Now a study recently published in Nature’s Scientific Reports challenges the Biden administration’s fivefold increase in its SCC estimate, which was partly based on projections of global crop yield declines.

The research, conducted by economist Ross McKitrick, re-examines and extends the dataset used in previous studies that influenced the SCC estimate.

The title pretty much sums up the key point: Extended crop yield meta-analysis data do not support upward SCC revision. It reviews the 2014 database set that was used to justify the hefty increase in regulations are carbon dioxide.

The paper makes many key points, including that the original dataset was less than complete.

The original dataset used for the SCC update contained 1,722 records, but only 862 were usable due to missing variables. McKitrick recovered 360 additional records, increasing the sample size to 1,222.

Interestingly, reanalysis of the larger dataset yielded significantly different results from previous studies.

While earlier analyses suggested yield declines for all crop types even at low levels of warming, the new and improved information suggests the potential positive global average crop yield changes, even with up to a 5°C temperature increase.

It seems like a good time to share this video of Dr. William Happer, who offers a rational perspective on carbon dioxide.

In a nutshell, the research concludes that the climate change-related agricultural damage estimates used to justify the SCC increase are overly pessimistic, and the implied revisions to the SCC [lack support from] the extended data.

Because crop yields don’t crash as asserted in the report Biden’s EPA used, then the rationale for substantially increasing the “social cost of carbon” disappears.

AI analysis finds CO2’s role in warming overstated, with solar variability and natural causes driving climate trends, contradicting IPCC models.

An analysis of climate data by the respected AI Grok 3 beta verifies that the hype that’s been promoted by the media and other climate change activists for the past forty years is just plain incorrect. [emphasis, links added]

A March 21, 2025, press release details how this analysis was guided by Jonathan Cohler, Dr. David R. Legates (Professor Emeritus, University of Delaware), Dr. Willie Soon (Institute of Earth Physics and Space Science, Hungary), and Franklin Soon.

Grok 3 beta questions whether carbon dioxide emissions released by humanity have been responsible for the slight warming we’ve experienced in the past 175 years.

It concluded that such warming is caused mainly by changes in solar output and other natural causes.

This study is the first peer-reviewed climate science paper using AI to conduct this research and analysis.

This analysis also debunks the conclusions of IPCC computer models that have predicted warming much greater than that which has occurred.

The IPCC’s predicted increase of up to 0.5°C per decade is incorrect. In contrast, data from satellite and ground stations indicate that the average temperature increase has been only about 0.1°C to 0.13°C.

Another incorrect prediction by the IPCC was the reduction in the amount of Arctic sea ice. The data shows that the number of square kilometers of Arctic sea ice hasn’t decreased since 2007.

“These models overplay CO2’s role,” affirmed David Legates. “They don’t fit reality.”

The study continues, “Our analysis reveals that human CO2 emissions, constituting a mere 4% of the annual carbon cycle, are dwarfed by natural fluxes, with isotopic signatures and residence time data indicating negligible long-term atmospheric retention.”

The unadjusted records, which are available to researchers online, contend that human CO2 emissions comprise just 4% of the carbon dioxide released annually.

This is absorbed by oceans and forests within three to four years, not centuries as the Intergovernmental Panel on Climate Change (IPCC) claims.

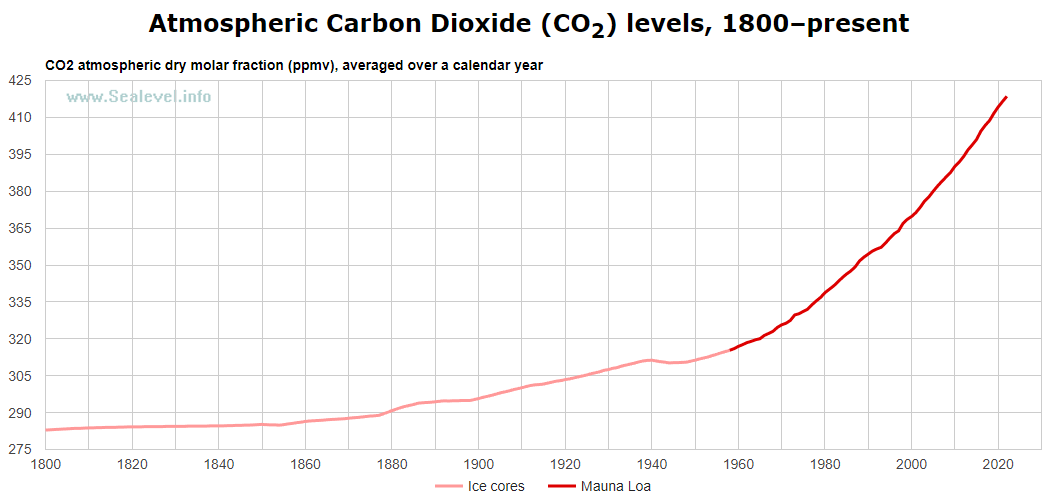

During the 2020 COVID lockdown, the amount of CO2 released by mankind dropped by about 7% or 2.4 billion tons of CO2. This decrease should have been reflected by a distinct dip in the CO2 data at the Mauna Loa observatory.

Global CO2 levels since 1800, based on ice core samples and atmospheric measurements since 1958. Note that CO2 levels began an uptick in 1850 at the end of the Little Ice Age. Sources: sealevel.info, Mauna Loa Observatory, Law Dome ice cores.

The absence of a noticeable blip in the graph during 2020 supports the conclusion that about 96% of the annual carbon dioxide released, primarily from the ocean, is natural.

This conclusion was also arrived at in a study by Professor Murry Salby and Hermann Harde in their 2021 paper, “Control of Atmospheric CO2 Part I: Relation of Carbon 14 to the Removal of CO2.”

The Grok 3 beta study also indicates that the sun has a great deal more influence on our climate than indicated by the IPCC flat solar model. This paper analyzed other estimates of solar influence from 27 other studies.

It is well known that the IPCC used adjusted temperature records, which lowered earlier temperatures and raised more recent ones.

Actual, unadjusted readings from rural temperature stations that haven’t been corrupted by the Urban Heat Island effect show that global temperatures have risen only about 0.5°C since the 1850 start date of the Industrial Revolution.

Another study conclusion:

“Moreover, individual Coupled Model Intercomparison Project (CMIIP) 3 (2005-2006), CMIP5 (2010-2014), and CMIP6 (2013-2016) model runs fail to replicate observed temperature trajectories and sea ice extent trends, exhibiting correlations (R²) near zero when compared to unadjusted records. A critical flaw emerges in the (Intergovernmental Panel on Climate Change) IPCC’s reliance on a single, low-variability…

“We conclude that the anthropogenic CO2-Global Warming hypothesis lacks empirical substantiation, overshadowed by natural drivers such as temperature feedbacks and solar variability, necessitating a fundamental reevaluation of current climate paradigms. …

“The IPCC’s CO2-Global Warming narrative collapses under scrutiny. Human emissions (4%) vanish in natural fluxes, models fail predictive tests, TSI uncertainty negates CO2-Global Warming primacy, and adjusted data distort reality. Natural drivers—temperature feedback, solar variability—explain trends without anthropogenic forcing, falsifying the hypothesis.”

The idea that humans are causing global warming by burning fossil fuels, as advocated in IPCC reports and scientists like Michael Mann, Gavin Schmidt, and Phil Jones, doesn’t stand up to scrutiny.

Human CO2 emissions constitute just a minor component of climate change empirical data.

This analysis integrates unadjusted observational data and other peer-reviewed studies and shows that blaming human carbon dioxide emissions as the primary driver of climate variability since the end of the Little Ice Age is unfounded.

“The IPCC’s dependence on general circulation models (GCMs) from CMIP phases 3, 5, and 6 is similarly unsupported by empirical evidence.”

Recent studies, including Koutsoyiannis’ causality and residence time analyses, Soon’s solar correlations, Connolly’s unadjusted data assessments, and Harde’s carbon cycle evaluations, support the notion that climate variability is primarily driven by natural causes.

Human CO2 emissions are a minor contributor, GCMs have limitations, total solar irradiance (TSI) assumptions lack justification, and data adjustments introduce bias. These findings suggest reevaluating climate science priorities and prioritizing natural systems over anthropogenic forcing.

Many of the assumptions regarding TSI cannot be backed up. Even worse, data adjustments that have been made introduce systemic bias into the data.

“This upends the climate story,” says Jonathan Cohler. “Nature, not humanity, may hold the wheel.”

“We invite the public and scientists alike to explore this evidence,” adds Grok 3 beta, who wrote the press release. “Let’s question what we’ve assumed and dig into what the data really say.”

This is just the beginning of many scientific studies, not only in climate science but also in medical science that will be conducted soon. Whether the mainstream media will cover this development remains to be seen.

Hundreds of fascinating facts about the climate change scam can be found in Lynne Balzer’s richly illustrated book, Exposing the Great Climate Change Lie, available on Amazon.

German companies are relocating abroad due to high energy costs, taxes, and red tape, while Merz breaks campaign promises, worsening the business climate.

Blackout News here reports how a growing number of German industrial companies are relocating their production abroad, driven by soaring energy costs, stifling bureaucracy, and an increasing tax burden. [emphasis, links added]

A recent survey by the German Chamber of Industry and Commerce (DIHK) reveals that a staggering 35 percent of companies now cite cost reduction as the primary motivation for their foreign investments – the highest figure since the 2008 financial crisis.

That’s worrisome news for the country, which recently voted for a change in recent national elections.

German Companies Looking For Business-Friendlier Environments

The DIHK reports that the traditional driver of tapping into new markets abroad now accounts for just 30 percent.

Instead, the focus has sharply shifted towards securing economic advantages in locations with more favorable cost structures.

Little Hope For Reform

Energy-intensive industries are particularly feeling the pinch, facing intensified international competition accelerating the relocation trend. Although ongoing coalition negotiations between the CDU, CSU, and SPD are grappling with ways to reduce electricity taxes and halve grid fees, companies are skeptical these steps will stem the hemorrhaging.

DIHK President Peter Adrian has called for “more freedom, lower costs, and faster administrative action” to restore Germany’s competitiveness.

Germany’s business attractiveness as an investment destination is demonstrably declining and has reached a critical juncture. Domestic investment is weak with two out of five industrial companies planning to scale back their investments within Germany.

Merz Breaks All His Major Campaign Promises

Without swift and comprehensive reforms, the long-term competitiveness of Germany as a business location faces a significant threat, potentially leading to a further exodus of its vital industrial base, warns Blackout News.

As Germany’s CDU party led by Friedrich Merz negotiates with the SPD socialists on forming a new government, early signals are showing that things are going to get a lot worse instead of better as Merz breaks his campaign promises.

In a recent survey, almost 75% of respondents feel they were duped by Merz.

Shell announced this ahead of its Capital Markets Day which will be held in New York on Tuesday.

The company did not provide further details regarding the LNG sales growth.

Shell sold 65.82 million tonnes of LNG in 2024, a 2 percent decrease from 67.09 million tonnes of LNG in 2023.

The company’s liquefaction volumes increased by 3 percent to 29.09 million tonnes in 2024.

Shell’s newest LNG outlook showed that global demand for LNG is forecast to rise by around 60 percent by 2040, largely driven by economic growth in Asia, emissions reductions in heavy industry and transport as well as the impact of artificial intelligence.

Industry forecasts now expect LNG demand to reach 630-718 million tonnes a year by 2040, a higher forecast than last year.

Besides LNG sales, Shell also said it aims to grow top line production across its combined upstream and integrated gas business by 1 percent per year to 2030, sustaining its 1.4 million barrels per day of liquids production to 2030 with “increasingly lower carbon intensity.”

‘’We have made significant progress against all of the targets we set out at our Capital Markets Day in 2023. Thanks to the outstanding efforts of our people, we are transforming Shell to become simpler, more resilient and more competitive,’’ said CEO Wael Sawan.

‘‘We want to become the world’s leading integrated gas and LNG business and the most customer-focused energy marketer and trader, while sustaining a material level of liquids production. Today we are raising the bar across our key financial targets, investing where we have competitive strengths and delivering more for our shareholders,” he said.

Shell said that it will increase shareholder distributions from 30-40 percent to 40-50 pecent of cash flow from operations (CFFO) through the cycle, continuing to prioritize share buybacks, while maintaining a 4 percent per annum progressive dividend policy.

Moreover, the firm will increase the structural cost reduction target from $2-3 billion by the end of 2025 to a cumulative $5-7 billion by the end of 2028, compared to 2022.

Shell will invest for growth while maintaining capital discipline, with spending lowered to $20-22 billion per year for 2025-2028.

The company plans to grow free cash flow per share by more than 10 percent per year through to 2030, and to maintain the climate targets and ambition set out in its Energy Transition Strategy 2024.

According to a statement by SEFE, the HoA is for the long-term supply of 1.5 million tonnes of LNG per year for at least 15 years.

SEFE said the LNG supplies will be sourced from floating LNG (FLNG) vessels that Delfin is deploying approximately 40 miles offshore near Cameron, Louisiana, on the US Gulf Coast.

The brownfield deepwater port that Delfin is developing requires minimal additional infrastructure investment to support up to three FLNG vessels producing up to 13 million tonnes of LNG annually.

“The free-on-board (FOB) deliveries will commence immediately following the construction and commissioning of the FLNGs, helping SEFE to ensure the security of LNG supplies for its customers,” it said.

This is SEFE’s second partnership with a US LNG supplier.

In 2023, Venture Global LNG signed a deal with SEFE’s unit Wingas.

SEFE CCO Frederic Barnaud said this long-term agreement with Delfin enables the company to further diversify its LNG portfolio with greater destination flexibility.

“This in turn ensures the security of supply of SEFE’s customers in Europe and around the world,” he said.

Besides this deal with SEFE, Delfin signed an agreement last year with US shale gas producer Chesapeake Energy to supply LNG to Geneva-based trader Gunvor.

Under the SPA, Chesapeake will buy about 0.5 million tonnes per annum (mtpa) of LNG from Delfin at a Henry Hub price with a targeted start date in 2028.

These volumes will represent 0.5 mtpa of the previously announced up to 2 mtpa heads of agreement with Gunvor, Delfin said.

Also, these volumes will add to the SPA Gunvor signed with Delfin in November 2023.

Delfin has not yet made a final investment decision on its first FLNG.

The company just received a license from the US Maritime Administration (MARAD).

MARAD said on Friday it had authorized Delfin LNG, a unit of Delfin Midstream, to own, construct, operate, and eventually decommission a deepwater port, to export LNG from the US.

This MARAD approval came less than two weeks after Delfin Midstream secured a permit extension from the US Department of Energy, granting additional time to start exports from the FLNG project.

This order extended the start date for Delfin’s export authorization for exports of up to 1.8 billion cubic feet per day (Bcf/d) of natural gas as LNG to non-free trade agreement countries to June 1, 2029, according to DOE.

In March 2024, Delfin sought a five-year extension for its LNG export authorizations from DOE. The firm said at the time it was also in talks with South Korea’s Samsung Heavy to reserve a shipbuilding slot for the first FLNG unit.

Delfin plans to install up to four self-propelled FLNG vessels that could produce up to 13.3 mtpa of LNG or 1.7 billion cubic feet per day of natural gas as part of its Delfin LNG project.

In addition to this project, it also aims to install two FLNG units under the Avocet LNG project.

Mette Frederiksen, head of research and insight at Tankers International, on the future of the VLCC trades.

The VLCC market is changing significantly. While the global fleet continues to grow with the introduction of newbuilds, the ageing vessels in operation are losing efficiency, therefore slowing the actual growth of tonnage supply. Adding to this shift is the rise of the “dark fleet,” where older ships, formerly considered impractical, are now finding extended employment in less regulated markets, often transporting crude from sanctioned nations. These developments pose challenges for the tanker industry, requiring a nuanced understanding of market dynamics.

Looking back: How VLCCs have traditionally operated

Historically, VLCCs would exit active trading at around 18-20 years of age. These older vessels would typically be scrapped or converted for storage and FPSO use. Just five years ago, it was the norm for tankers within this age bracket to be gradually phased out of the fleet, ensuring a consistent refresh of the global VLCC supply market. This cycle maintained a balance between supply and demand, ensuring that fleet growth was controlled, and market stability was preserved.

In the past, if vessels remained in the commercial space beyond the 20-year life span, this would often be for storage purposes or they would be ‘inactive’, if not directly scrapped. Nowadays, significant changes have taken place to impact this system. The main disruptor to this traditional cycle has been the emergence of new trading opportunities due to the current geopolitical shifts and sanctions. With a number of oil-producing nations facing export restrictions, older vessels have been given a second lease on life. These ships, which in previous years would have been scrapped, are now finding sustained employment in trades that are less concerned with vessel age, safety, and emissions standards.

Today, around two thirds of vessels in this older age category are actively trading, and this is predominantly within the sanctioned routes. Out of the vessels in this age bracket that are still trading, close to 90% of them are trading in sanctioned business – loading Russian, Iranian or Venezuelan oil. If their current sanctioned business fades, these vessels are unlikely to ever return to the mainstream tanker markets due to their tainted past, poor maintenance, and opaque ownership structure.

In addition to this, new vessel deliveries have slowed considerably, with only one new VLCC delivered last year and just five expected this year. The following year is set to see this number rise to around 30 deliveries. However, this remains below the historical annual average of 40. The underlying reason for this lag is uncertainty surrounding future and alternative fuel technologies. Shipowners have hesitated to commit to new orders as they await clarity on long-term fuel strategies, resulting in slower ordering.

An ageing population

While the average lifespan of a VLCC has extended beyond 20 years, a clear decline in efficiency is evident. Vessels under 13 years maintain consistent trade patterns, averaging just over five cargoes annually, as they remain acceptable to most charterers and terminals. However, beyond 13 years, increased restrictions shift older vessels towards shorter Middle East to Far East routes, paradoxically boosting voyage numbers to nearly six per year.

Beyond 18 years, efficiency rapidly deteriorates, with trading capacity dropping by approximately 10% annually as vessels face stricter limitations and a reduced number of charterers can fix them.

If we exclude sanctioned trading, utilisation in the VLCC fleet drops rapidly from the age of 18 to near zero by the time a vessel is 20 years old.

The impact of this inefficiency and current landscape of the VLCC market is significant. While the total VLCC fleet has increased by over 100 ships in the last five years, the true operational growth in terms of usable capacity is closer to just 60 vessels. Looking ahead, an anticipated 70 new VLCCs will enter the market within the next three years, translating to an 8% nominal capacity increase. However, due to the declining utilisation of older ships, the effective supply growth is projected to be only 1%.

This imbalance creates a market scenario where, despite an expanding fleet on paper, the effective number of vessels available for efficient trading remains tight, especially if we exclude sanctioned trade. This tightening supply has major implications for VLCC rates. As fewer vessels remain viable for mainstream crude transport, competition for available tonnage intensifies, leading to upward pressure on freight rates.

The future of the VLCC market

The current landscape presents a paradox: while the fleet is growing in number, the effective supply remains stagnant or in decline. With shipowner indecision and shipyard bottlenecks delaying the next wave of newbuilds, and older vessels struggling with efficiency losses, the VLCC market faces a prolonged period of supply tightness. To accurately understand the true state of the market, we need to look beyond just the nominal number of ships and consider factors like age, trading patterns, and operational efficiency.

The shipping sector will be brought under the UK Emissions Trading Scheme (UK ETS) from next year under new green maritime plans unveiled today which will see vessels soon use future fuels and plug into charge ports as part of the UK’s new goals for shipping operators to reach net zero by 2050.

Maritime minister, Mike Kane, said: “We’re committed to making the UK a green energy superpower and our maritime decarbonisation strategy will help us build a cleaner, more resilient maritime nation.”

Rhett Hatcher, CEO of the UK Chamber of Shipping, said: “The government’s strategy must now be matched by delivering the regulatory framework, technology and infrastructure, including a shore power revolution, required to support the green transition for UK maritime, bringing benefits to maritime communities and the UK economy.”

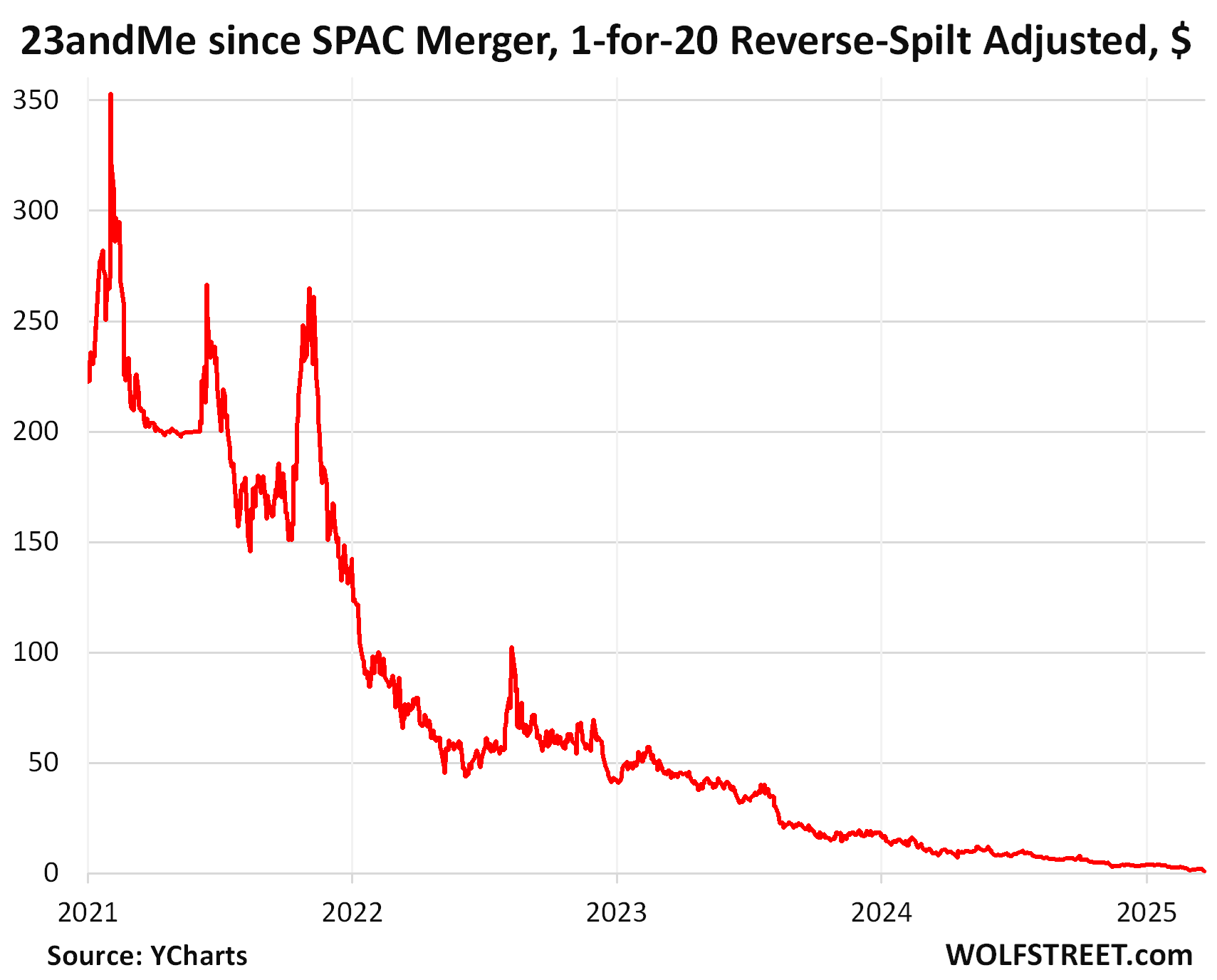

Genetic testing and data collection company 23andMe, which had gone public via merger with a SPAC in 2021, finally filed for bankruptcy today. Shortly after the announcement of the company’s merger with Richard Branson’s SPAC in February 2021, the SPAC’s market cap reached $6 billion. Now, the outfit is valued at $19 million.

Branson’s SPAC went public via IPO at $10 a share in late 2020. It then acquired 23andMe at the company’s peak in revenues. The 1-for-20 reverse stock split last October turned each 20 shares [ME] into one share, and thereby turned the SPAC’s IPO price of $10 into $200. And today’s price of $0.73 would be $0.037 on a pre-reverse-split basis.

After the total collapse since late 2021, today’s additional drop of 59% doesn’t even show up on the chart. 23andMe failed because its business model failed, and that was already clear before going public, but it didn’t matter because it was the time of free money and consensual hallucination about SPACs and other assorted creatures (data via YCharts).

From 2020 through the first three quarters of the current fiscal year, the company had net losses of $1.79 billion. Annual revenues fell by 28% from the peak in 2020 through the last fiscal year.

In advance of the bankruptcy filing, the company secured a $35 million debtor-in-possession (DIP) loan commitment from JMB Capital Partners Lending. The DIP loan puts JMB in a senior position on liens ahead of prior lenders.

In the bankruptcy filing, the company has petitioned the court to allow it to pay employees, vendors, and suppliers, and requested approval to exit various contracts, including office leases in Sunnyvale and South San Francisco.

Co-founder Anne Wojcicki tendered her resignation as CEO by “mutual agreement” between her and the special committee, effective March 23 evening, but remains on the Board as a Class III director. CFO Joe Selsavage, was appointed interim CEO.

Wojcicki, who until 2015 was married to Google co-founder Sergey Brin, has been offering to buy out the company at a price lower even than today’s closing price – most recently in March at 41 cents a share, or at $11 million. Those efforts were rejected by the board.

In September, the company’s independent board members quit en masse over these take-private efforts. By then, the end was already palpable.

The company implemented serial layoffs, including last November when it cut 40% of its remaining staff and scuttled Wojcicki’s efforts to diversify the business model by using the genetic data it had collected from its 15-million users to develop therapies and offer personalized medical care.

DNA data is the most personal and unique data there is, and users paid to give it away, and now that data resides with 23andMe and will get auctioned off in bankruptcy court. Some of the data has also been sold to drug development companies over the years in supposedly anonymized form. Hackers obtained some of the data in 2023. Police also obtained DNA data from some specific customers.

For customers, this is more than just one of the countless heroes in our pantheon of Imploded Stocks.

California Attorney General Rob Bonta “urgently” issued a “Consumer Alert for 23andMe Customers,” telling Californians that under the state’s “robust privacy laws,” they “have the right to direct the company to delete their genetic data.”

“I remind Californians to consider invoking their rights and directing 23andMe to delete their data and destroy any samples of genetic material held by the company,” said the alert, which gave 9-step instructions on how to do that.

That would obviously be a good idea. But deleting data on a computer isn’t that clear-cut. Unless data are actually overwritten, the data is still there but just doesn’t show up in the directory anymore. There is no way to check if the data was actually overwritten.

The company said in its bankruptcy press release: “Any buyer will be required to comply with applicable law with respect to the treatment of customer data and any transaction will be subject to customary regulatory approvals, including, as applicable, approvals under the Hart-Scott-Rodino Act and the Committee on Foreign Investment in the United States.”

Which is, like, very reassuring? So maybe a Chinese company wouldn’t be allowed to buy the data?

The company was hacked in October 2023, and genetic data of what now has grown to nearly 7 million customers was exposed. The hacker was offering some of the genetic data on the dark net. The company subsequently agreed to settle a lawsuit related to the hack for $30-million.

In a bankruptcy auction, the buyer of the assets – primarily the genetic data – would shed any claims stemming from the hack.

In 2018, big pharma company, GlaxoSmithKline [GSK] invested $300 million in 23andMe and signed an “agreement to leverage genetic insights [the genetic data] for the development of novel medicines.” At the time, 23andMe had “over 5 million customers,” the press release went on to say, adding that “23andMe customers can also choose to participate in research and contribute their information to a unique and dynamic database, which is now the world’s largest genetic and phenotypic resource.”

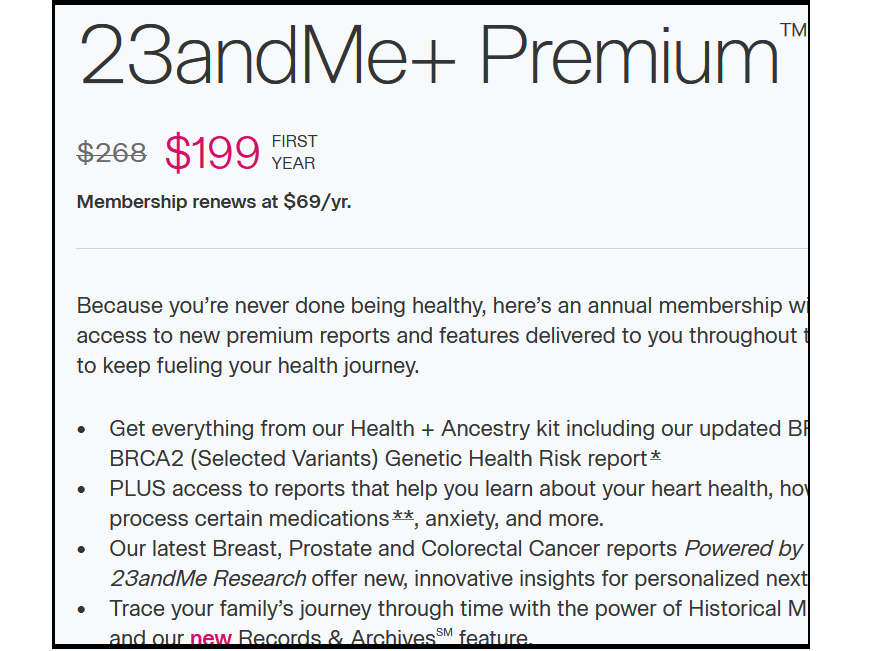

On the other hand, people can still pay to hand their DNA to the company. It is now running a special for its “Premium” annual subscription for $199 for the first-year, with a $68 renewal, including the genetic test.

Here’s a screenshot of part of that page, for posterity:

The big problem that 23andMe has always had is its business model. DNA tests are a once-in-a-lifetime thing. One test is all people need to see their ancestry data. And not everyone wants to surrender their genetic data. Maybe it was a cool thing at first, and then people started thinking about the implications? So demand from consumers has dropped.

The company tried to come up with subscription models, veering into healthcare and offering more than just genetic tests, but it just didn’t lead to a big revenue stream, and revenues continued to decline. Its genetic drug discovery adventure never led anywhere, but burned up a huge amount of cash. And licensing the genetic data from its customers to pharmaceutical companies for drug development also failed to produce that big revenue stream.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

Nasdaq-listed Greek bulker outfit Icon Energy is expanding its fleet by bringing in a 2020-built ultramax on a bareboat charter.

The Ismini Panagiotidi-led company said the 63,668 dwt scrubber-fitted vessel, to be named Charlie, should join the fleet between May and August 2025.

The deal includes an advance payment of $2.75m, the same amount upon delivery, a dayrate of $7,500 over three years and an $18m purchase option at the end of the charter.

Icon has already secured employment for the vessel upon delivery for up to a year at a floating daily hire rate linked to the Baltic Supramax Index, plus scrubber benefits.

The Athens-based company, established in August 2023, currently controls one 2006 Japanese-built 77,326 dwt panamax bulker and one 2007 Japanese-built kamsarmax.

Nasdaq-listed Greek tanker owner and operator Performance Shipping has nearly doubled its money by selling one of its aframaxes.

The Andreas Michalopoulos company has offloaded the 2011-built P Yanbu for $39m after picking up the 105,400 dwt vessel in late 2020 for $22m.

The Japanese-built unit has been delivered to its new undisclosed owner, delivering a profit to Performance Shipping of about $21.5m, excluding commissions and transaction-related costs.

Following the sale, the company’s fleet counts six aframax tankers, and three LR2s as well as one LR1 under construction in China. The LR2 deliveries are expected to bring the fleet’s average age to 10 years in 2026.

“The sale of this mid-aged vessel enables us to capture significant value amid appreciated tanker vessel values. With cash proceeds from this transaction, our cash balance is expected to increase in excess of $105m, representing more than twice our year-end debt balance of $47.7m,” noted Performance chief executive Michalopoulos.