Italian-Swiss dry bulk group Nova Marine Carriers has established a joint venture with Marcegaglia for shipments of raw materials to the manufacturing sites of the Italian steelmaker. The JV called NovaMar Logistic will take over the management of the 2012-built open hatch 26,300 dwt handy bulker Sider Luck and operate it on European cabotage routes, …

Green methanol provider C2X has secured $100m in further investment from A.P. Møller Holding, A.P. Møller – Mærsk and Japanese energy company ENEOS. The proceeds from the investment will primarily be used to fund the final development phase of the Beaver Lake Renewable Energy (BLRE) project which C2X is developing together with SunGas Renewables in Alexandria …

Legal proceedings are set to unfold in the aftermath of last month’s North Sea collision between the containership Solong and the product tanker Stena Immaculate, with owners filing claims against each other. Court records indicate that Solong‘s owner, Ernst Russ from Germany, filed a legal claim at the Admiralty Court on Thursday against “the owners …

Shipping stocks remain under severe pressure today as the world comes to terms with the immensity of Wednesday’s tariff announcements from US president Donald Trump. The average US tariff rate has now been set at just under 25%, levels not seen since the 1930s and the days of the Great Depression. The Trump tariffs resulted …

Oslo-based Atlantica Shipping has seen one of its platform supply vessels contracted long-term in UK waters. Shell is taking the 2003-built Skandi Caledonia on hire for at least one year, with further extension options attached to the contract. The PSV, acquired by Atlantica in 2023 from DOF, which continues to manage the vessel, is scheduled …

Ningbo Ocean Shipping Co (NBOSCO) has announced that Zongquan Xu is stepping down as chairman and will no longer serve as a member of the company. The director and manager at Zhejiang Seaport Shipping is leaving the Shanghai-listed subsidiary of Ningbo-Zhoushan Port Group after four years at the helm. In addition, Xiaofeng Chen has applied …

UK-based Octopus Energy has made another investment in the offshore wind sector, this time via the acquisition of a 10% stake in the East Anglia One wind farm. The 714MW wind farm is located 43 km off the coast of Suffolk in the East of England and has been powering Britain with green energy since …

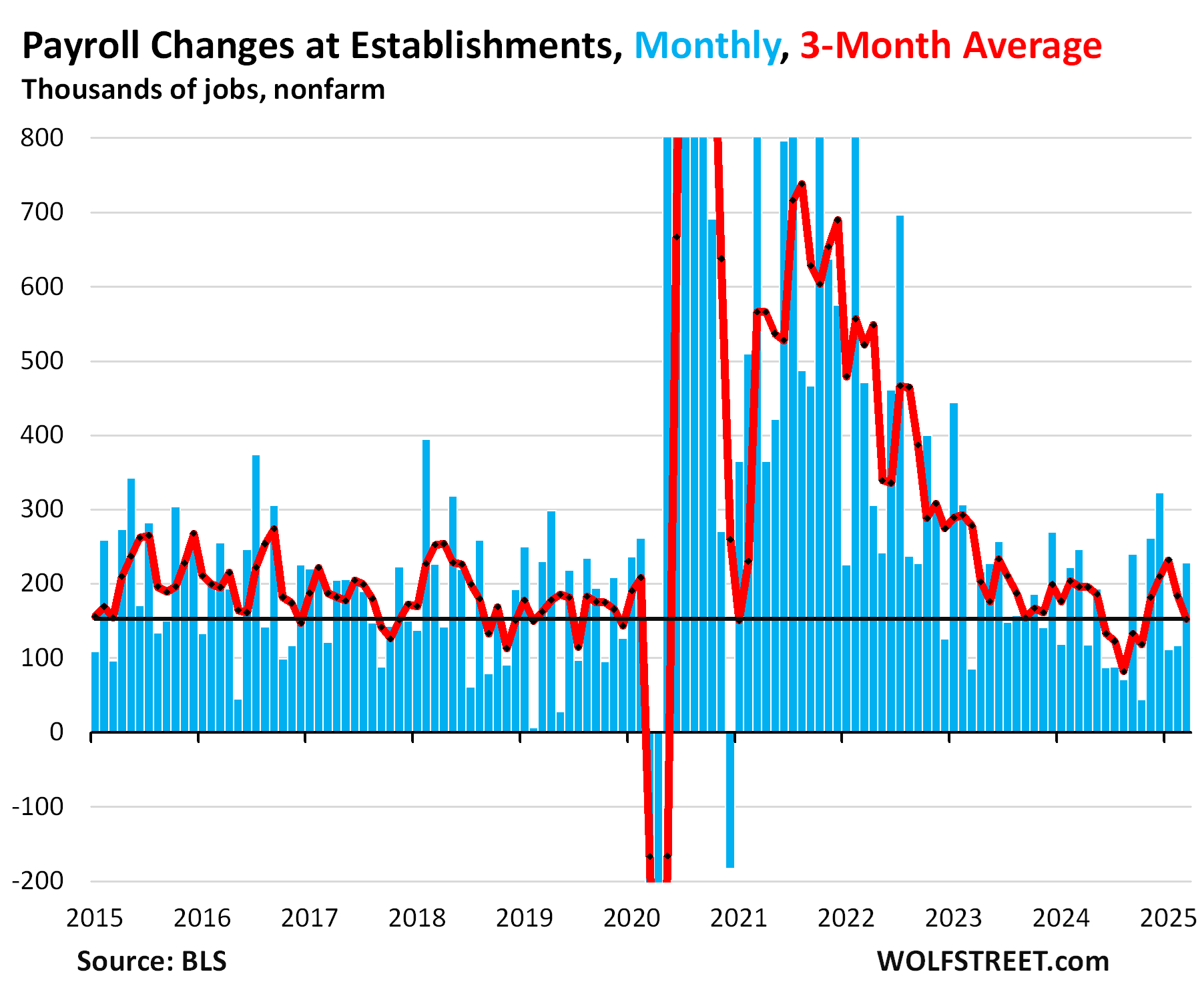

The labor market accelerated in March, after the moderate growth in January and February, despite the job reductions at the federal government, despite the chaos and uncertainty on trade, despite the sour mood of consumers that nevertheless spent like drunken sailors on new vehicles in Q1, despite all the things in the media to scare the bejesus out of everyone.

Total nonfarm payrolls in March jumped by 228,000 from the prior month, blowing past an entire range of projections, to 159.4 million, according to the Bureau of Labor Statistics today (blue columns in the chart).

The three-month average job creation, which includes the revisions and irons out some of the month-to-month squiggles, declined to 152,000 jobs, which is in solid territory (red line).

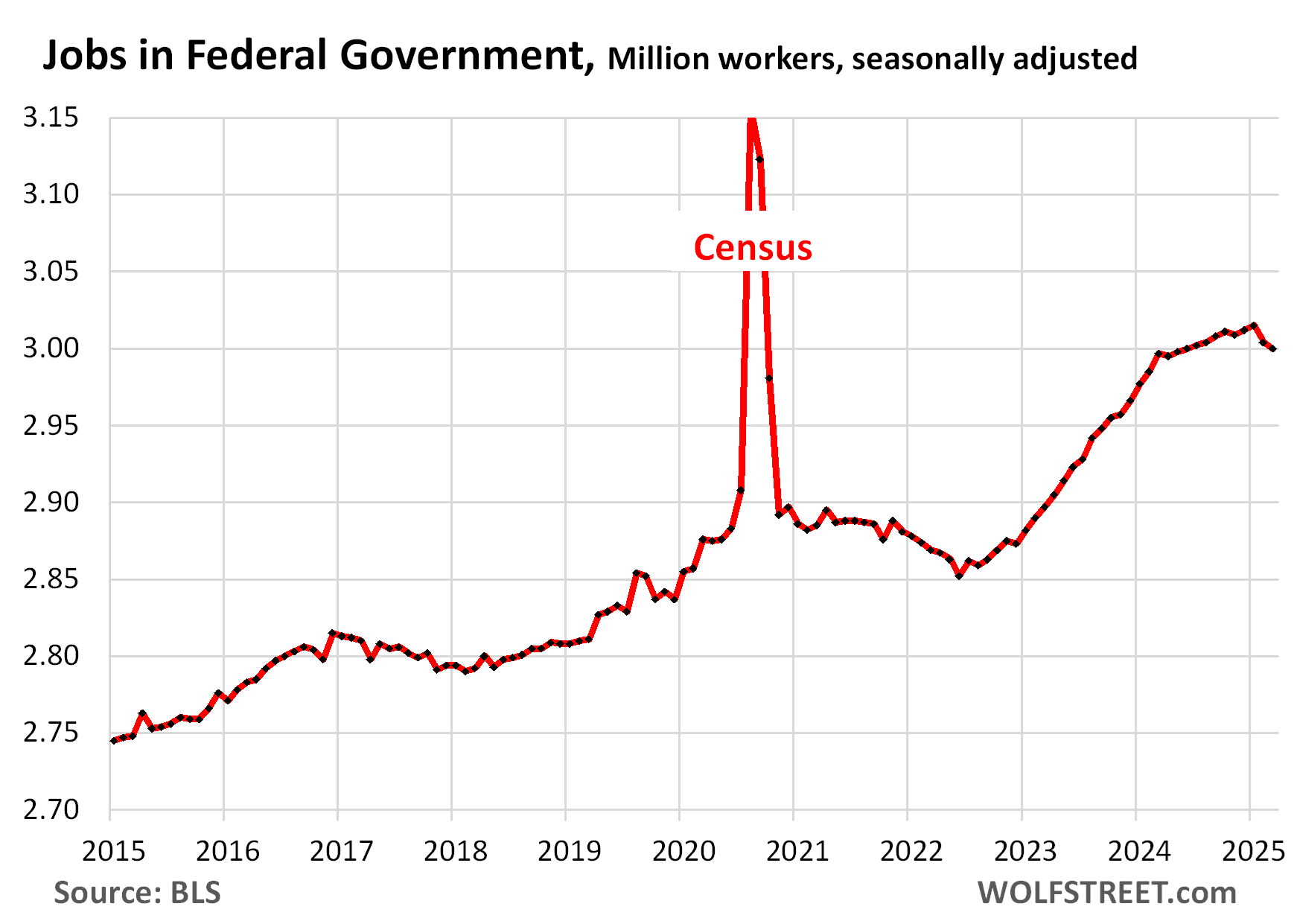

Civilian employment at the federal government – which accounts for less than 1.9% of total nonfarm payrolls – dipped in March by 4,000 to 3.0 million workers, after having declined by 11,000 in the prior month, bringing the two-month decline to 15,000.

This doesn’t yet capture the full effects of the job cuts so far: Workers on paid leave or receiving severance pay are counted as employed until they stop being paid, the BLS pointed out.

This relatively low ratio of federal government payrolls (3.0 million) to total nonfarm payrolls (159.2 million) indicates that the job cuts at the federal government, once they show up to the full extent, won’t make a major dent in overall employment.

This does not include employees working for companies that have contracts with the government. Their employees fall under the various nongovernment categories, such as “Professional and business services,” where employment has actually increased over the past two months despite some layoffs at big government contractors.

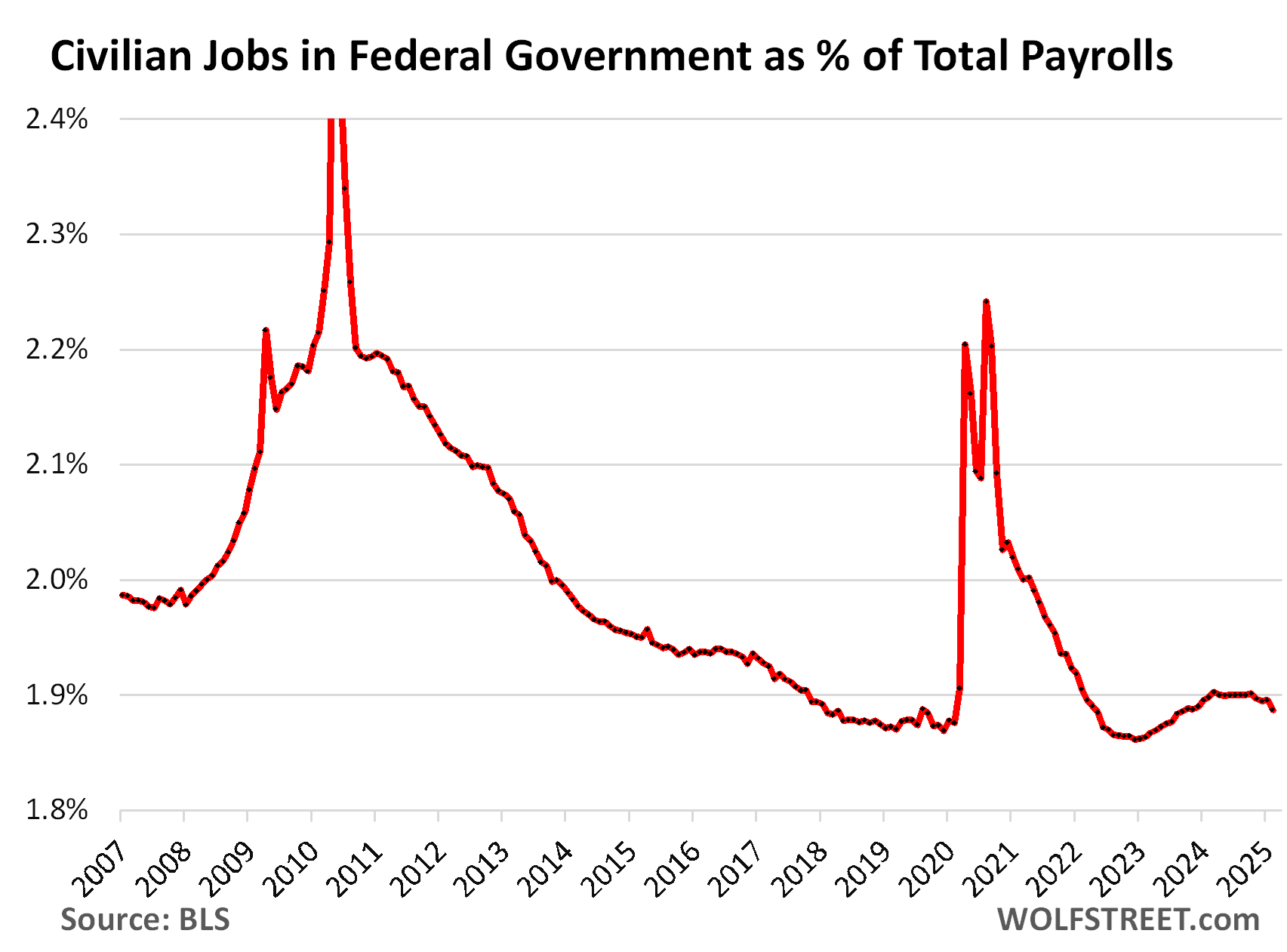

In March, this ratio of civilian government employment to total nonfarm payrolls dipped to 1.89%:

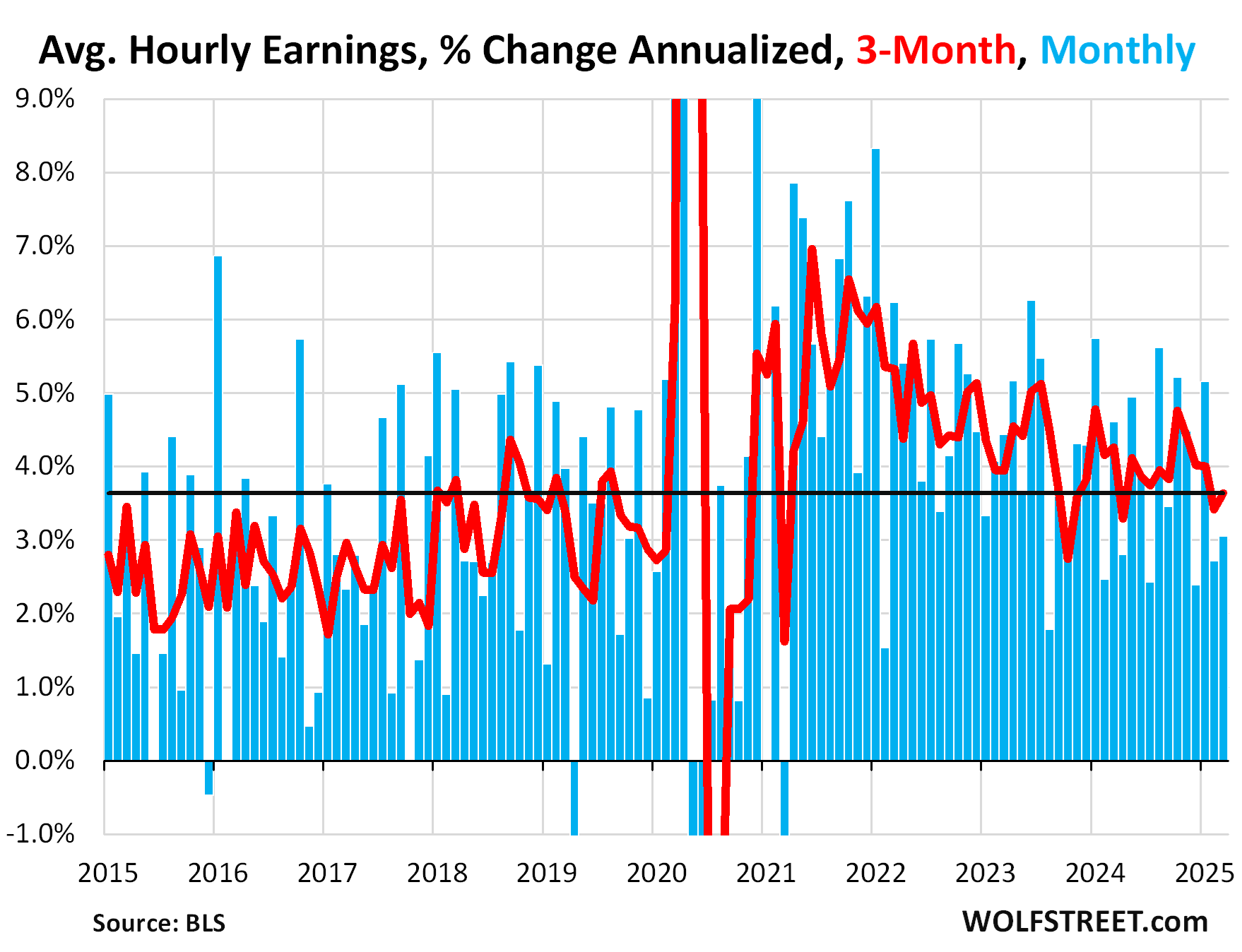

Average hourly earnings rose by 0.25% in March from February (+3.0% annualized), a slight acceleration from February but a deceleration from the hot increase in January of 0.42% (5.2% annualized).

The three-month average rose by 3.6% annualized, a slight acceleration from the prior month (red line).

Year-over-year, average hourly earnings rose by 3.8% in March, after having increased in the 4.0% range in the prior three months.

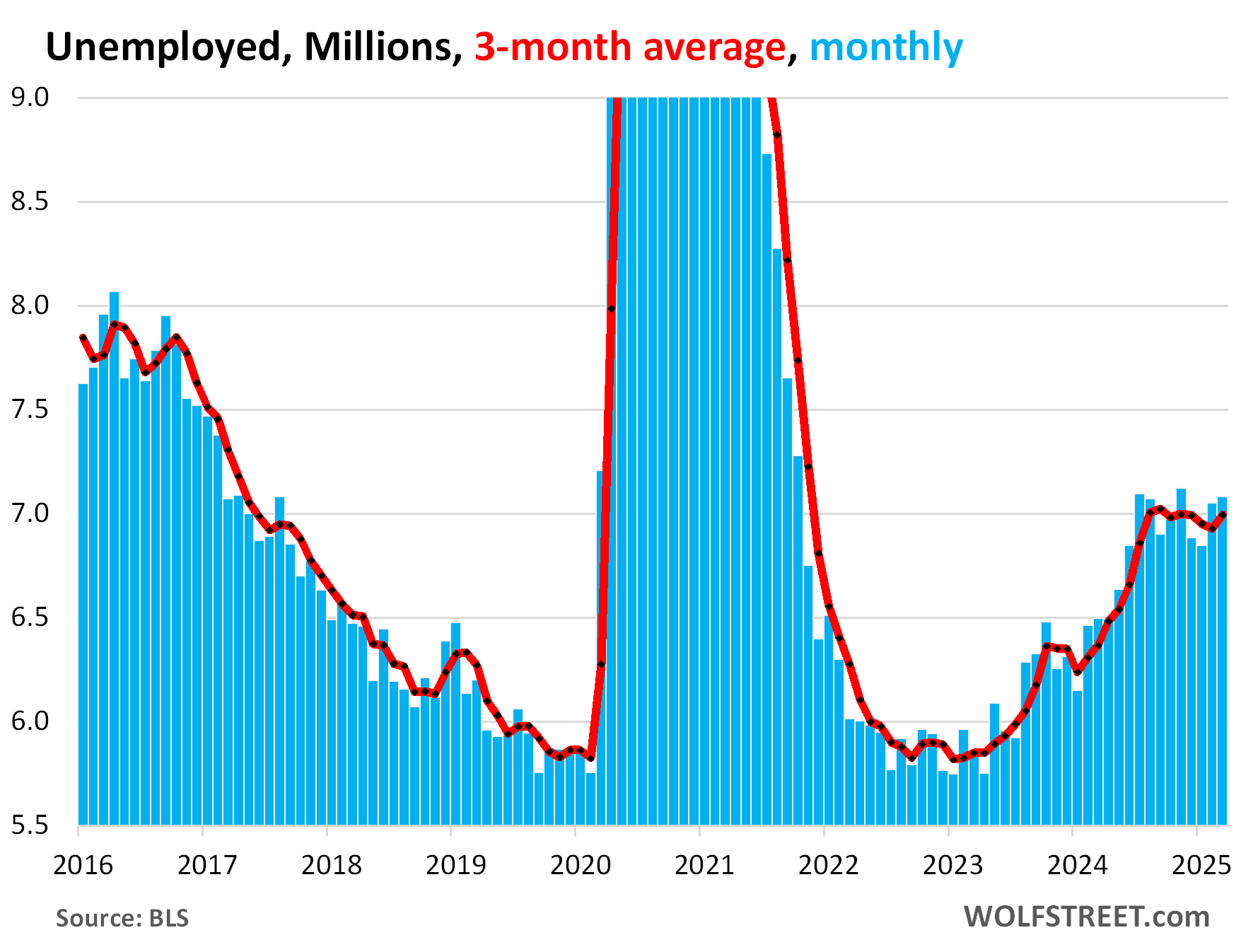

Unemployment ticked up by 31,000 to 7.08 million people who were actively looking for a job during the survey period, according to the BLS household survey today. Unemployment has been in this range since July.

The three-month average rose by 66,000 to 6.99 million and has also been in this range since July (red)

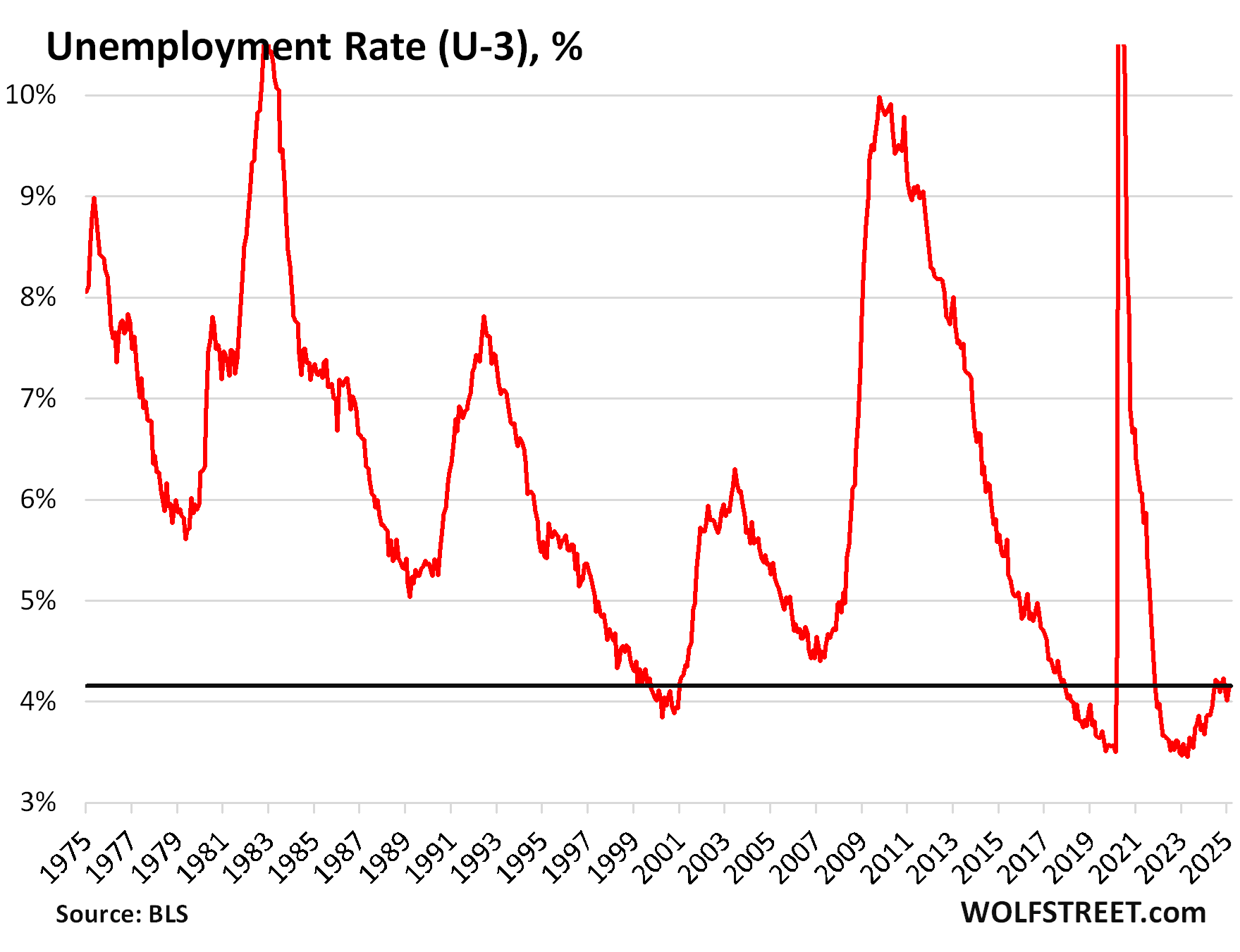

The headline unemployment rate (U-3) edged up to 4.152% (rounded to 4.2%) in March from 4.139% (rounded to 4.1%) in February. The actual increase of 1.3 basis points ended up looking like a 10-basis-point increase due to the effect of rounding.

Over the past 10 months, the unemployment rate has stabilized at the historically low range of 4.0% to 4.2%, with July having been the high point (4.22%) and January the low point (4.01%).

The unemployment rate = number of unemployed people who are actively looking for a job divided by the labor force (number of working people plus the number of people who are actively looking for work).

The Fed faces a peculiar mix of a solid labor market, inflation that has been accelerating for six months, uneven economic growth, and tariff chaos that it fears may add to persistent inflation as businesses and consumers expect higher prices in future years, thereby adjusting to higher prices – the “inflationary mindset,” as I call it – causing inflation expectations to become “unanchored,” which is one of the ingredients thought to allow higher inflation to fester. So Powell was fairly hawkish today, focused on inflation. And in this scenario, it seems markets may have to learn to stand on their own two feet?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

A climate change finance company backed by big-name celebrities has filed for bankruptcy following the arrest of its cofounder.

A climate change finance company backed by big-name celebrities has filed for bankruptcy. The bankruptcy follows the arrest of the company’s co-founder for allegedly attempting to defraud investors of $145 million. [emphasis, links added]

Aspiration Inc., now known as CTN Holdings Inc., [was originally a sustainability-focused financial services firm].

Aspiration is a self-described “climate-friendly banking alternative that’s good for your wallet and the planet.”

“When it comes to climate change, your money is power,” the Aspiration website reads. “You can feel good knowing that your deposits will not fund fossil fuel exploration or production. By moving money to Aspiration, you’re giving the climate a fighting chance.”

Aspiration was reportedly backed by notable celebrities, including Leonardo DiCaprio, Drake, Robert Downey Jr., Orlando Bloom, Cindy Crawford, and billionaire Steve Ballmer.

The climate change banking company – which reached a peak valuation of $2.3 billion in 2021 – shifted to selling carbon credits to other businesses in 2023, which Forbes described as a “strange pivot.”

Aspiration then brokered carbon credit deals with major corporations such as Microsoft, Meta Platforms, and Ballmer’s Los Angeles Clippers.

Aspiration was founded in 2013 by Andrei Cherny and Joe Sanberg – both heavily linked to the Democratic Party.

At age 21, Cherny became a speechwriter for former President Bill Clinton. Cherny is a former chair of the Arizona Democratic Party.

He previously lost the Democratic primary in Arizona for the U.S. House of Representatives in 2012 to Kyrsten Sinema. The Democrat also lost in 2024 when running in Arizona’s 1st Congressional District election.

Meanwhile, Sanberg is a progressive anti-poverty advocate and a Democratic donor.

On March 3, 2025, the U.S. Attorney’s Office of California’s Central District announced that Sanberg had been arrested on a federal criminal complaint accusing him of conspiring to defraud two investor funds of at least $145 million.

Joseph Neal Sanberg, founder of the climate-focused banking startup Aspiration, was arrested for allegedly defrauding investors of $145 million. Image via screencap

Sanberg’s alleged co-conspirator, Ibrahim Ameen AlHusseini, pleaded guilty to wire fraud for falsifying documents and information to assist Sanberg.

Ibrahim Ameen AlHusseini – also a prolific donor to Democrat causes who served on Aspiration’s board of directors — allegedly participated in the scheme to defraud investors.

“According to the complaint against Sanberg and AlHusseini’s plea agreement, Sanberg obtained $145 million in loans secured by AlHusseini, who Sanberg knew did not have sufficient financial assets to cover those loans if Sanberg defaulted,” the statement read.

“Sanberg hid this fact from investors, then defaulted on the loans, which resulted in at least a $145 million in losses.”

Sanberg allegedly negotiated multimillion-dollar loans by pledging Aspiration stock as collateral.

Prosecutors said of AlHusseini, “At Sanberg’s direction, the defendant made untrue statements. Defendant and Sanberg knew that the falsified statements inflated the value of the assets in defendant’s accounts by tens of millions of dollars.”

The U.S. Attorney’s Office of California’s Central District said Sanberg defaulted on a $145 million loan in November 2022 and again in the spring of 2023.

Sanberg has pleaded not guilty.

Sanberg’s lawyer, Marc Mukasey, stated, “Mr. Sanberg has pleaded not guilty to the charges. We will buckle down and defend him with vigor and zeal.”

If convicted, Sanberg faces a maximum prison sentence of 20 years.

Forbes reported, “The charges against Sanberg relate only to his personal conduct; CTN isn’t implicated, according to a court filing.”

In a filing in the U.S. Bankruptcy Court in Wilmington, Delaware, chief restructuring officer Miles Staglik said he doesn’t believe the accusations implicate CTN in any criminal activity.

However, investors affiliated with Sanberg reportedly stopped providing funding to CTN in February 2025.

Staglik admitted that the criminal case has hurt the company’s ability to raise capital to operate. CTN had trouble finding sufficient funding to keep the business afloat, according to bankruptcy filings.

Staglik “emphasized that current management and employees were unaware of the alleged misconduct and that the business itself is a victim,” according to the Wall Street Journal.

Sanberg no longer holds any positions at CTN Holdings and is no longer involved in its operations.

On March 30, 2025, Aspiration, which had been rebranded as CTN Holdings, filed for Chapter 11 bankruptcy protection in Delaware. The company reportedly has approximately $170 million in debt.

Bloomberg reported, “CTN’s largest unsecured creditor is the National Basketball Association’s Los Angeles Clippers and Kia Forum, which are both owned by Steven Ballmer. Aspiration’s backers included Ballmer, whose Clippers and Kia Forum hold roughly $40 million in unsecured claims for ‘contracted carbon credits’ and ‘carbon credit value,’ according to the bankruptcy petition.”

Ballmer is a “major funder of progressive-left groups,” according to Influence Watch.

In addition to the potentially damning Sanberg allegations, the U.S. Department of Justice and the Commodity Futures Trading Commission have reportedly been investigating Aspiration over its claims of “planting 35 million trees, raising questions about the validity of its environmental impact,” according to Forbes.

The Department [for Energy Security and Net Zero] has more to do to convince Parliament that it has a robust plan for ensuring security of energy supply to meet increasing demand.

The security of the energy supply is the highest priority for the Department. Energy demand is set to rise from increasing numbers of electric vehicles and heat pumps, data processing centres, and the move to building homes.

The stability of the energy grid might be affected by the Department’s plans to move towards cleaner power by 2030, because intermittent renewable energy from wind and solar vary according to weather conditions.

Nuclear is an important low-carbon form of baseload generation but there are questions around the life and capacity of the existing plants and the time needed to get small modular nuclear reactors up and running.

In January 2025, the National Energy Systems Operator issued a routine notification to energy providers to increase supply after energy generation briefly fell below a margin set to make sure demand in the days ahead was met.

the Department should set out … how it will make sure there is capacity in the grid when there is low generation from renewable energy during periods of calm weather, including from wider technologies like nuclear.

The Committee has very good reasons to be concerned.

NESO emphasised that we would need to maintain our full existing fleet of gas power stations long after 2030, keeping them ticking over for the inevitable periods when the wind does not blow and the sun does not shine.

However, many of our gas plants are now more than 30 years old, and there is little attraction in keeping them open just to switch them on for an odd day here and there.

Many of these may not still be open in five or ten years. From a technical point of view, keeping them idling for weeks at a time creates problems as well.

In short, if Ed Miliband wants 30 GW of gas power plants on standby in 2030, he will have to pay through the nose for it.

He will also have to subsidise the construction of a large tranche of new gas-generating capacity.

The problem is that, as the PAC point out, demand for electricity is set to grow rapidly in coming years to power electric cars, heat pumps, data centres and industry. NESO reckon that peak demand could rise to 62 GW by 2030.

In January, when we came perilously close to blackouts, demand peaked at 48 GW, with gas power stations and interconnectors working flat out.

There could have been blackouts if one major generator or interconnector had gone down. It does not take a genius to work out that we will not have enough reliable, dispatchable generating capacity to meet the projected demand in 2030.

Miliband’s plan is, of course, to triple wind and solar capacity, but this will make little difference. After all, three times nothing is still nothing!

NESO recognizes this problem, and their solution is to drastically cut demand on the system when wind power drops away, sometimes by as much as 10 percent. This will either be done by price rationing or rolling blackouts.

This should not be acceptable in a supposedly advanced country.