Energy News Beat

The strategy: Let inflation rip to bring the horrible debt-to-GDP ratio down. Households & yield investors pay for it. Turns out, no free lunches after all.

By Wolf Richter for WOLF STREET.

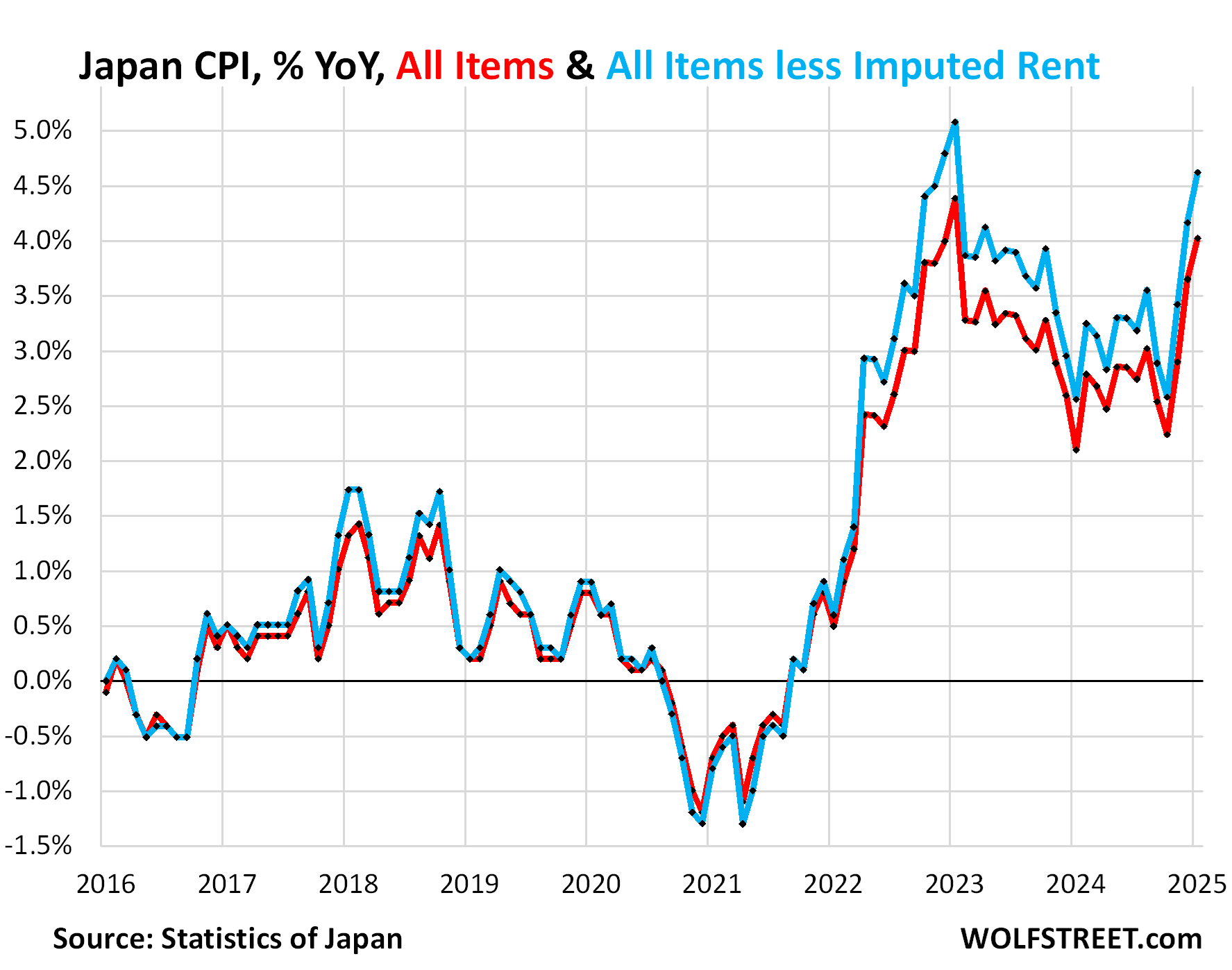

The “all items” Consumer Price Index for Japan surged by 4.02% in January year-over-year, the worst inflation rate since January 2023, and beyond that one month, the worst rate since 1981 (red in the chart).

The all-items CPI minus “imputed rent” – a calculated figure derived from other indicators – spiked to 4.6%, according to Statistics Japan on Friday (blue).

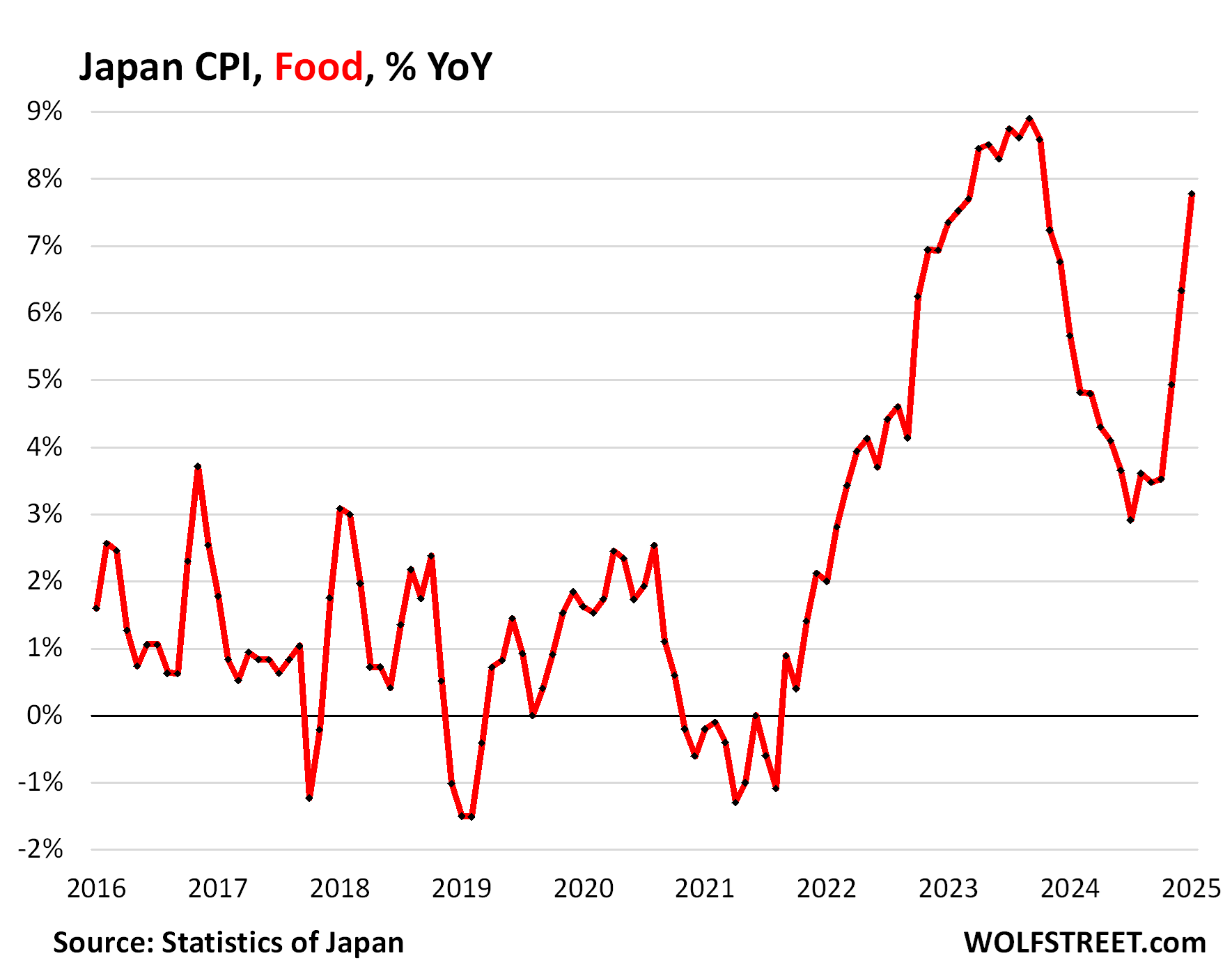

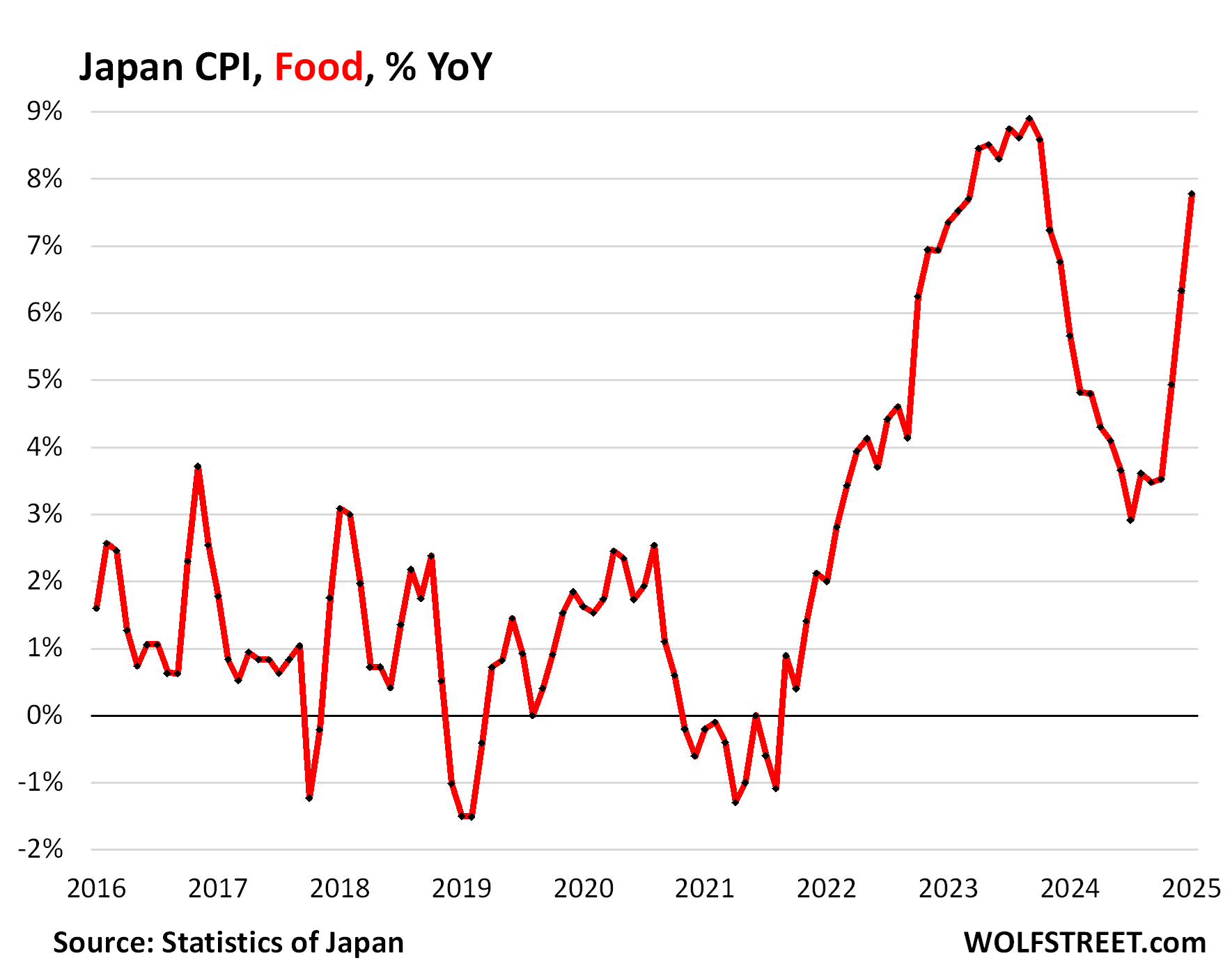

Fresh food prices soared by 7.8% year-over-year, driven by prices of fresh good, +22%, including +25.6% for vegetables and seaweeds and +22.6% for fresh fruits. Inflation in fresh foods has been bad since early 2022.

Japanese households devote a relatively large share of their spending to food, a far higher share than any other country in the G7, based on the Engel coefficient, according to the Nikkei last November. So this hurts:

Energy prices soared by 10.8% year-over-year, with electricity soaring by 18.1% and gas to the home up by 6.2%:

This includes electricity, manufactured & piped gas, liquefied propane, kerosene (used in common household space heaters), and gasoline.

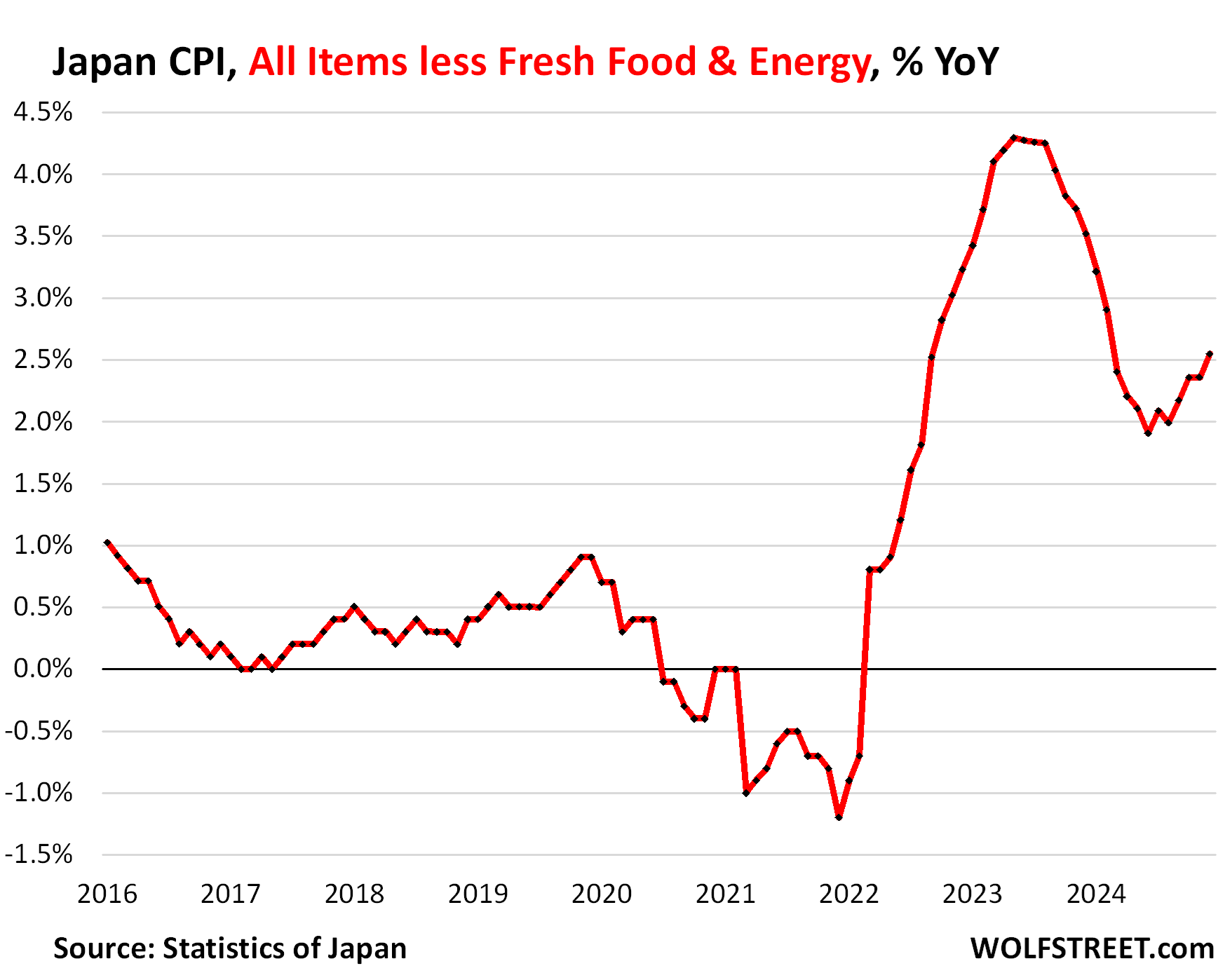

Core CPI – the all-items CPI minus fresh food – accelerated to 3.2%, the worst since June 2023.

Excluding both fresh food and energy, inflation rose by 2.6%. This is a key metric for the Bank of Japan’s 2% inflation target.

The Bank of Japan has raised its policy rate three times to a whopping 0.5%, starting from -0.1%. And it indicated that it would raise rates further in baby steps. The BOJ also started QT in 2024 and is accelerating it in 2025, but it’s a slow process, and its balance sheet is gigantic.

With the BOJ’s policy rate at 0.5% and the 10-year yield of Japanese Government Bonds (JGBs) at 1.34% currently, investors in fixed income products are getting eaten alive on a daily basis by this 4.0% inflation.

By contrast, in the US, CPI is at 3.0% (Japan is at 4.0%), while the midpoint of the Fed’s policy rates is 4.33%, and the 10-year Treasury yield is at 4.5%, still compensating investors for inflation plus some.

But Japan’s long-run fiscal mess, with a debt-to-GDP ratio of 254% in 2024, is more than twice as terrible as the US fiscal mess with a debt-to GDP ratio of 122%.

The Bank of Japan is clearly trying to resolve Japan’s sovereign debt problem, the biggest in the developed world, by fueling inflation to devalue that debt — along with everything else denominated in yen.

And it’s working in its insidious way: Under the impact of this inflation, the debt-to-GDP ratio has been edging lower, from the peak of 260% in 2022. Turns out, there are no free lunches after all, someone is going to pay for it, and it’s the Japanese households, through much higher prices and steeply negative “real” yields on their yield investments. But after decades of reckless government profligacy, there really aren’t many alternatives left to deal with it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Inflation Spikes to 4.0% in Japan, Much Worse than in the US. BOJ Babied its Rate to Just 0.5%, with More Baby Hikes in View appeared first on Energy News Beat.