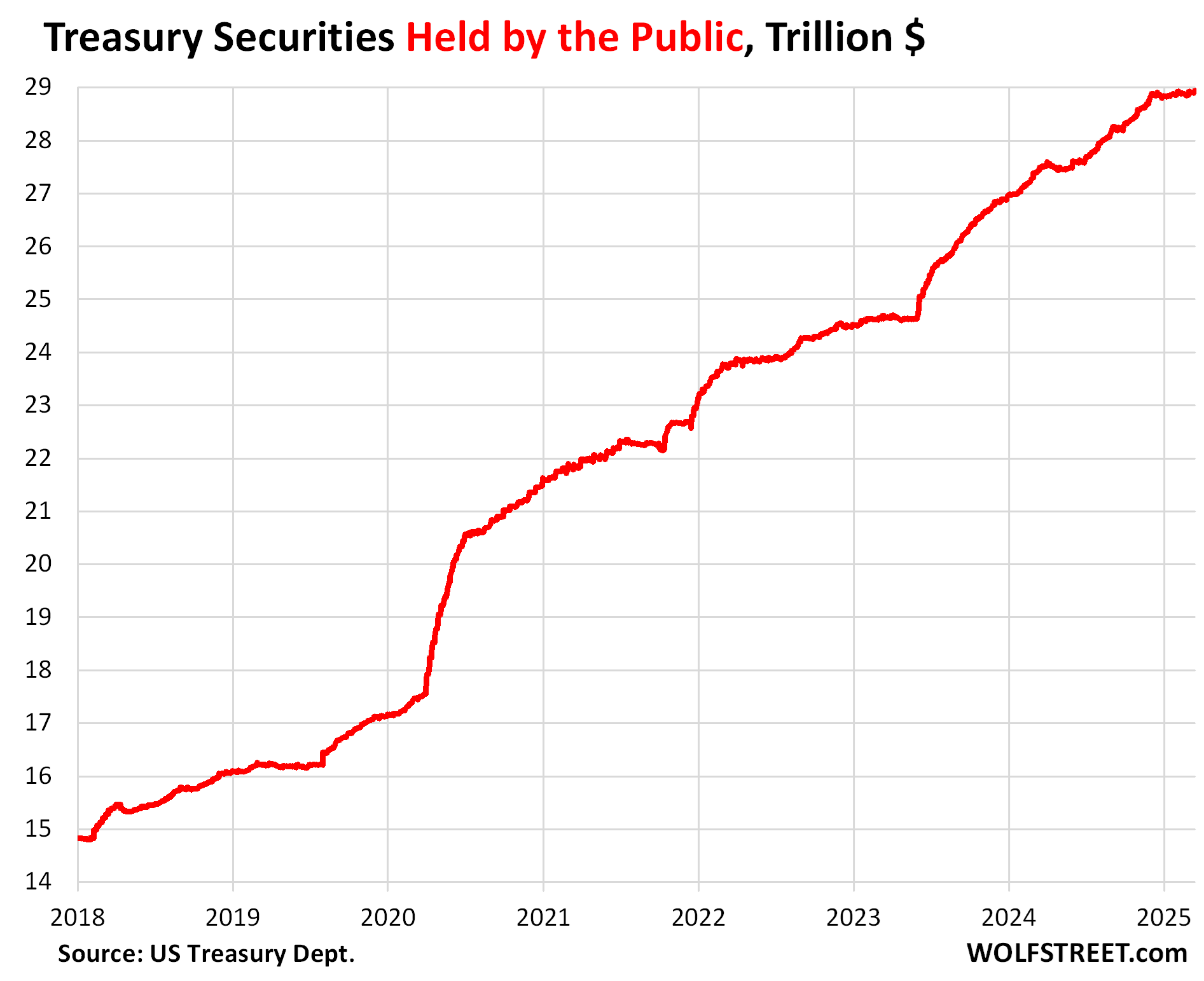

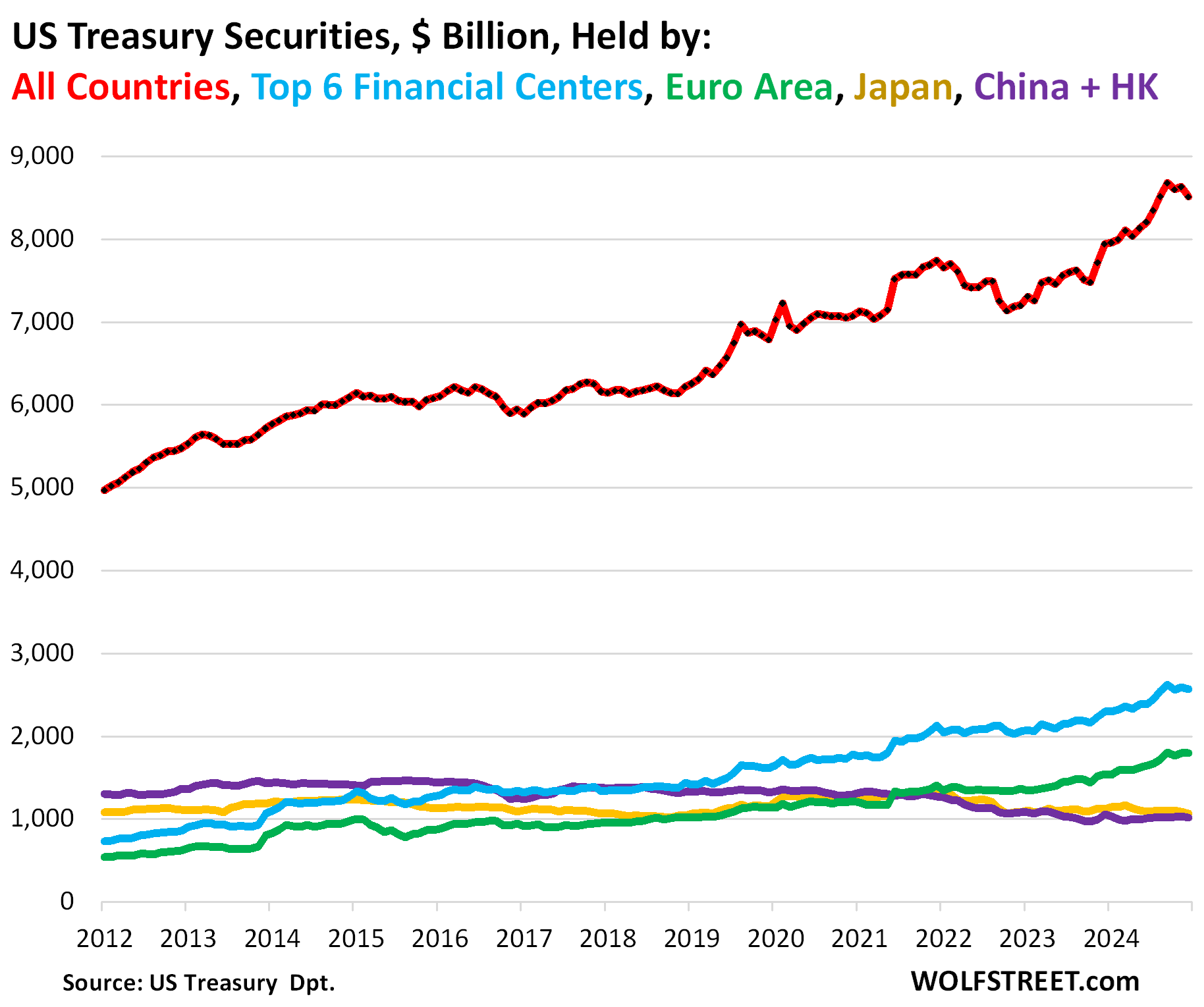

Since it is now in Putin’s best interest to do nothing other than watch the WEF globalist political parties and politicians collapse their economies, it is now in Trump’s best interest to do the same. The reason is simple. The US National Debt rose from under $6 trillion before Bush 43’s global war on terror to $36 trillion at the time of this writing.

It is in Trump’s best interest to prioritize reducing the twin annual current account trade deficits and the yearly budget deficits responsible for the increase in National Debt. Trump cannot let the Left-wing globalist fantasies explained in the “Seven P Plan of the Left” series destroy the West on both sides of the Atlantic.

Therefore, it is in Trump’s best interest to tackle the twin deficits with Elon Musk’s DOGE on one side of the Atlantic and leave the WEF Globalist politicians to their fate on the other side of the Atlantic.

Sweden and Norway have already chastised Germany for the Green Party insisting on a delusional energy policy for the biggest industrial economy in Europe. If Norway and Sweden are pulling back from providing Europe free energy, then why should Donald Trump and America pay for it?

It is now in both Donald Trump’s and Vladimir Putin’s best interest to “do nothing” other than focus on their domestic well-being. Why should the “strange death of Europe” be followed by the “strange death of America.”

Donald Trump’s biggest problem is to explain how and why the Western media and the USAID/NED-backed alternative media channels so misled the European and American audiences over the nature and causes of the Russian invasion of Ukraine.

The fundamentals of the Russian invasion of Ukraine are in the timeline section below. The details are in the various papers posted on Energy News Beat and Raven Geostrategic websites.

Part 3: Understanding the Catastrophic Downside Risk of the Kellogg Plan and Exploring Alternatives

Part 2: Why Keith Kellogg’s Plan is DOA: Shifting the Global Political Center of Gravity Part 2

George McMillan Articles and Interviews: https://energynewsbeat.co/george-mcmillian/

Podcast Interview: The 7 P Plan of the Left – The Transformation of America into a Single-Party Socialist State

The post Foreword to “Kellogg Plan is DOA” series of papers—the main talking point appeared first on Energy News Beat.