Energy News Beat

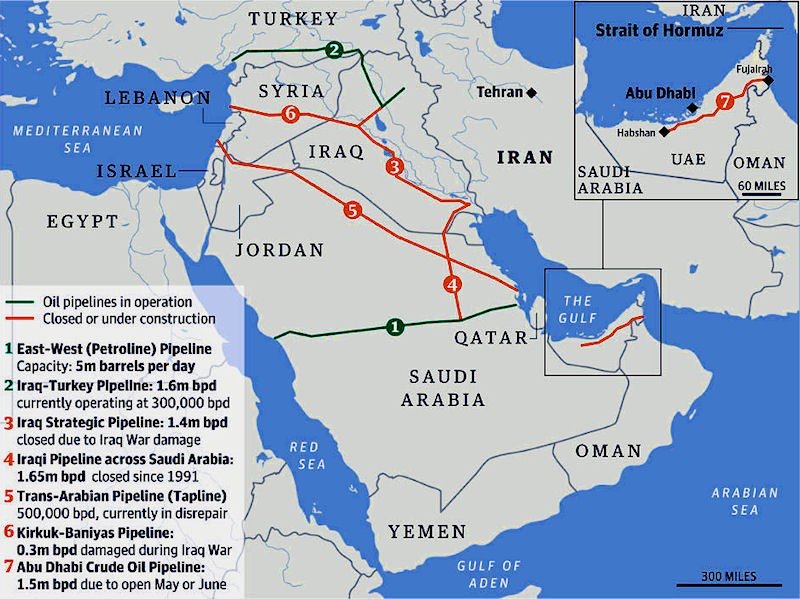

The world is facing its most severe oil and gas supply crunch in history, triggered by the ongoing Middle East conflict and prolonged disruptions to flows through the Strait of Hormuz—the chokepoint carrying roughly 20% of global oil. What began in late February as a short-term geopolitical flashpoint has evolved into a structural crisis, with cumulative supply losses now approaching one billion barrels and daily shortfalls estimated at up to 8 million barrels per day (roughly 8% of global supply).

Analysts at the International Energy Agency (IEA) have described it as the “largest disruption to crude supplies in the history of the global oil market,” while Goldman Sachs has labeled it the “largest-ever supply shock,” prompting upward revisions to oil price forecasts (Brent now expected to average around $85–$100+ per barrel in 2026).

In response, energy security has surged to the top of government and corporate agendas. Industry leaders who have long warned of underinvestment in exploration and production (E&P) are now seeing their calls heeded. The result: a renewed global oil exploration boom, focused on diversified, resilient supply chains far from the Middle East.

Why Exploration Is Booming Again“Production and recovery represent the most immediate path to incremental barrels,” said SLB (Schlumberger) CEO Olivier Le Peuch. “As customers continue to prioritize energy security and national resource development, investment in this space is set to grow.”

Baker Hughes Chairman Lorenzo Simonelli echoed the sentiment: the conflict is “further reinforcing energy security as a priority, which is expected to support structural growth in upstream and global energy infrastructure spending… It’s going to be about diversifying the energy mix and making it more durable.”

ExxonMobil CEO Darren Woods added that countries without strategic petroleum reserves are now racing to build them, while importers hunt for alternative sources.

Higher oil prices—sustained above $90–$100 per barrel—are delivering windfall cash flows that companies are channeling back into drilling rather than returning solely to shareholders. Rystad Energy estimates U.S. shale producers alone could generate an extra $63.4 billion in cash flow in 2026 if prices average $100 per barrel.

Key Countries and Regions Leading the Charge

Africa has emerged as one of the clearest long-term winners. With vast underdeveloped reserves and lower geopolitical risk premiums compared to the Middle East, the continent is set to account for roughly 40% of global high-impact exploration wells in 2026. Activity is concentrated along the Atlantic margin—particularly the Orange Basin offshore Namibia and South Africa, and the Gulf of Guinea in West Africa.

Major projects include: Uganda’s Lake Albert developments (first oil targeted for 2026 at ~190,000 bpd via the East African Crude Oil Pipeline).

Nigeria and Angola expansions.

Namibia’s Venus discovery and related ultra-deepwater plays.

Upstream investment across Africa is forecast at $41 billion in 2026, with production climbing toward 11.4 million bpd.

The Americas remain a core focus. U.S. shale (especially the Permian Basin) continues to deliver record exports, though domestic fuel prices have risen as a result. ExxonMobil and other majors are ramping up activity where infrastructure already exists. South America is also gaining momentum: Guyana’s Stabroek Block (led by ExxonMobil) is producing over 900,000 bpd and expanding; Suriname’s offshore blocks and Brazil’s pre-salt developments are attracting fresh capital.

Other non-OPEC+ growth hotspots include Canada and Brazil, which were already projected to drive supply increases before the shock accelerated diversification efforts.

Major Companies Positioned to Benefit

Upstream Majors: ExxonMobil – Leading in Guyana and the Permian; actively reassessing global energy security exposure.

Chevron, ConocoPhillips, Shell, and BP – All poised for cash-flow gains in U.S. shale and select international plays.

TotalEnergies – Strong Africa and Suriname exposure.

Petrobras – Deepwater Brazil pre-salt expertise.

Oilfield Services Leaders (set for increased E&P spending): SLB (Schlumberger)

Baker Hughes

Halliburton

Offshore drillers such as Noble Corporation, Transocean, and Valaris.

These service providers are already signaling stronger 2026 activity as operators shift capital toward exploration and recovery. Potential Impact on Consumers and Investors

For Consumers:

Higher crude prices translate directly into elevated gasoline, diesel, heating oil, and jet fuel costs—acting like a broad “tax” on households and businesses. U.S. average gas prices have already climbed above $4.50 per gallon in some reports amid the shock.

This squeezes discretionary spending, raises inflation (a 5% oil price increase typically adds ~0.1% to overall inflation), and can slow economic growth. Prolonged high prices risk stagflationary pressures, though U.S. resilience and diversified supply have so far limited recessionary fallout.

For Investors:

The boom creates clear winners. Energy stocks, particularly integrated majors and shale producers, are benefiting from fatter margins and free cash flow. Oilfield service companies stand to gain from a multi-year upcycle in drilling and infrastructure spending. Diversified E&P exposure in Africa, Guyana, and the U.S. offers upside from both higher prices and new discoveries. However, volatility remains: if the Hormuz disruptions ease rapidly, prices could retreat; sustained high prices risk demand destruction or policy responses. Long-term, the structural shift toward resilient supply chains favors companies with strong balance sheets and low-breakeven assets.

Outlook

The longer the current supply shock persists, the more permanent the pivot toward diversified exploration is likely to become. Whether the crisis resolves in weeks or months, the industry consensus is clear: energy security now demands greater redundancy, more upstream investment, and a broader geographic spread of supply. For investors and policymakers alike, the message is that the oil exploration boom is not a temporary spike—it is a strategic response to a changed global risk landscape.

Appendix: Sources and Links

- Original OilPrice.com article: https://oilprice.com/Energy/Crude-Oil/Global-Supply-Shock-Reignites-Oil-Exploration-Boom.html (May 12, 2026)

- IEA reports and statements on historic disruption: https://www.rte.ie/news/business/2026/0312/1563033-oil-shock-largest-supply-disruption-iea/ and related coverage.

- Goldman Sachs oil forecast revisions: https://www.bloomberg.com/news/articles/2026-03-23/goldman-sachs-raises-oil-forecasts-on-largest-ever-supply-shock

- Rystad Energy U.S. shale cash flow analysis: https://finance.yahoo.com/news/100-oil-could-deliver-63-230000864.html

- Rystad Energy on Africa high-impact drilling 2026: https://www.rystadenergy.com/news/high-impact-oil-gas-wells-2026-upstream-exploration and https://www.worldoil.com/news/2026/1/28/africa-set-to-lead-global-high-impact-exploration-drilling-in-2026/

- African Energy Chamber 2026 Outlook: https://energychamber.org/14-african-oil-gas-projects-driving-the-continents-energy-boom/

- Additional context from Bloomberg, HBR, and market reports on supply shock scale (various 2026 articles).

- Oil & Gas drilling company rankings and services leaders (FinanceCharts, VanEck, etc.).

All data and quotes drawn from publicly available industry reports and executive statements as of May 12, 2026. Markets move fast—always conduct your own due diligence.

The post Global Supply Shock Reignites Oil Exploration Boom appeared first on Energy News Beat.